BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

In the modern professional landscape, specialization is often celebrated, but it is the rare individual who bridges two highly technical, demanding fields that seem worlds apart. Podiatrists who are also Certified Public Accountants (CPAs) embody this uncommon duality. They combine the clinical precision of medical practice with the analytical rigor of financial expertise. While the pairing may appear unconventional at first glance, the intersection of podiatric medicine and accounting creates a powerful skill set that benefits not only the practitioners themselves but also the patients, healthcare organizations, and broader medical community they serve.

Podiatrists focus on diagnosing and treating conditions of the foot and ankle—areas of the body that are deceptively complex and essential to mobility. Their work requires deep anatomical knowledge, surgical skill, and the ability to manage chronic conditions such as diabetes‑related neuropathy. At the same time, podiatrists operate in a healthcare environment that is increasingly shaped by financial pressures, regulatory requirements, and business realities. Running a podiatry practice demands far more than clinical competence; it requires strategic financial management, compliance with tax and healthcare regulations, and the ability to navigate insurance reimbursement systems. This is where the CPA credential becomes a transformative asset.

A podiatrist who is also a CPA brings a level of financial literacy that most medical professionals simply do not possess. They understand the intricacies of tax law, financial reporting, and business planning. This dual expertise allows them to manage their practices with exceptional efficiency. They can evaluate overhead costs, optimize billing processes, and make informed decisions about equipment purchases or expansion plans. In an era where many private practices struggle to remain financially viable, this combination of skills can be the difference between sustainability and closure.

Beyond practice management, podiatrists with CPA credentials are uniquely positioned to contribute to healthcare policy and administration. They can analyze the financial impact of regulatory changes, assess the cost‑effectiveness of treatment protocols, and participate in leadership roles within hospitals or medical groups. Their ability to interpret financial data gives them a voice in discussions that shape the future of healthcare delivery. They can advocate for reimbursement models that reflect the true value of podiatric care, or design budgeting strategies that improve patient access without compromising quality.

This dual background also enhances patient care in subtle but meaningful ways. A podiatrist who understands the financial side of healthcare can help patients navigate insurance coverage, anticipate out‑of‑pocket costs, and make informed decisions about treatment options. They can design care plans that balance medical necessity with financial feasibility, especially for patients managing chronic conditions that require ongoing attention. In this sense, financial knowledge becomes an extension of patient advocacy.

***

***

The path to becoming both a podiatrist and a CPA is not an easy one. Each field requires years of education, rigorous examinations, and ongoing professional development. The commitment to mastering both disciplines speaks to a mindset of intellectual curiosity and resilience. These individuals are not content with a single lens through which to view their work; they seek a multidimensional understanding of the systems they operate within. This mindset is increasingly valuable in a healthcare environment that demands adaptability and interdisciplinary thinking.

Moreover, the combination of podiatry and accounting reflects a broader trend toward hybrid professional identities. As industries become more interconnected, the most impactful professionals are often those who can bridge gaps between disciplines. A podiatrist‑CPA exemplifies this evolution. They are clinicians who understand balance sheets, business owners who understand anatomy, and problem‑solvers who can approach challenges from both scientific and financial perspectives.

In the future, the healthcare system may see more professionals pursuing dual competencies like this. The pressures of modern medical practice—ranging from reimbursement challenges to the complexities of electronic health records—require a blend of clinical and administrative expertise. While not every podiatrist will become a CPA, the example set by those who do highlights the value of interdisciplinary knowledge. It encourages medical professionals to broaden their skill sets and engage more deeply with the financial and operational aspects of their work.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

A forensic accountant is a financial professional who blends traditional accounting expertise with investigative skills to uncover, analyze, and explain financial irregularities. While many people associate accounting with routine bookkeeping or tax preparation, forensic accounting operates in a very different arena—one where money trails intersect with legal disputes, fraud schemes, and complex financial conflicts. The role requires not only technical knowledge of accounting principles but also the curiosity of an investigator and the clarity of a communicator who can translate intricate financial data into understandable conclusions.

At its core, forensic accounting involves the examination of financial information for use in legal settings. The word “forensic” itself means “suitable for use in court,” which captures the essence of the profession. Forensic accountants are often called upon when financial information must be scrutinized with a level of detail and rigor that can withstand legal scrutiny. Their work may support civil litigation, criminal investigations, insurance claims, business valuations, or internal corporate inquiries. Because of this, they frequently collaborate with attorneys, law enforcement agencies, regulatory bodies, and corporate leadership.

