BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on December 31, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

Synthetic stocks represent one of the most intriguing innovations in contemporary financial markets. Unlike traditional shares, which grant direct ownership in a company, synthetic stocks are financial instruments designed to mimic the behavior of real stocks without requiring investors to actually hold the underlying asset. They are created through derivatives, contracts, or blockchain-based mechanisms that replicate the price movements and returns of equities. This concept has gained traction as technology reshapes investing, offering new opportunities and challenges for both retail and institutional participants.

What Are Synthetic Stocks?

At their core, synthetic stocks are contracts that simulate the performance of a real stock. For example, if a company’s share price rises by 10 percent, the synthetic version of that stock would also increase by the same amount. Investors gain exposure to the asset’s price movements, dividends, or other features without owning the actual shares. These instruments can be built using options, swaps, or tokenized assets on blockchain platforms. The goal is to provide flexibility and accessibility, especially in markets where direct ownership may be restricted or costly.

Advantages of Synthetic Stocks

Synthetic stocks offer several benefits that make them appealing to modern investors:

Accessibility: They allow individuals in regions with limited access to U.S. or global equities to participate in those markets.

Fractional Ownership: Synthetic instruments can be divided into smaller units, enabling investors to buy exposure to expensive stocks like Tesla or Amazon without needing large sums of capital.

Liquidity: Because they are often traded on digital platforms, synthetic stocks can provide faster and more efficient transactions.

Customization: Investors can tailor synthetic contracts to include specific features, such as dividend replication or leverage, depending on their risk appetite.

These advantages highlight how synthetic stocks democratize investing, making global markets more inclusive.

Risks and Challenges

Despite their promise, synthetic stocks also carry significant risks.

Counterparty Risk: Since synthetic instruments are contracts, investors rely on the issuer to honor obligations. If the issuer defaults, the investor may lose their capital.

Regulatory Uncertainty: Many jurisdictions are still grappling with how to classify and regulate synthetic assets, especially those built on blockchain. This creates potential legal and compliance challenges.

Market Volatility: Synthetic stocks mirror the volatility of real equities, meaning investors are still exposed to sharp price swings.

Complexity: Understanding the mechanics of synthetic instruments requires financial literacy. Without proper knowledge, retail investors may face unexpected losses.

These challenges underscore the importance of caution and education when engaging with synthetic markets.

***

***

Synthetic Stocks and Blockchain

One of the most exciting developments in synthetic stocks is their integration with blockchain technology. Platforms can issue tokenized versions of real equities, allowing investors to trade synthetic shares 24/7 across borders. Smart contracts automate dividend payments or price tracking, reducing reliance on intermediaries. This innovation not only enhances transparency but also expands access to markets previously limited by geography or regulation. However, blockchain-based synthetic stocks also raise questions about investor protection, taxation, and systemic risk.

The Future of Synthetic Stocks

Looking ahead, synthetic stocks are likely to play a growing role in global finance. As regulators establish clearer frameworks, these instruments could become mainstream tools for portfolio diversification. They may also serve as bridges between traditional finance and decentralized finance (DeFi), blending the stability of established markets with the innovation of digital platforms. For institutional investors, synthetic stocks could provide efficient hedging strategies, while retail investors may use them to gain exposure to assets that were once out of reach.

Conclusion

Synthetic stocks embody the evolving nature of financial markets in the digital age. By replicating the performance of real equities, they expand access, flexibility, and innovation for investors worldwide. Yet they also introduce new risks that require careful management and regulatory oversight. As technology continues to reshape finance, synthetic stocks stand as a symbol of both opportunity and caution. They remind us that while markets evolve, the balance between innovation and responsibility remains essential. For investors willing to learn and adapt, synthetic stocks may represent not just a trend, but a transformative force in the future of investing.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on December 30, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

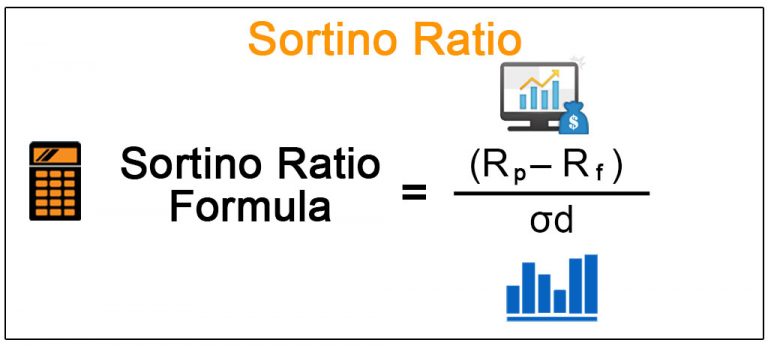

In the field of investment analysis, one of the most important challenges is balancing risk and reward. Investors want to maximize returns, but they also want to minimize the chances of losing money. Traditional measures such as the Sharpe Ratio have long been used to evaluate risk‑adjusted performance, but they treat all volatility the same. This means that both upward and downward swings in returns are penalized equally, even though investors generally welcome upside volatility. To address this limitation, the Sortino Ratio was developed as a more refined tool that focuses specifically on downside risk.

