BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Sometimes debt is a necessary tool in building wealth

Using debt to build wealth might seem counterintuitive. After all, when you calculate your wealth, you look at what you own (assets) and subtract what you owe (debts and liabilities) to determine what your net worth (wealth) is.

It’s easy to oversimplify that debt is bad and is harmful to your wealth. Because some debt is really harmful, like credit cards, automobile, debt gets lumped into the category of “bad.”

But some types of debt can be useful and sometimes necessary to create wealth; home, education, business, etc. For folks that don’t readily have access to large sums of cash or capital, debt may be the tool that allows them to expand.

According to Medical Economics, there were 10 clinic and physician practices filing bankruptcy in 2024, making it the highest level of the last six years, according to a new analysis of cases with liabilities of at least $10 million.

Meanwhile, the Steward Health Care System bankruptcy, which was based in Massachusetts but making headlines across the nation, has become “the largest hospital sector bankruptcy by far in the last 30 years,” according to a new analysis by Gibbins Advisors, based in Nashville, Tennessee.

Health care bankruptcy filings totaled 57 last year, down from 79 in 2023, said “Healthcare Restructuring: Trends and Outlook.” The report analyzed Chapter 11 health care bankruptcy cases with liabilities of at least $10 million, since 2019.

Last year’s total was down 28% from 2023’s peak, but greater than the 2019 to 2022 average of 42 filings a year, the report said.

Bankruptcy, often considered a last financial resort, is a legal process that can help alleviate outstanding debts for individuals and businesses. Reasons to file for bankruptcy can include divorce, job loss, exorbitant medical bills or credit card debt.

There are several types of bankruptcy — six, as a matter of fact. The two most common types of bankruptcy for individuals are Chapter 7 and Chapter 13.

But there are four other types as well: Chapter 9, Chapter 11, Chapter 12 and Chapter 15. And, the type of bankruptcy filed depends on the situation.

Regardless of which type, the process is typically the same: You’ll usually retain an attorney and make your case before a judge, who will then erase some debts or set up a repayment plan.

Also note that an eligibility requirement — for all bankruptcy chapters — is that you must undergo credit counseling within the 180 days before filing.

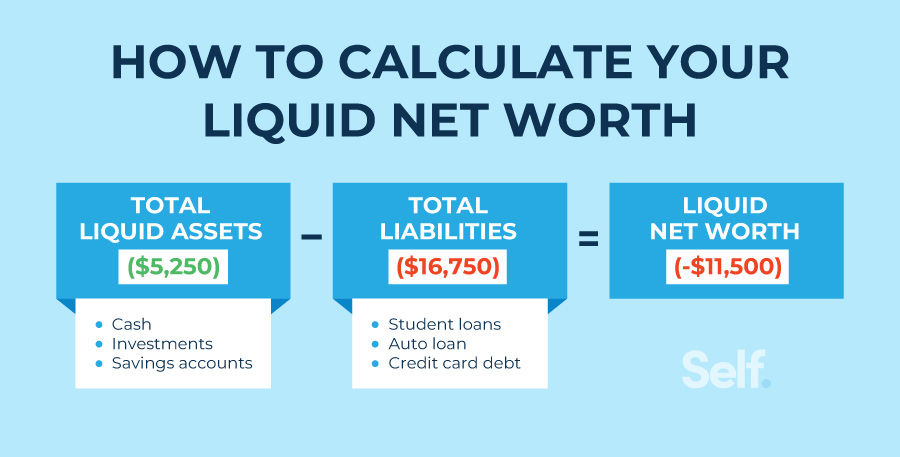

Net worth is everything you own of significance (Assets) minus what is owed in debts (Liabilities). Assets include cash and investments, real estate, cars and anything else of value.

How is net worth calculated? Assets – Debt = Net Worth. Net worth is calculated by adding all owned assets (anything of value) and then subtracting all of your liabilities.

Is net worth yearly? No, net worth is not yearly. Net worth isn’t inherently yearly but is often tracked on an annual basis to assess financial progress year over year.

What net worth is considered wealthy, rich and upper class? In the U.S. salary average is around $59,000, and only 20% of Americans have a household income of $100,000 or more.

Is net worth the same as net income? No, net worth is not the same as net income. Net income is what you actually bring home after taxes and payroll deductions, like Social Security and 401(k) contributions.

Can one measure their net worth if they don’t have many assets or a high income? Yes. Knowing your net worth isn’t about the amount you have; it’s about understanding your financial position. It helps you track your progress, informs your financial decisions, and motivates you to improve your financial health, regardless of where you start.

Posted on December 19, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Austerity Financial Measures describe official actions (typically taken under duress) by financially challenged governments (those that are under the threat of otherwise not being able to meet all of their obligations to debt holders and other creditors) to reduce the amount of money they spend, freeing more of it for paying off liabilities.

Austerity measures commonly involve deficit cutting, reduced spending, and cuts in government benefits and services provided. They are considered a “necessary evil,” along with revenue-raising measures, for bringing government budgets back into financial balance.

Once the value of all personal assets and liabilities is known, net worth can be determined with the following formula: Net worth = assets minus liabilities. Obviously, higher is better.

In The Millionaire Next Door, Thomas H. Stanley, PhD, and William H. Danko give the following benchmark for net worth accumulation. Although conservative for physicians of a past generation, it may be more applicable in the future because of current managed care environment. Here is the guide: Multiple your age by your annual pre-tax income from all sources; except inheritances, and then divide by ten.

Example:

As an HMO pediatrician, Dr. Curtis earned $ 90,000 last year. So, if she is 35, her net worth should be at least $ 315,000.

How do you get to that point? In a word, consume less and save more. Stanley and Danko found that the typical millionaire set aside 15 percent of earned income annually and has enough invested to survive 10 years, at current income levels if he stopped working.

Question: If Dr. Curtis lost her job tomorrow, how long could she pay herself the same salary? Could you?