One of the most recognized responsibilities of a forensic accountant is the detection and investigation of fraud. Fraud can take many forms—embezzlement, financial statement manipulation, asset misappropriation, or complex schemes involving shell companies and hidden transactions. Forensic accountants use a combination of analytical procedures, data mining techniques, and professional skepticism to identify patterns that suggest wrongdoing. They may trace the flow of funds through multiple accounts, reconstruct destroyed or incomplete records, or analyze inconsistencies in financial statements. Their goal is not only to uncover what happened but also to determine how it happened and who was responsible.

Beyond fraud detection, forensic accountants play a crucial role in litigation support. In legal disputes involving financial matters, attorneys rely on forensic accountants to provide objective, evidence‑based analysis. This may include calculating economic damages, evaluating the value of a business, assessing lost profits, or determining the financial impact of a breach of contract. In divorce proceedings, forensic accountants may help identify hidden assets or evaluate the true income of a spouse. Their findings often become part of expert reports submitted to the court, and they may be called to testify as expert witnesses. In this capacity, they must present complex financial information in a clear, concise manner that judges and juries can understand.

Another important aspect of forensic accounting is prevention. Organizations increasingly recognize the value of proactive measures to reduce the risk of fraud and financial misconduct. Forensic accountants may design internal controls, conduct risk assessments, or evaluate corporate governance practices to help organizations strengthen their defenses. By identifying vulnerabilities before they are exploited, they contribute to a healthier financial environment and help protect stakeholders from potential losses.

The skill set required for forensic accounting is broad and demanding. Technical proficiency in accounting and auditing is essential, but equally important are analytical thinking, attention to detail, and strong communication skills. Forensic accountants must be able to interpret large volumes of financial data, identify anomalies, and draw logical conclusions. They must also be comfortable working with digital tools, as modern investigations often involve electronic records, data analytics, and specialized software. Integrity and objectivity are critical, given the legal implications of their work and the trust placed in their findings.

The profession also requires adaptability. Every case is different, and forensic accountants must be prepared to navigate unfamiliar industries, evolving fraud techniques, and changing regulatory environments. They may work in public accounting firms, government agencies, law enforcement units, insurance companies, or as independent consultants. Regardless of the setting, the common thread is their role as financial detectives who bring clarity to situations where the truth is obscured by complexity or deception.

In summary, a forensic accountant is far more than a traditional number‑cruncher. They are investigators, analysts, communicators, and trusted advisors who operate at the intersection of finance and law. Their work uncovers hidden truths, supports the pursuit of justice, and helps organizations safeguard their financial integrity. As financial systems grow more complex and fraud schemes become more sophisticated, the role of the forensic accountant continues to expand in importance. Their unique blend of skills makes them indispensable in a world where transparency and accountability are more critical than ever.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

A concept of tax fairness that states that people with different amounts of wealth or different amounts of income should pay tax at different rates. Wealth includes assets such as houses, cars, stocks, bonds, and savings accounts. Income includes wages, interest and dividends, and other payments.

A business authorized by the IRS to participate in the IRS e-file Program. The business may be a sole proprietorship, a partnership, a corporation, or an organization. Authorized IRS e-file Providers include Electronic Return Originators (EROs), Transmitters, Intermediate Service Providers, and Software Developers. These categories are not mutually exclusive. For example, an ERO can at the same time, be a Transmitter, a Software Developer, or an Intermediate Service Provider, depending on the function being performed.

Assuming all other dependency tests are met, the citizen or resident test allows taxpayers to claim a dependency exemption for persons who are U.S. citizens for some part of the year or who live in the United States, Canada, or Mexico for some part of the year.

Amount that taxpayers can claim for a “qualifying child” or “qualifying relative”. Each exemption reduces the income subject to tax. The exemption amount is a set amount that changes from year to year. One exemption is allowed for each qualifying child or qualifying relative claimed as a dependent.

This allows tax refunds to be deposited directly to the taxpayer’s bank account. Direct Deposit is a fast, simple, safe, secure way to get a tax refund. The taxpayer must have an established checking or savings account to qualify for Direct Deposit. A bank or financial institution will supply the required account and routing transit numbers to the taxpayer for Direct Deposit.

The transmission of tax information directly to the IRS using telephones or computers. Electronic filing options include (1) Online self-prepared using a personal computer and tax preparation software, or (2) using a tax professional. Electronic filing may take place at the taxpayer’s home, a volunteer site, the library, a financial institution, the workplace, malls and stores, or a tax professional’s place of business.

Electronic preparation means that tax preparation software and computers are used to complete tax returns. Electronic tax preparation helps to reduce errors.

The Authorized IRS e-file Provider that originates the electronic submission of an income tax return to the IRS. EROs may originate the electronic submission of income tax returns they either prepared or collected from taxpayers. Some EROs charge a fee for submitting returns electronically.

Free from withholding of federal income tax. A person must meet certain income, tax liability, and dependency criteria. This does not exempt a person from other kinds of tax withholding, such as the Social Security tax.