Definition and Formula

The Sortino Ratio measures the excess return of an investment relative to the risk‑free rate, divided by the standard deviation of negative returns. In formula form:

σd\sigma_d = standard deviation of downside returns

This formula highlights the unique feature of the Sortino Ratio: it only considers harmful volatility, ignoring fluctuations that exceed expectations.

Why It Matters

The key advantage of the Sortino Ratio is its ability to separate “good” volatility from “bad” volatility. Upside volatility, which represents returns above the target or minimum acceptable rate, is not penalized. Downside volatility, which represents returns below expectations, is penalized heavily. This distinction makes the Sortino Ratio especially useful for investors who prioritize capital preservation. For example, retirees or individuals saving for short‑term goals may prefer investments with higher Sortino Ratios because they indicate stronger protection against losses.

Practical Applications

The Sortino Ratio has several practical uses:

Portfolio Evaluation: Investors can compare funds or strategies using the Sortino Ratio. A higher ratio suggests better risk‑adjusted performance.

Risk Management: By focusing on downside deviation, managers can identify investments that minimize losses during downturns.

Goal‑Oriented Investing: For individuals with specific financial targets, the Sortino Ratio helps ensure that chosen investments align with their tolerance for risk.

For instance, a mutual fund with a Sortino Ratio of 2 is generally considered strong, meaning it generates twice the return per unit of downside risk.

Comparison with the Sharpe Ratio

While both the Sharpe and Sortino Ratios measure risk‑adjusted returns, they differ in how they treat volatility. The Sharpe Ratio penalizes all fluctuations, whether positive or negative. The Sortino Ratio, however, only penalizes harmful volatility. This makes the Sortino Ratio more investor‑friendly, especially for those who care more about avoiding losses than capturing every possible gain. In practice, the Sharpe Ratio is better for broad comparisons across asset classes, while the Sortino Ratio is better for evaluating downside protection in portfolios.

Limitations

Despite its strengths, the Sortino Ratio is not without limitations:

Data Sensitivity: It requires accurate downside deviation data, which can be difficult to calculate.

Threshold Choice: Results vary depending on the minimum acceptable return chosen.

Context Dependence: It should be used alongside other metrics, such as the Sharpe or Treynor Ratios, for a complete picture of risk and return.

Conclusion

The Sortino Ratio is a powerful tool for investors who want to measure performance while minimizing exposure to harmful volatility. By focusing exclusively on downside risk, it provides a more realistic assessment of whether returns justify the risks taken. While not perfect, it complements other risk‑adjusted metrics and is especially valuable for investors with low tolerance for losses. In today’s uncertain markets, understanding and applying the Sortino Ratio can help investors make smarter, more resilient decisions.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on December 30, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

***

***

Trading in metal markets Monday hit the brakes on a year-end rally, sending silver futures to their steepest one-day decline in almost five years.

Investors dropped commodities key to everything from central-bank reserves to the infrastructure build-out linked to the A.I. boom. The selloff in copper and precious-metals futures dragged down shares in Arizona mining firms, the world’s largest gold producer and a silver company with assets stretching from Alaska to Quebec.

Key to electrical wiring running through data centers and power lines, copper fell 4.8%. Gold retreated 4.5%, while silver plunged 8.7%. All three remain near record prices after a dizzying 2025 climb, and in London trading, copper hit another all-time high on Monday.

In the world of accounting and finance, three concepts often arise when discussing the treatment of assets and expenses: amortization, depreciation, and capitalization. While they are related in the sense that they all deal with how costs are recognized over time, each serves a distinct purpose and applies to different types of assets. Understanding the differences among them is essential for accurate financial reporting, effective business decision-making, and compliance with accounting standards.

Capitalization: Recording Costs as Assets

Capitalization is the process of recording a cost as an asset rather than an immediate expense. When a company incurs a significant expenditure that is expected to provide benefits over multiple years, it does not reduce its income statement right away. Instead, the expenditure is placed on the balance sheet as an asset. This approach reflects the principle that expenses should be matched with the revenues they help generate.

For example, if a business purchases machinery, the cost is capitalized because the machine will contribute to production for several years. Similarly, software development costs or construction of a new building may be capitalized. By doing so, the company acknowledges that the expenditure is not consumed in a single period but rather represents a resource that will yield value over time. Capitalization thus serves as the starting point for both depreciation and amortization, since once an asset is capitalized, its cost must be systematically allocated across its useful life.

Depreciation: Allocating the Cost of Tangible Assets

Depreciation refers to the systematic allocation of the cost of tangible fixed assets over their useful lives. Tangible assets include items such as buildings, vehicles, machinery, and equipment. Because these assets wear out, become obsolete, or lose value through usage, depreciation ensures that the expense is recognized gradually rather than all at once.

