![]()

UPCOMING: Our Newest Major Textbook Release

[By Ann Miller RN MHA]

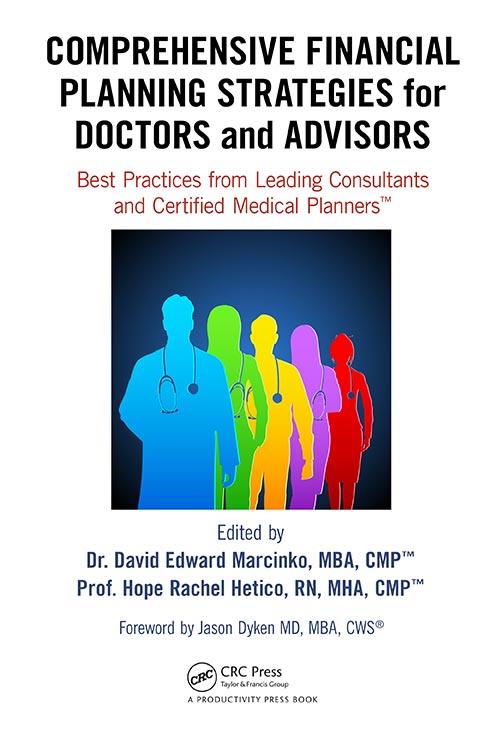

Release: February 19th, 2015 by Productivity Press, Inc

744 Pages | 43 Illustrations

Editor(s): Dr. David Edward Marcinko MBA CMP™ and Professor Hope Rachel Hetico RN MHA CMP™

***

COMPREHENSIVE FINANCIAL PLANNING STRATEGIES for DOCTORS and ADVISORS

[Best Practices from Leading Consultants and

Certified Medical Planners™]

Features:

- Engaging content with case models, templates and examples for all medical professionals and their consulting advisors.

- Combines holistic financial planning with new topics like hedge funds, investment banking, Wall Street practices and shenanigans; securities markets and margin accounts; alternative asset classes and investment policy creation – all integrated with emerging health industry concerns like the PP-ACA, ACOs, new tax laws and reimbursement models; practice sales, contracting and valuations; social media, hospital employee fringe benefits and PHO stock options.

- Presents disruptive theories on industry suitability rules, fiduciary accountability and stewardship principles, and how to select the most knowledgeable and cost-efficient advisor for every life-cycle need.

Summary

Drawing on the expertise of multi-degreed doctors, and multi-certified financial advisors, COMPREHENSIVE FINANCIAL PLANNING STRATEGIES FOR DOCTORS AND ADVISORS[Best Practices from Leading Consultants and Certified Medical Planners™]will shape the industry landscape for the next-generation as the current ecosystem strives to keep pace. Traditional generic products and sales-driven advice will yield to a new breed of deeply informed financial advisor, or Certified Medical Planner™.

The profession is set to be transformed by “cognitive-disruptors” that will significantly impact the $2.8 trillion healthcare marketplace for those financial consultants serving this challenging sector. There will be winners and losers. The text which contains 24 chapters, and champions healthcare providers while informing financial advisors, is divided into four sections compete with glossary of terms, CMP™ curriculum content, and related information sources:

- For ALL medical providers and financial industry practitioners

- For NEW medical providers and financial industry practitioners

- For MID-CAREER medical providers and financial industry practitioners

- For MATURE medical providers and financial industry practitioners.

Using an engaging style, the book is filled with authoritative guidance and health care–centered discussions, to provide tools and techniques to create a personalized financial plan using professional advice. Comprehensive coverage includes topics likes behavioral finance, medical risk management, Modern Portfolio Theory (MPF), the Capital Asset Pricing Model (CAP-M) and Arbitrage Pricing Theory (APT); as well as insider insights on commercial real estate; High Frequency Trading platforms and robo-advisors; the Patriot and Sarbanes–Oxley Acts; hospital endowment fund management, ethical wills, divorce and other special situations.

The result is a codified “must-have” book, for all health industry participants, and those seeking advice from the growing cadre of financial consultants and Certified Medical Planners™ who seek to “do well – by doing good”, dispensing granular physician-centric financial advice: Omnia pro medicus-clientis.

RAISING THE BAR

CERTIFIED MEDICAL PLANNER™

“The informed voice of a new generation of fiduciary advisors for healthcare”

[Omnia pro medicus-clientis]

More:

- Enter the CMPs

- Arkansas Medical News Interviews Dr. Marcinko

- http://www.CertifiedMedicalPlanner.org

- Table of Contents: http://www.crcpress.com/product/isbn/9781482240283

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Link: http://feeds.feedburner.com/HealthcareFinancialsthePostForcxos

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

- DICTIONARIES: http://www.springerpub.com/Search/marcinko

- PHYSICIANS: www.MedicalBusinessAdvisors.com

- PRACTICES: www.BusinessofMedicalPractice.com

- HOSPITALS: http://www.crcpress.com/product/isbn/9781466558731

- CLINICS: http://www.crcpress.com/product/isbn/9781439879900

- ADVISORS: www.CertifiedMedicalPlanner.org

- BLOG: www.MedicalExecutivePost.com

- FINANCE:Financial Planning for Physicians and Advisors

- INSURANCE:Risk Management and Insurance Strategies for Physicians and Advisors

![]()

![]()

![]()

8

8

Share this:

Filed under: "Advisors Only", "Doctors Only", Book Reviews, Breaking News, Career Development, CMP Program, Financial Planning | Tagged: certified medical planner, CMP, david marcinko, Financial Planning, hope hetico | 6 Comments »