Amount that taxpayers can claim for themselves, their spouses, and eligible dependents. There are two types of exemptions-personal and dependency. Each exemption reduces the income subject to tax. While each is worth the same amount, different rules apply to each.

A program sponsored by the IRS in partnership with participating states that allows taxpayers to file federal and state income tax returns electronically at the same time.

The federal government levies a tax on personal income. The federal income tax provides for national programs such as defense, foreign affairs, law enforcement, and interest on the national debt.

Provides benefits for retired workers and their dependents as well as for disabled workers and their dependents. Also known as the Social Security tax.

To mail or otherwise transmit to an IRS service center the taxpayer’s information, in specified format, about income and tax liability. This information-the return-can be filed on paper, electronically (e-file).

Determines the rate at which income is taxed. The five filing statuses are: single, married filing a joint return, married filing a separate return, head of household, and qualifying widow(er) with dependent child.

Spending and income records and items to keep for tax purposes, including paycheck stubs, statements of interest or dividends earned, and records of gifts, tips, and bonuses. Spending records include canceled checks, cash register receipts, credit card statements, and rent receipts.

A foster child is any child placed with a taxpayer by an authorized placement agency or by court order. Eligible foster children may be claimed by taxpayers for tax benefits.

Money, goods, services, and property a person receives that must be reported on a tax return. Includes unemployment compensation and certain scholarships. It does not include welfare benefits and nontaxable Social Security benefits.

You must meet the following requirements: 1. You are unmarried or considered unmarried on the last day of the year. 2. You paid more than half the cost of keeping up a home for the year. 3. A qualifying person lived with you in the home for more than half the year (except temporary absences, such as school). However, a dependent parent does not have to live with the taxpayer.

Taxes on income, both earned (salaries, wages, tips, commissions) and unearned (interest, dividends). Income taxes can be levied on both individuals (personal income taxes) and businesses (business and corporate income taxes).

Performs services for others. The recipients of the services do not control the means or methods the independent contractor uses to accomplish the work. The recipients do control the results of the work; they decide whether the work is acceptable. Independent contractors are self-employed.

A person who represents the concerns or special interests of a particular group or organization in meetings with lawmakers. Lobbyists work to persuade lawmakers to change laws in the group’s favor.

An economic system based on private enterprise that rests upon three basic freedoms: freedom of the consumer to choose among competing products and services, freedom of the producer to start or expand a business, and freedom of the worker to choose a job and employer.

You are married and both you and your spouse agree to file a joint return. (On a joint return, you report your combined income and deduct your combined allowable expenses.)

You must be married. This method may benefit you if you want to be responsible only for your own tax or if this method results in less tax than a joint return. If you and your spouse do not agree to file a joint return, you may have to use this filing status.

Used to provide medical benefits for certain individuals when they reach age 65. Workers, retired workers, and the spouses of workers and retired workers are eligible to receive Medicare benefits upon reaching age 65.

When the amount of a credit is greater than the tax owed, taxpayers can only reduce their tax to zero; they cannot receive a “refund” for any excess nonrefundable credit.

Allow taxpayers to “sign” their tax returns electronically. The PIN, a five-digit self-selected number, ensures that electronically submitted tax returns are authentic. Most taxpayers can qualify to use a PIN.

Taxes on property, especially real estate, but also can be on boats, automobiles (often paid along with license fees), recreational vehicles, and business inventories.

Benefits that cannot be withheld from those who don’t pay for them, and benefits that may be “consumed” by one person without reducing the amount of the product available for others. Examples include national defense, streetlights, and roads and highways. Public services include welfare programs, law enforcement, and monitoring and regulating trade and the economy.

To be a qualifying child, the dependent must meet eight tests: (1) relationship, (2) age, (3) residence, (4) support, (5) citizenship or residency, (6) joint return, (7) qualifying child of more than one person, and (8) dependent taxpayer.

There are tests that must be met to be a qualifying relative, they are: (1) not a qualifying child, (2) member of household or relationship, (3) citizenship or residency, (4) gross income, (5) support, (6) joint return, and (7) dependent taxpayer.

If your spouse died in 2010, you can use married filing jointly as your filing status for 2010 if you otherwise qualify to use that status. The year of death is the last year for which you can file jointly with your deceased spouse. You may be eligible to use qualifying widow(er) with dependent child as your filing status for two years following the year of death of your spouse. For example, if your spouse died in 2010, and you have not remarried, you may be able to use this filing status for 2011 and 2012. This filing status entitles you to use joint return tax rates and the highest standard deduction amount (if you do not itemize deductions). This status does not entitle you to file a joint return.

Compensation received by an employee for services performed. A salary is a fixed sum paid for a specific period of time worked, such as weekly or monthly.