There are several methods of calculating depreciation, such as straight-line, declining balance, or units of production. The straight-line method spreads the cost evenly across the asset’s useful life, while the declining balance method accelerates the expense recognition, reflecting higher usage or loss of value in earlier years. The units of production method ties depreciation directly to output, making it particularly useful for machinery or equipment whose wear and tear is closely linked to usage.

Depreciation not only affects the income statement by reducing reported profits but also impacts the balance sheet by lowering the book value of assets. Importantly, depreciation is a non-cash expense; it does not involve an outflow of cash but rather represents the allocation of a previously capitalized cost. This distinction is crucial for understanding cash flow versus net income.

***

***

Amortization: Spreading the Cost of Intangible Assets

Amortization is conceptually similar to depreciation but applies to intangible assets rather than tangible ones. Intangible assets include patents, trademarks, copyrights, goodwill, and software. These assets do not have physical substance, but they still provide economic benefits over time. Amortization ensures that the cost of acquiring or developing such assets is recognized gradually across their useful lives.

Like depreciation, amortization can be calculated using different methods, though the straight-line method is most common for intangibles. For example, if a company acquires a patent with a legal life of 20 years, the cost of the patent is amortized evenly over that period. In some cases, intangible assets may have indefinite lives, such as goodwill. These assets are not amortized but are instead tested periodically for impairment, meaning their value is assessed to determine whether it has declined.

Amortization, like depreciation, is a non-cash expense. It reduces reported income but does not affect cash flow directly. It also lowers the book value of intangible assets on the balance sheet, ensuring that financial statements reflect a realistic valuation of the company’s resources.

***

***

Comparing the Three Concepts

While capitalization, depreciation, and amortization are interconnected, they differ in scope and application:

Capitalization is the initial step, determining whether a cost should be treated as an asset rather than an expense.

Depreciation applies to tangible assets, allocating their cost over time as they are used or lose value.

Amortization applies to intangible assets, spreading their cost across their useful lives.

Together, these processes ensure that financial statements present a fair and consistent picture of a company’s financial position. They embody the matching principle in accounting, which requires that expenses be recognized in the same period as the revenues they help generate.

Importance in Business Decision-Making

The treatment of costs through capitalization, depreciation, and amortization has significant implications for businesses. Capitalizing expenditures can improve short-term profitability by deferring expense recognition, but it also increases assets and future obligations to recognize depreciation or amortization. Depreciation and amortization, meanwhile, affect reported earnings and can influence decisions about investment, financing, and taxation.

For managers, understanding these concepts is critical when evaluating the financial health of the company. For investors, they provide insight into how efficiently a company is using its resources and whether its reported profits are sustainable. For regulators and auditors, they ensure compliance with accounting standards and prevent manipulation of financial results.

Conclusion

Amortization, depreciation, and capitalization are fundamental accounting concepts that shape how businesses record and report their financial activities. Capitalization determines whether a cost becomes an asset, depreciation allocates the cost of tangible assets, and amortization spreads the cost of intangible assets. Though distinct, they work together to ensure that expenses are matched with revenues, assets are valued realistically, and financial statements provide meaningful information. Mastery of these concepts is essential not only for accountants but also for managers, investors, and anyone seeking to understand the financial dynamics of a business.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on December 29, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd

***

***

Introduction

In the world of finance and accounting, time is not merely a backdrop but a critical dimension that shapes how information is recorded, interpreted, and acted upon. The concept of a financial time range—expressed through accounting periods, fiscal years, and financial quarters—provides the framework for organizing economic activity into manageable segments. Without such ranges, businesses would struggle to measure performance, investors would lack comparability, and regulators would face difficulties in enforcing transparency. This essay explores the meaning, types, and importance of financial time ranges, while also considering their implications for decision-making.

Definition and Purpose A financial time range is essentially the span of time covered by financial statements. It defines the boundaries within which transactions are accumulated, summarized, and reported. For example, an accounting period may be one month, one quarter, or one year. By establishing these ranges, businesses ensure that financial data is timely, relevant, and comparable. Stakeholders rely on this consistency to evaluate trends, assess risks, and make informed decisions.

Types of Financial Time Ranges

Accounting periods: Specific intervals—monthly, quarterly, or annually—used to prepare financial statements. They allow managers to monitor performance regularly and adjust strategies accordingly.

Fiscal years: Unlike calendar years, fiscal years can begin and end at any point, depending on the company’s preference.

Financial quarters: Companies often divide their fiscal year into four quarters, each lasting three months. This practice is especially important for firms that report quarterly earnings.

Annual reporting: At the end of each fiscal year, businesses prepare comprehensive financial statements, which provide a holistic view of performance.

Importance of Financial Time Ranges The significance of financial time ranges lies in their ability to impose structure on the continuous flow of transactions. Key benefits include:

Comparability: Results can be compared across successive periods, identifying growth patterns or declines.

