By Staff Reporters

***

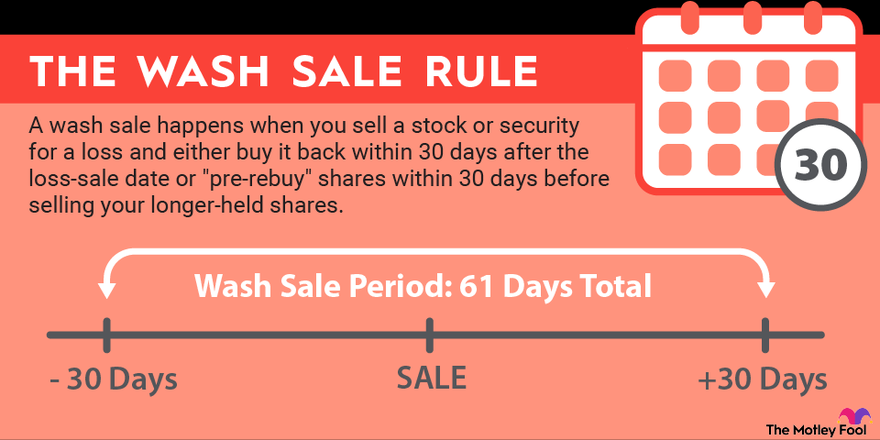

DEFINITION

The wash-sale rule prohibits selling an investment for a loss and replacing it with the same or a “substantially identical” investment 30 days before or after the sale. If you do have a wash sale, the IRS will not allow you to write off the investment loss which could make your taxes for the year higher than you hoped.

CITE: https://www.r2library.com/Resource/Title/082610254

***

***

Don’t get soaked by the wash sale

Even if you sell at a loss from a brokerage account or IRA, it still might not want to permanently exit a portfolio position. It may want to get back into an investment now at a cheaper cost with room to re-grow.

BUT – Just wait a moment, according to the IRS “wash-sale” rule.

The IRS will not count a capital loss if, within 30 days before the sale or within 30 days afterwards, the taxpayer is also buying or acquiring a “substantially identical” investment. The rule applies to investments like stocks, bonds, mutual funds, exchange traded funds and options – but not cryptocurrency.

The basic trick is just keeping track of the days. Another skill is considering what counts as “substantially identical” for the fast-moving investor who sees a buying opportunity either 30 days before or after the day of sale.

An investor could sell a stock and buy an exchange traded fund or mutual fund that contains the stock and not run afoul of the rule, Going the other way, from a mutual fund or ETF containing a stock to a direct stock purchase, also will not trigger the rule, he noted.

EXAMPLE: Suppose an investor has several investment accounts — perhaps one is a long-term account and the other is more for short-term trades. The rule applies across the account. So if one sells and the other buys within 30 days before or after, the wash-sale rule will scrap the capital loss.

Buying and selling shares of two different funds tracking the same index within the 30-day period could also cause the wash sale rule to kick in. However, a move like selling a piece of an ETF tracking the S&P 500, and then soon buying an ETF tracking the Russell 1000 Index would be OK according to a tutorial from Charles Schwab SCHW, +3.70%. “That would preserve your tax break and keep you in the market with about the same asset allocation,” an explainer said.

But while someone’s eyeing a repurchase and letting the wash-sale window close one place, they may have a chance to start the tax strategy process in a different part of their portfolio. “There’s really tax loss harvesting opportunities across a number of different asset classes this year.”

***

COMMENTS APPRECIATED

Thank You

***

***

Share this:

Filed under: "Ask-an-Advisor", Funding Basics, Glossary Terms, Investing | Tagged: crypto, cryptocurrency, WASH RULE: Not For Cryptocurrency?, wash sale, wash sale crypto, wash sale rule | 1 Comment »