Similar to Social Security and Medicare taxes. The self-employment tax rate is 15.3 percent of self-employment profit. The self-employment tax is calculated on Schedule SE—Self-Employment Tax. The self-employment tax is reported on Form 1040, U.S. Individual Income Tax Return.

If on the last day of the year, you are unmarried or legally separated from your spouse under a divorce or separate maintenance decree and you do not qualify for another filing status.

Provides benefits for retired workers and their dependents as well as for the disabled and their dependents. Also known as the Federal Insurance Contributions Act (FICA) tax.

Develops software for the purposes of (1) formatting electronic tax return information according to IRS specifications, and/or (2) transmitting electronic tax return information directly to the IRS.

For dependency test purposes, support includes food, clothing, shelter, education, medical and dental care, recreation, and transportation. It also includes welfare, food stamps, and housing provided by the state. Support includes all income, taxable and nontaxable.

Interest income that is not subject to income tax. Tax-exempt interest income is earned from bonds issued by states, cities, or counties and the District of Columbia.

The amount of tax that must be paid. Taxpayers meet (or pay) their federal income tax liability through withholding, estimated tax payments, and payments made with the tax forms they file with the government.

Money and goods received for services performed by food servers, baggage handlers, hairdressers, and others. Tips go beyond the stated amount of the bill and are given voluntarily.

Taxes on economic transactions, such as the sale of goods and services. These can be based on a set of percentages of the sales value (ad valorem-sales taxes), or they can be a set amount on physical quantities (“per unit”-gasoline taxes).

The concept that people in different income groups should pay different rates of taxes or different percentages of their incomes as taxes. “Unequals should be taxed unequally.”

A system of compliance that relies on individual citizens to report their income freely and voluntarily, calculate their tax liability correctly, and file a tax return on time.

This provides free income tax return preparation for certain taxpayers. The VITA program assists taxpayers who have limited or moderate incomes, have limited English skills, or are elderly or disabled. Many VITA sites offer electronic preparation and transmission of income tax returns.

Compensation received by employees for services performed. Usually, wages are computed by multiplying an hourly pay rate by the number of hours worked.

Money, for example, that employers withhold from employees paychecks. This money is deposited for the government. (It will be credited against the employees’ tax liability when they file their returns.) Employers withhold money for federal income taxes, Social Security taxes and state and local income taxes in some states and localities.

Product costing deals with determining the total costs involved in the production of a good or service. Costs may be broken down into subcategories, such as variable, fixed, direct, or indirect costs. Cost accounting is used to measure and identify those costs, in addition to assigning overhead to each type of product created by the company.

Managerial accountants calculate and allocate overhead charges to assess the full expense related to the production of a good. The overhead expenses may be allocated based on the number of goods produced or other activity drivers related to production, such as the square footage of the facility. In conjunction with overhead costs, managerial accountants use direct costs to properly value the cost of goods sold and inventory that may be in different stages of production.

Marginal costing (sometimes called cost-volume-profit analysis) is the impact on the cost of a product by adding one additional unit into production. It is useful for short-term economic decisions. The contribution margin of a specific product is its impact on the overall profit of the company. Margin analysis flows into break-even analysis, which involves calculating the contribution margin on the sales mix to determine the unit volume at which the business’s gross sales equals total expenses. Break-even point analysis is useful for determining price points for products and services.

Cash Flow Analysis

Managerial accountants perform cash flow analysis in order to determine the cash impact of business decisions. Most companies record their financial information on the accrual basis of accounting. Although accrual accounting provides a more accurate picture of a company’s true financial position, it also makes it harder to see the true cash impact of a single financial transaction. A managerial accountant may implement working capital management strategies in order to optimize cash flow and ensure the company has enough liquid assets to cover short-term obligations.

When a managerial accountant performs cash flow analysis, he will consider the cash inflow or outflow generated as a result of a specific business decision. For example, if a department manager is considering purchasing a company vehicle, he may have the option to either buy the vehicle outright or get a loan. A managerial accountant may run different scenarios by the department manager depicting the cash outlay required to purchase outright upfront versus the cash outlay over time with a loan at various interest rates.

Inventory Turnover Analysis

Inventory turnover is a calculation of how many times a company has sold and replaced inventory in a given time period. Calculating inventory turnover can help businesses make better decisions on pricing, manufacturing, marketing, and purchasing new inventory. A managerial accountant may identify the carrying cost of inventory, which is the amount of expense a company incurs to store unsold items.

If the company is carrying an excessive amount of inventory, there could be efficiency improvements made to reduce storage costs and free up cash flow for other business purposes.

Constraint Analysis

Managerial accounting also involves reviewing the constraints within a production line or sales process. Managerial accountants help determine where bottlenecks occur and calculate the impact of these constraints on revenue, profit, and cash flow. Managers then can use this information to implement changes and improve efficiencies in the production or sales process.