Timeliness: Regular reporting ensures that information is available when decisions need to be made.

Accountability: Defined ranges allow regulators and shareholders to hold management responsible for performance.

Strategic planning: Managers use financial ranges to forecast, budget, and allocate resources effectively.

Global Variations and Challenges Financial time ranges are not uniform across the globe. While many organizations follow the calendar year, others adopt fiscal years that align with tax regulations or industry cycles. This diversity can complicate cross-border comparisons, requiring adjustments in analysis. Moreover, technological advancements now allow for real-time financial tracking, raising questions about whether traditional ranges remain sufficient in a digital economy.

Conclusion

The financial time range is more than a technical detail; it is a cornerstone of modern financial systems. By segmenting time into accounting periods, fiscal years, and quarters, businesses create a rhythm of reporting that supports transparency, comparability, and accountability. As globalization and technology reshape financial practices, the concept of time in finance may evolve, but its fundamental role will remain unchanged. Ultimately, financial time ranges ensure that the story of a business is told in chapters rather than scattered fragments, enabling stakeholders to interpret and act with confidence.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on December 29, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

***

***

The U.S. housing market has 37.2 percent more sellers than buyers, according to a new report by Redfin—more than double the gap reported last year, at 17 percent.

In November, there were 529,770 more sellers than buyers across the country, the real estate brokerage reported. It was the largest gap in records dating back to 2013, with the exception of this past summer.

Posted on December 29, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

BASIC DEFINITIONS

By Dr. David Edward Marcinko MBA MEd

***

***

A Financial Innovation

Double‑barrelled bonds represent a distinctive form of municipal financing that blends two layers of security to reassure investors and reduce borrowing costs for issuers. At their core, these instruments combine the pledge of a specific revenue stream with the backing of a broader governmental taxing authority. This dual protection creates a hybrid between revenue bonds and general obligation bonds, offering both targeted repayment sources and the safety net of full faith and credit.

Structure and Mechanics

A traditional revenue bond is repaid solely from the income generated by a project, such as tolls from a highway or fees from a water utility. While this structure ties repayment directly to the project’s success, it can expose investors to risk if revenues fall short. General obligation bonds, by contrast, are backed by the taxing power of the municipality, meaning repayment is supported by property taxes or other general revenues. Double‑barrelled bonds merge these two approaches. They are issued with the expectation that project revenues will cover debt service, but if those revenues prove insufficient, the municipality’s general funds are legally obligated to step in.

This dual commitment is what gives the bonds their “double‑barrelled” name. Investors gain confidence knowing that repayment does not depend solely on the performance of a single project. Municipalities benefit because this confidence often translates into lower interest rates compared to pure revenue bonds.

Advantages for Issuers and Investors

For issuers, double‑barrelled bonds provide flexibility. They allow municipalities to finance projects that may not generate consistent or predictable revenue streams, while still accessing capital markets at favorable terms. The presence of a general obligation pledge reduces perceived risk, broadening the pool of potential investors. This can be especially useful for projects that serve essential public purposes but lack strong revenue‑generating capacity, such as schools or public safety facilities.

For investors, the appeal lies in the layered security. The primary revenue source offers a clear repayment path, while the general obligation pledge acts as a safety net. This combination reduces default risk and enhances credit quality. In practice, double‑barrelled bonds often receive higher ratings than comparable revenue bonds, making them attractive to conservative investors seeking stability.

Potential Drawbacks

Despite their advantages, double‑barrelled bonds are not without challenges. From the issuer’s perspective, pledging general funds creates a long‑term obligation that can strain budgets if project revenues consistently underperform. Taxpayers may ultimately bear the burden of repayment, raising questions about fairness when the financed project benefits only a subset of the community. Additionally, the complexity of the structure can make disclosure and transparency more demanding, requiring careful communication with investors and rating agencies.

For investors, while the dual pledge reduces risk, it does not eliminate it. Municipal financial health can fluctuate, and reliance on general obligation backing assumes that the municipality maintains sufficient taxing capacity and fiscal discipline. In rare cases of severe financial distress, even double‑barrelled bonds may face repayment challenges.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The United States economy is one of the most diverse and dynamic in the world, driven by a broad mix of industries that together form an intricate and interdependent system. These industries are commonly grouped into eleven major sectors, each contributing unique strengths to national productivity, employment, and innovation. Understanding these sectors provides insight into how the U.S. economy functions and why it remains globally influential.

1. Energy The energy sector powers every other part of the economy. It includes oil, natural gas, coal, and increasingly renewable sources such as wind and solar. This sector influences everything from transportation to manufacturing costs. As the U.S. transitions toward cleaner energy, innovation and infrastructure investment continue to reshape the sector’s future.

2. Materials The materials sector supplies the raw inputs needed for construction, manufacturing, and consumer goods. It includes companies involved in mining, chemicals, forestry, and metals. Because it sits at the beginning of many supply chains, this sector is sensitive to global commodity prices and economic cycles.

3. Industrials Industrials encompass manufacturing, aerospace, defense, transportation, and engineering services. This sector builds the physical backbone of the economy—airplanes, machinery, roads, and logistics networks. It is also a major employer, especially in regions with strong manufacturing traditions.

4. Consumer Discretionary This sector includes goods and services people buy with disposable income, such as cars, apparel, entertainment, and restaurants. Because spending here rises and falls with consumer confidence, it serves as a barometer of economic health. Innovation in e‑commerce and retail technology continues to transform how businesses in this sector operate.

5. Consumer Staples In contrast to discretionary goods, consumer staples include essential products such as food, beverages, and household items. Demand remains steady even during economic downturns, making this sector relatively stable. It plays a crucial role in maintaining everyday life and supporting national food security.

6. Health Care The health care sector spans hospitals, pharmaceuticals, biotechnology, medical devices, and insurance. It is one of the fastest‑growing sectors due to an aging population, rising medical needs, and continuous scientific breakthroughs. Its economic importance is matched by its social significance.

***

***

7. Financials Banks, insurance companies, investment firms, and real estate services make up the financial sector. It allocates capital, manages risk, and supports business growth. Because financial institutions connect all parts of the economy, this sector’s stability is essential for preventing systemic crises.

8. Information Technology Often considered the engine of modern economic growth, the IT sector includes software, hardware, semiconductors, and digital services. It drives innovation across all industries, enabling automation, data analytics, and global communication. The U.S. remains a global leader in technology development and entrepreneurship.

9. Communication Services This sector includes telecommunications, media, entertainment, and internet platforms. It shapes how people connect, consume information, and participate in digital culture. As streaming, social media, and online advertising expand, this sector continues to evolve rapidly.

10. Utilities Utilities provide essential services such as electricity, water, and natural gas. Highly regulated and stable, this sector ensures the infrastructure that households and businesses rely on daily. Its long‑term investments support reliability and modernization, including the shift toward smart grids and renewable integration.

11. Real Estate The real estate sector includes residential, commercial, and industrial property development and management. It reflects population trends, business expansion, and investment patterns. Housing markets, in particular, play a major role in shaping consumer wealth and economic sentiment.

Together, these eleven sectors form a resilient and interconnected economic system. Each contributes distinct capabilities, yet all depend on one another to support growth, innovation, and national prosperity. Understanding these sectors provides a clearer picture of how the U.S. economy adapts, competes, and continues to evolve in a rapidly changing world.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on December 28, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

SPONSOR: Health Capital Consultants, LLC

***

***

On November 21, 2025, the Centers for Medicare & Medicaid Services (CMS) released its Calendar Year (CY) 2026 Hospital Outpatient Prospective Payment System (OPPS) and Ambulatory Surgical Center (ASC) Payment System Final Rule, affecting approximately 4,000 hospitals and 6,000 ASCs. The rule finalizes payment updates, policy reforms, and transparency requirements that will impact hospital and ASC operations beginning January 1, 2026.

This Health Capital Topics article discusses the key OPPS changes and updates included in the Final Rule. (Read more…)

Posted on December 28, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

Dr. David Edward Marcinko; MBA MEd

***

***

The idea of portable mortgages has emerged as a potential solution to challenges facing today’s housing market. In a traditional mortgage system, when a homeowner sells their property, they must pay off the existing loan and take out a new one at prevailing interest rates. This structure works smoothly when interest rates are stable, but in periods of sharp increases, it creates what is often called the “lock‑in effect.” Homeowners who secured low rates in the past are reluctant to move, since doing so would mean replacing their affordable loan with a far more expensive one. Portable mortgages aim to address this problem by allowing borrowers to carry their existing loan terms to a new property.

How Portable Mortgages Would Work

A portable mortgage would allow a homeowner to transfer their current loan—including the interest rate and repayment schedule—to a new home. Instead of starting over with a fresh loan, the borrower would continue under the same contract, simply attaching it to a different property. This concept is already familiar in some international markets, where portability is offered as a feature of certain mortgage products. Bringing such a system into the United States would represent a significant departure from current practice, but it could unlock new flexibility for homeowners.

Potential Benefits

The advantages of portable mortgages are easy to imagine. First, they would increase mobility. Families could relocate for work, education, or lifestyle reasons without being penalized by higher borrowing costs. Second, they could improve liquidity in the housing market. More homeowners willing to sell would mean more properties available, easing supply constraints that drive up prices. Third, portability could help households upgrade to larger homes or downsize to smaller ones without facing a financial shock. Finally, the psychological effect of knowing that a favorable loan can be preserved might reduce hesitation and encourage more natural movement in the housing market.

Challenges and Risks

Despite these potential benefits, portable mortgages also raise serious challenges. One issue is the complexity of the American mortgage system, which relies heavily on securitization. Mortgages are bundled into securities and sold to investors, who expect predictable terms. Allowing loans to move between properties could complicate valuation and trading of these securities. Another challenge is the mismatch between loan and property. Mortgages are underwritten based on both the borrower’s financial profile and the specific property’s value. Transferring a loan to a new home could introduce risks if the new property is less stable or valued differently.