Financial Leverage Metrics

Financial leverage refers to a company’s use of borrowed capital in order to acquire assets and increase its return on investments. Through balance sheet analysis, managerial accountants can provide management with the tools they need to study the company’s debt and equity mix in order to put leverage to its most optimal use.

Performance measures such as return on equity, debt to equity, and return on invested capital help management identify key information about borrowed capital, prior to relaying these statistics to outside sources. It is important for management to review ratios and statistics regularly to be able to appropriately answer questions from its board of directors, investors, and creditors.

Accounts Receivable (AR) Management

Appropriately managing accounts receivable (AR) can have positive effects on a company’s bottom line. An accounts receivable aging report categorizes AR invoices by the length of time they have been outstanding. For example, an AR aging report may list all outstanding receivables less than 30 days, 30 to 60 days, 60 to 90 days, and 90+ days.

Through a review of outstanding receivables, managerial accountants can indicate to appropriate department managers if certain customers are becoming credit risks. If a customer routinely pays late, management may reconsider doing any future business on credit with that customer.

Budgeting, Trend Analysis, and Forecasting

Budgets are extensively used as a quantitative expression of the company’s plan of operation. Managerial accountants utilize performance reports to note deviations of actual results from budgets. The positive or negative deviations from a budget also referred to as budget-to-actual variances, are analyzed in order to make appropriate changes going forward.

Managerial accountants analyze and relay information related to capital expenditure decisions. This includes the use of standard capital budgeting metrics, such as net present value and internal rate of return, to assist decision-makers on whether to embark on capital-intensive projects or purchases. Managerial accounting involves examining proposals, deciding if the products or services are needed, and finding the appropriate way to finance the purchase. It also outlines payback periods so management is able to anticipate future economic benefits.

Managerial accounting also involves reviewing the trendline for certain expenses and investigating unusual variances or deviations. It is important to review this information regularly because expenses that vary considerably from what is typically expected are commonly questioned during external financial audits. This field of accounting also utilizes previous period information to calculate and project future financial information. This may include the use of historical pricing, sales volumes, geographical locations, customer tendencies, or financial information.

A Certified Public Accountant (CPA) is a licensed professional who has passed an examination administered by a state’s Board of Accountancy. State CPA exams are created under guidelines issued by The American Institute of Certified Public Accountants (AICPA). The Uniform CPA Exam can only be taken by accountants who already have professional experience in the field and a bachelor’s degree.CPAs are not fiduciaries.

Not all accountants are CPAs. Accountants who are CPAs are licensed by their state’s Board of Accountancy after passing the Uniform CPA Exam. CPAs prepare reports that accurately reflect the business dealings of the companies and individuals that hire them. Many prepare tax returns for individuals or businesses and advise them on ways to minimize taxes. Obtaining the CPA designation requires a bachelor’s degree, typically with a major in business administration, finance, or accounting. Other majors are acceptable if the applicant meets the minimum requirements for accounting courses.

Enrolled Agent

Although not a CPA, an Enrolled Agent [EA] is a person who has earned the privilege of representing taxpayers before the Internal Revenue Service [IRS]. This is done by either passing a three-part comprehensive IRS test covering individual and business tax returns, or through experience as a former IRS employee. Enrolled agent status is the highest credential the IRS awards. Individuals who obtain this elite status must adhere to ethical standards and complete 72 hours of continuing education courses every three years.

Certified Managerial Accountant

A Certified Management Accountant (CMA), which is issued by the Institute of Management Accountants (IMA), builds on financial accounting proficiency by adding management skills that aid in making strategic business decisions based on financial data.

Oftentimes, the reports and analyses prepared by certified management accountants (CMAs) will go above and beyond those required by generally accepted accounting principles (GAAP).

For example, in addition to a company’s required GAAP financial statements, CMAs may prepare additional management reports that provide specific insights useful to corporate decision-makers, such as performance metrics on specific company departments, products, or even employees.

Certified Financial Analyst

A Certified Financial Analyst [CFA] is a globally-recognized professional designation offered by the CFA Institute, an organization that measures and certifies the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management, and security analysis. From 1963 through November 2023, more than 3.7 million candidates had taken the CFA exam. The overall pass rate was 45%. From 2014 through 2023, the 10-year average pass rate was 43%.1

CFA Institute. The CFA Institute was formerly the Association for Investment Management and Research (AIMR).

The CFA charter is one of the most respected designations in finance and is widely considered to be the gold standard in the field of investment analysis. To become a charter holder, candidates must pass three difficult exams, have a bachelors degree, and have at least 4,000 hours of relevant professional experience over a minimum of three years. Passing the CFA Program exams requires strong discipline and an extensive amount of studying.