There is also the possibility of an affordability paradox. While portability helps individual homeowners, it could entrench advantages for those who locked in low rates during past years, widening the gap between them and new buyers who must borrow at higher rates. Lenders might also face administrative burdens, needing new systems to evaluate portability requests and ensure compliance.

Policy Considerations

The debate around portable mortgages reflects broader concerns about housing affordability. Policymakers are searching for ways to ease the lock‑in effect and encourage mobility. Portable mortgages are one idea among several, alongside proposals for longer‑term loans or targeted refinancing programs. Each option carries trade‑offs between individual relief and systemic stability. Implementing portability would require regulatory changes and cooperation across lenders, investors, and government agencies.

Comparative Perspective

Countries that already offer portable mortgages provide useful lessons. In some markets, portability is common but subject to restrictions, such as requiring borrowers to requalify under the lender’s criteria or limiting portability to certain types of loans. These examples show that portability can work, but only with careful design and oversight.

Conclusion

Portable mortgages represent an innovative response to the challenges of rising interest rates and constrained housing supply. They promise greater mobility, improved affordability, and a more dynamic housing market. Yet they also pose risks to the financial system and raise questions of fairness between different groups of borrowers. Whether they can be successfully introduced depends on balancing these competing concerns. While not a simple solution, portable mortgages highlight the need for creative thinking about how to adapt the housing finance system to today’s realities.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Franchising has long been associated with industries such as food service and retail, but in recent decades, it has expanded into professional services, including financial planning, accounting, and investment management. These areas, traditionally dominated by independent firms or large corporate institutions, are increasingly adopting franchise models to deliver standardized, accessible, and trusted financial services. By combining entrepreneurial opportunity with brand recognition and operational support, financial service franchises are reshaping how individuals and businesses manage their money.

Growth Drivers

Several factors explain the rise of franchising in financial services:

Complex financial landscape: With tax laws, investment options, and retirement planning becoming more complicated, individuals and businesses seek reliable, standardized guidance.

Demand for accessibility: Many communities lack affordable financial advisory services, and franchises can fill this gap by offering consistent solutions across multiple locations.

Trust and brand recognition: Consumers often feel more comfortable working with a recognizable brand rather than an unknown independent advisor.

Entrepreneurial appeal: Professionals with backgrounds in finance or accounting can leverage franchise systems to start their own businesses with reduced risk.

Types of Financial Service Franchises

Franchises in this sector cover a wide range of services:

Accounting and tax preparation: These franchises provide bookkeeping, payroll, and tax filing services for individuals and small businesses.

Financial planning: Franchises offer retirement planning, estate planning, and wealth management services, often targeting middle-income families who may not otherwise access professional advice.

Investment management: Some franchises focus on portfolio management, investment education, and advisory services, helping clients navigate stock markets, mutual funds, and other vehicles.

Business consulting: Beyond personal finance, franchises also provide small business owners with guidance on budgeting, cash flow, and strategic growth.

Advantages of Franchising in Financial Services

The franchise model offers distinct benefits for both clients and franchisees:

Consistency and reliability: Clients receive standardized services across locations, ensuring predictable quality.

Training and support: Franchisees benefit from established systems, training programs, and compliance guidance, reducing the risk of errors in complex financial matters.

Scalability: Franchises can expand quickly into new markets, bringing financial services to underserved communities.

Lower entry barriers: Professionals entering the financial services industry gain access to proven business models, marketing support, and operational infrastructure.

Challenges and Criticisms

Despite its advantages, franchising in financial services faces notable challenges:

Regulatory complexity: Financial services are heavily regulated, and franchisees must comply with strict laws governing investments, accounting practices, and client confidentiality.

Quality concerns: While standardization is a goal, maintaining consistent advisory quality across multiple franchise locations can be difficult.

Profit vs. fiduciary duty: Critics argue that franchising risks prioritizing profitability over client interests, especially in investment management where conflicts of interest may arise.

Market competition: Independent advisors and large financial institutions remain strong competitors, requiring franchises to differentiate themselves through pricing, accessibility, or niche services.

Future Outlook

The future of financial service franchising appears promising. As financial literacy becomes more important in an era of economic uncertainty, franchises will likely expand their role in educating clients and offering accessible solutions. Advances in technology—such as AI-driven financial planning tools, automated accounting software, and digital investment platforms—will further enhance franchise offerings. Hybrid models that combine in-person advisory services with digital tools are expected to dominate, providing clients with both convenience and personalized guidance.

Conclusion

Franchises in financial planning, accounting, and investment management represent a transformative shift in how financial services are delivered. They combine the trust of recognizable brands with the entrepreneurial drive of local professionals, expanding access to essential financial guidance. While challenges remain in regulation, quality assurance, and balancing profit with fiduciary responsibility, the franchise model offers a scalable and reliable way to meet growing demand. As financial needs evolve, franchising will continue to play a pivotal role in democratizing financial expertise, bridging the gap between large institutions and local communities, and empowering individuals and businesses to make informed financial decisions.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on December 27, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko MBA MEd, Ann Miller RN MHA CPHQ and Staff Reporters

INFORMATION AND NEWS PORTAL

***

***

Contribute Your Knowledge to the Medical Executive-Post.com

Healthcare, finance and economics today is defined by rapid transformation, complex challenges, and the urgent need for visionary leadership. Contributing your expertise to the Medical Executive Post.com blog is more than an opportunity to share ideas; it is a chance to shape conversations that influence the future of medical administration, health economics and finance.

At its core, the role of a physician, nurse, medical executive, financial advisor, investment planner, CPA or healthcare attorney is about bridging the gap between expertise and dissemination strategy. These opinions bring invaluable perspectives, and it is the ME-P that ensures these voices are harmonized into a coherent vision. Writing for Medical Executive Post.com allows contributors to highlight best practices, share lessons learned, and inspire peers to think critically about how leadership can improve outcomes.

One of the most pressing issues facing healthcare and financial executives today is resource management. Rising costs, workforce shortages, and the integration of new technologies demand innovative solutions. By contributing to this blog, you can explore strategies that balance fiscal responsibility with compassionate care. For example, discussing how tele-medicine, block chain or artificial intelligence can expand access without overwhelming budgets, or how data analytics can streamline operations while enhancing patient safety, provides actionable insights for leaders navigating these challenges.

Equally important is the ethical dimension of medical and financial leadership. Executives are entrusted with decisions that affect not only institutions but also the lives of patients and communities. Contributing to the blog offers a platform to advocate for transparency, accountability, and equity. Sharing perspectives on how to build inclusive healthcare and financial systems, or how to foster trust through ethical governance, ensures that leadership remains grounded in values as well as efficiency.

Finally, the blog is a space for collaboration. Healthcare finance is not a solitary endeavor; it thrives on networks of professionals who learn from one another. By writing for Medical Executive Post.com, you join a community dedicated to advancing the profession. Whether through case studies, thought pieces, or reflections on leadership journeys, each contribution strengthens the collective knowledge base and inspires others to lead with courage and vision.

In conclusion, contributing to Medical Executive Post.com is about more than publishing words online. It is about shaping the dialogue that defines modern healthcare financial and economic leadership. Through thoughtful analysis, ethical reflection, and collaborative spirit, we aim to use this platform to advance the mission of those executives everywhere: delivering care that is innovative, equitable, and deeply human.

Imposter syndrome has become a widely discussed psychological pattern across many industries, but it holds a particularly strong presence in the world of finance. Known for its high stakes, competitive culture, and relentless performance expectations, finance creates an environment where even the most capable professionals can feel like frauds waiting to be exposed. Imposter syndrome is not simply a lack of confidence; it is a persistent belief that one’s success is undeserved, accompanied by the fear that others will eventually uncover the truth. In a field where precision, intelligence, and decisiveness are prized, this internal narrative can be especially damaging.

Economics plays a significant role in shaping the conditions that allow imposter syndrome to flourish. The financial sector operates within a labor market characterized by high competition, asymmetric information, and strong incentives tied to performance. Human capital theory suggests that individuals invest heavily in education and skills to compete for elite roles, yet the rapid evolution of financial products and technologies means that knowledge depreciates quickly. This creates a constant pressure to keep up, reinforcing the fear that one’s expertise is never sufficient. Additionally, signaling theory helps explain why professionals often feel compelled to project confidence even when uncertain; appearing knowledgeable becomes a form of economic signaling that influences promotions, compensation, and perceived value.

The industry’s culture of comparison further amplifies these pressures. From the first day of an internship to the highest levels of leadership, individuals are measured against peers, market benchmarks, and performance metrics. Compensation structures—especially bonuses tied to relative performance—create a winner‑take‑all environment. Behavioral economics shows that people tend to overestimate the abilities of others while underestimating their own, a cognitive bias that feeds directly into imposter feelings. Even strong performers may feel that they are only as good as their last deal, trade, or quarterly report. In such an environment, success feels fragile, as though it could collapse with a single misstep.

The complexity of financial work also contributes to imposter syndrome. Whether analyzing derivatives, building valuation models, or navigating regulatory frameworks, finance demands mastery of intricate concepts. Yet the pace of the industry leaves little room for slow learning or uncertainty. The economic principle of information asymmetry is at play here: newcomers often assume that others possess more knowledge than they do, even when that is not the case. The industry’s jargon‑heavy communication style reinforces this perception, making it easy to believe that everyone else understands more.

Imposter syndrome is not limited to junior employees. Senior leaders, portfolio managers, and partners often experience it as well. The higher one climbs, the more visible mistakes become, and the more pressure there is to maintain an image of expertise. Prospect theory helps explain this dynamic: losses—such as reputational damage—loom larger than equivalent gains, making leaders especially sensitive to the fear of being “found out.”