There are more than 200,000 CFA charter holders worldwide in 164 countries.The designation is handed out by the CFA Institute, which has 11 offices worldwide and 160 local member societies.

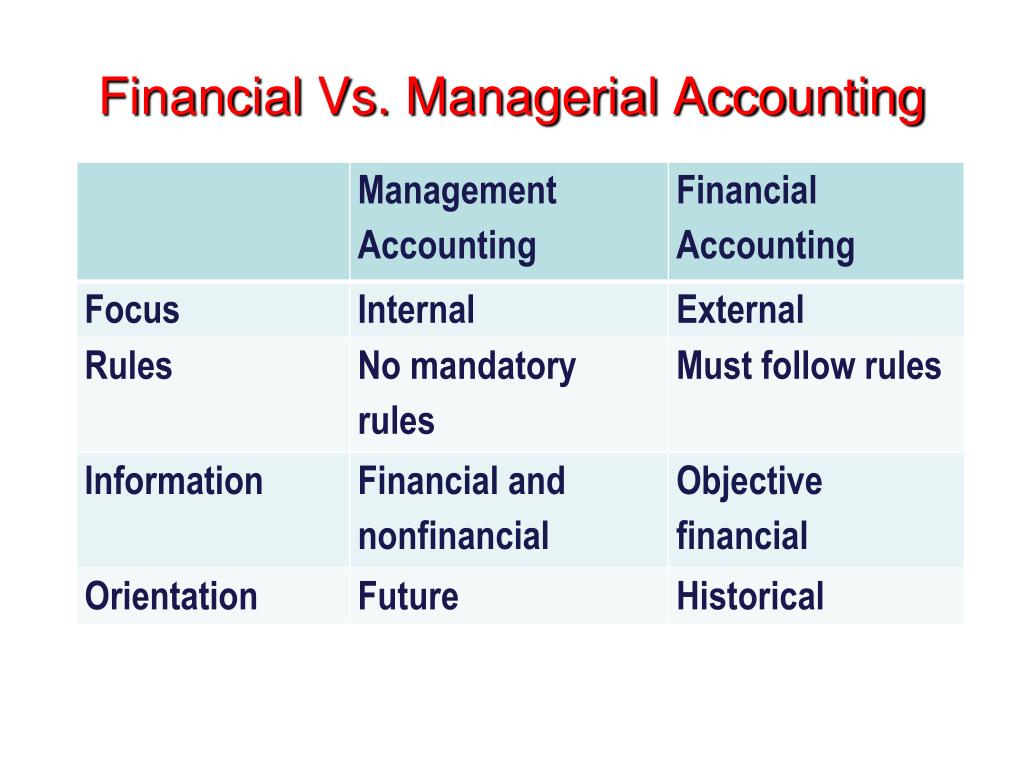

Financial accounting and managerial accounting are two distinct branches of the accounting field, each serving different purposes and stakeholders. Financial accounting focuses on creating external reports that provide a snapshot of a company’s financial health for investors, regulators, and other outside parties. Managerial accounting, meanwhile, is an internal process aimed at aiding managers in making informed business decisions.

Objectives of Financial Accounting

Financial accounting is primarily concerned with the preparation and presentation of financial statements, which include the balance sheet, income statement, and cash flow statement. These documents are meticulously crafted to reflect the company’s financial performance over a specific period, providing insights into its profitability, liquidity, and solvency. The objective is to offer a clear, standardized view of the financial state of the company, ensuring that external entities have a reliable basis for evaluating the company’s economic activities.

The process of financial accounting also involves the meticulous recording of all financial transactions. This is achieved through the double-entry bookkeeping system, where each transaction is recorded in at least two accounts, ensuring that the accounting equation remains balanced. This systematic approach provides accuracy and accountability, which are paramount in financial reporting. CPA = Certified Public Accountant.

Objectives of Managerial Accounting

Managerial accounting is designed to meet the information needs of the individuals who manage organizations. Unlike financial accounting, which provides a historical record of an organization’s financial performance, managerial accounting focuses on future-oriented reports. These reports assist in planning, controlling, and decision-making processes that guide the day-to-day, short-term, and long-term operations.

At the heart of managerial accounting is budgeting. Budgets are detailed plans that quantify the economic resources required for various functions, such as production, sales, and financing. They serve as benchmarks against which actual performance can be measured and evaluated. This enables managers to identify variances, investigate their causes, and implement corrective actions. Another objective of managerial accounting is cost analysis. Managers use cost accounting methods to understand the expenses associated with each aspect of production and operation. By analyzing costs, they can determine the profitability of individual products or services, control expenditures, and optimize resource allocation.

Performance measurement is another key objective. Managerial accountants develop metrics and key performance indicators (KPIs) to assess the efficiency and effectiveness of various business processes. These performance metrics are crucial for setting goals, evaluating outcomes, and aligning individual and departmental objectives with the overall strategy of the organization. CMA = Certified Managerial Accountant

Reporting Standards in Financial Accounting

The bedrock of financial accounting is the adherence to established reporting standards, which ensure consistency, comparability, and transparency in financial statements. Globally, the International Financial Reporting Standards (IFRS) are widely adopted, setting the guidelines for how particular types of transactions and other events should be reported in financial statements. In the United States, the Financial Accounting Standards Board (FASB) issues the Generally Accepted Accounting Principles (GAAP), which serve a similar purpose. These standards are not static; they evolve in response to changing economic realities, stakeholder needs, and advances in business practices.

For instance, the shift towards more service-oriented economies and the rise of intangible assets have led to updates in revenue recognition and asset valuation guidelines. The convergence of IFRS and GAAP is an ongoing process aimed at creating a unified set of global standards that would benefit multinational corporations and investors by reducing the complexity and cost of complying with multiple accounting frameworks.

The CPA and CMA designations cater to distinct professional focuses within the accounting and finance fields. A CPA is often seen as the gold standard for public accounting, emphasizing auditing, tax, and regulatory compliance. This certification is highly regarded for roles that require a deep understanding of financial reporting and external auditing. CPAs are frequently employed by public accounting firms, government agencies, and corporations that need to ensure their financial statements adhere to strict regulatory standards.

On the other hand, the CMA designation is tailored for professionals who aim to excel in management accounting and strategic financial management. CMAs are trained to analyze financial data to inform business decisions, focusing on internal processes and performance management. This makes the CMA particularly valuable for roles in corporate finance, strategic planning, and management consulting. Companies looking to optimize their internal financial operations and drive business strategy often seek out CMAs for their expertise in cost management, budgeting, and financial analysis.

The educational and experiential requirements for these certifications also differ. To become a CPA, candidates typically need to complete 150 semester hours of college education, which often includes a bachelor’s degree in accounting or a related field. Additionally, CPAs must pass the Uniform CPA Examination and meet specific state licensing requirements, which usually include a certain amount of professional experience.

In contrast, the CMA certification requires a bachelor’s degree in any discipline, two years of relevant work experience, and passing the two-part CMA exam. This flexibility in educational background can make the CMA more accessible to a broader range of professionals.

Managerial and medical cost accounting is not governed by generally accepted accounting principles (GAAP) as promoted by the Financial Accounting Standards Board (FASB) for CPAs. Rather, a healthcare organization costing expert may be a Certified Cost Accountant (CCA) or Certified Managerial Accountant (CMA) designated by the Cost Accounting Standards Board (CASB), an independent board within the Office of Management and Budget’s (OMB) Office of Federal Procurement Policy (OFPP).

The Cost Accounting Standards Board

CASB consists of five members, including the OFPP Administrator who serves as chairman and four members with experience in government contract cost accounting (two from the federal government, one from industry, and one from the accounting profession). The Board has the exclusive authority to make, promulgate, and amend cost accounting standards and interpretations designed to achieve uniformity and consistency in the cost accounting practices governing the measurement, assignment, and allocation of costs to contracts with the United States.

Codified at 48 CFR

CASB’s regulations are codified at 48 CFR, Chapter 99. The standards are mandatory for use by all executive agencies and by contractors and subcontractors in estimating, accumulating, and reporting costs in connection with pricing and administration of, and settlement of disputes concerning, all negotiated prime contract and subcontract procurement with the United States in excess of $500,000. The rules and regulations of the CASB appear in the federal acquisition regulations.

North American Industry Classification System (NAICS) codes are used to categorize data for the federal government. In acquisition they are particularly critical for size standards. The NAICS codes are revised every five years by the Census Bureau. As of October 1, 2007, the federal acquisition community began using the 2007 version of the NAICS codes at www.census.gov/epcd/www/naics.html

Cost Accounting Standards

Healthcare organizations and consultants are obligated to comply with the following cost accounting standards (CAS) promulgated by federal agencies:

CAS 501 requires consistency in estimating, accumulating, and reporting costs.

CAS 502 requires consistency in allocating costs incurred for the same purpose.

CAS 505 requires proper treatment of unallowable costs.

CAS 506 requires consistency in the periods used for cost accounting.

The requirements of these standards are different from those of traditional financial accounting, which are concerned with providing static historical information to creditors, shareholders, and those outside the public or private healthcare organization.

Assessment

Functionally, most healthcare organizations also contain cost centers, which have no revenue budgets or mission to earn revenues for the organization. Examples include human resources, administration, housekeeping, nursing, and the like. These are known as responsibility centers with budgeting constraints but no earnings. Furthermore, shadow cost centers include certain non-cash or cash expenses, such as amortization, depreciation and utilities, and rent. These non-centralized shadow centers are cost allocated for budgeting purposes and must be treated as costs http://www.CertifiedMedicalPlanner.org

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on August 16, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Aleksandar Stojanović, MSc

Here’s a brief insight before the explanations:

𝗖𝗙𝗢𝘀 are heavily invested in strategic planning, leadership, and risk management, often overlooking the entire financial spectrum.

𝗖𝗼𝗻𝘁𝗿𝗼𝗹𝗹𝗲𝗿𝘀 play a key role in accounting, financial reporting, and regulatory compliance, ensuring financial integrity.

𝗙𝗣&𝗔 𝗠𝗮𝗻𝗮𝗴𝗲𝗿𝘀 focus on financial modeling, analytical skills, and business acumen to drive business growth.

𝗜𝗻𝘁𝗲𝗿𝗻𝗮𝗹 𝗔𝘂𝗱𝗶𝘁𝗼𝗿𝘀 specialize in risk management, regulatory compliance, and analytical tasks to ensure internal control.

𝗙𝗶𝗻𝗮𝗻𝗰𝗲 𝗔𝗻𝗮𝗹𝘆𝘀𝘁𝘀 are adept at financial modeling, analytics, and reporting to support data-driven decisions.

𝗔𝗰𝗰𝗼𝘂𝗻𝘁𝗮𝗻𝘁𝘀 emphasize accounting skills, financial reporting, and regulatory compliance for precise record-keeping.

***

***

Now, generally, CFOs and FP&A Managers might spend more time connecting to business stakeholders for strategic decisions, while Controllers and Internal Auditors focus more on regulatory and compliance tasks.

Finance Analysts and Accountants are more involved in financial modeling and reporting.

These titles and responsibilities can be interchanged in some job descriptions, and the weight of these skills also depends on the industry and project.

But this breakdown is still quite helpful when planning career paths or understanding the roles within a finance department.

Posted on August 31, 2009 by Dr. David Edward Marcinko MBA MEd CMP™

Join Us!

By Ann Miller; RN, MHA

[Executive Director]

Perhaps you have a great idea for a short article to promote the integration of personal financial planning and medical practice management, including expert posts, humorous stories or interesting news; but don’t want to maintain a blog? We have more than 50 topic channels to consider.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Subscribe Now: Did you like this Medical Executive-Post, or find it helpful, interesting and informative? Want to get the latest ME-Ps delivered to your email box each morning? Just subscribe using the link below. You can unsubscribe at any time. Security is assured.

Posted on August 3, 2009 by Dr. David Edward Marcinko MBA MEd CMP™

A New ME-P Thought-Leader

By Ann Miller; RN, MHA

[Executive Director]

Brian J Knabe MD is a financial advisor with Savant Capital Management www.SavantCapital.com. He uses his experience from the medical field in his work with clients, portfolio managers, physicians and other financial advisors to develop comprehensive planning, investment, and tax strategies for professionals.

Medical and Financial Background

Brian is a magna cum laude graduate of Marquette University with an honors degree in biomedical engineering. He earned his medical degree from the University Illinois College of Medicine. Brian also attended the University of Illinois for his family practice residency, where he served as chief resident. Brian is currently pursuing his Certified Financial Planner (CFP®) designation, and he recently passed the exam.

Certified Medical Planner™

Dr. Knabe is also matriculating in the online www.CertifiedMedicalPlanner.org [CMP™] charter-designation program for financial advisors and medical management consultants, from the Institute of Medical Business Advisors, Inc.

Personal Background

As if the above were not enough to keep him busy, Brian is also a clinical assistant professor in the Department of Family Medicine with the University of Illinois. He is a member of several professional organizations, including the American Academy of Family Physicians, the American Medical Association [AMA], and the Catholic Medical Association. Brian has also served as the vice president of membership for the Blackhawk Area Council of the Boy Scouts of America.

Our Congratulations

And so, we trust all ME-P readers will give a congratulatory “shout-out” to Brian J. Knabe MD, our newest “thought-leader.” Read his position paper here:

Evidence Based Investing [A Scientific Framework for the Art of Investing]

We trust we will hear much more from him in the future.

Conclusion

And so, your thoughts and comments on this Medical Executive-Post are appreciated. Tell us what you think about the credentials of Dr. Knabe. Is this extreme education a new-wave of fiduciary focus for all financial advisors and planners in the healthcare space? Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, be sure to subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Our Other Print Books and Related Information Sources:

Subscribe Now: Did you like this Medical Executive-Post, or find it helpful, interesting and informative? Want to get the latest ME-Ps delivered to your email box each morning? Just subscribe using the link below. You can unsubscribe at any time. Security is assured.