The effects of imposter syndrome can be significant. It can lead to overworking, as individuals attempt to compensate for perceived inadequacy by pushing themselves harder than necessary. It can also stifle career growth, causing talented professionals to avoid promotions or high‑visibility projects out of fear they are not ready. Over time, this can contribute to burnout, anxiety, and disengagement—issues that already run high in the financial sector and carry economic costs for firms through turnover and reduced productivity.

Addressing imposter syndrome requires both individual and organizational strategies. On a personal level, professionals can benefit from reframing their internal narratives and recognizing that learning is continuous. Mentorship can help normalize uncertainty and reduce the perceived knowledge gap. At the organizational level, firms can foster cultures that value transparency, learning, and psychological safety. Encouraging questions, offering structured feedback, and celebrating progress rather than only outcomes can help reduce the fear of inadequacy.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on December 27, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

***

***

Oil prices were stable yesterday as investors weighed potential supply risks from developing geopolitical tensions in a thinly attended post-Christmas session, after the U.S.A carried out airstrikes against Islamic State militants in Nigeria and added greater economic pressure on Venezuelan oil.

Brent crude futures fell 16 cents, or 0.26%, to $62.08 per barrel by 1148 GMT. U.S. West Texas Intermediate (WTI) crude was down 7 cents, or 0.12%, at $58.28.

Oil prices are ready for their steepest annual decline since 2020, with Brent and WTI down 17% and 19% respectively versus the final close of 2024. Rising oil output from both the OPEC+ group and non-OPEC states has raised concerns of a market in surplus heading into next year.

The TED spread is one of the most widely recognized indicators of credit risk and overall confidence within the financial system. At its core, it measures the difference between the interest rate on short‑term U.S. government debt—typically the three‑month Treasury bill—and the interest rate at which banks lend to one another, historically represented by the three‑month London Interbank Offered Rate. Although simple in calculation, the spread captures a complex and revealing story about trust, liquidity, and perceived risk in global markets.

Treasury bills are considered among the safest assets in the world. They are backed by the full faith and credit of the U.S. government, and investors treat them as essentially risk‑free. Interbank loans, by contrast, carry credit risk because they depend on the financial health of the borrowing bank. When banks trust each other and view the system as stable, the rate they charge one another remains close to the Treasury bill rate. The TED spread stays low, signaling calm conditions and ample liquidity.

When uncertainty rises, however, the relationship changes dramatically. If banks begin to doubt the solvency or reliability of their peers, they demand higher interest rates to compensate for the perceived risk. Treasury bills, meanwhile, often become a safe‑haven asset, causing their yields to fall as investors rush toward security. The combination of rising interbank rates and falling Treasury yields widens the TED spread. This widening is interpreted as a sign of stress, fear, or dysfunction in the financial system.

The TED spread has historically served as an early warning signal during periods of financial turbulence. When the spread spikes, it often reflects a breakdown in trust—one of the most essential ingredients in modern banking. Banks rely on short‑term borrowing to fund daily operations, and when they hesitate to lend to one another, liquidity can evaporate quickly. A high TED spread therefore suggests that institutions are hoarding cash, preparing for potential losses, or bracing for broader instability.

Although the spread is a technical measure, its implications extend far beyond the banking sector. A rising TED spread can influence borrowing costs for businesses and consumers, as banks pass along their heightened funding costs. It can also affect investment decisions, as investors reassess risk across asset classes. In extreme cases, a sharply elevated spread can signal systemic danger, prompting central banks to intervene with liquidity injections or emergency lending facilities.

Despite its importance, the TED spread is not a perfect indicator. It reflects conditions in the interbank market, but financial stress can emerge in other corners of the system that the spread does not capture. Moreover, structural changes—such as reforms to benchmark interest rates—can influence how the spread behaves over time. Still, its simplicity and long history make it a valuable tool for analysts, policymakers, and investors seeking to gauge the pulse of the financial system.

Ultimately, the TED spread endures because it distills a complex web of financial relationships into a single, intuitive number. It tells a story about confidence: when the spread is narrow, trust is abundant and markets function smoothly; when it widens, fear takes hold and the machinery of finance begins to grind. In this way, the TED spread serves not only as a technical metric but also as a barometer of collective sentiment—revealing how secure or fragile the financial world feels at any given moment.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The One Big Beautiful Bill Act (OBBBA) represents one of the most sweeping changes to the U.S. financial and tax landscape in recent years. For financial planners and investment advisors, the legislation introduces a wide range of implications that require careful analysis, strategic adjustments, and proactive communication with clients. Because the act touches on taxation, estate planning, investment incentives, and government‑benefit programs, professionals in the advisory field must reassess existing plans and ensure that clients’ financial strategies remain aligned with the new rules.

One of the most significant areas affected by the OBBBA is personal taxation. The act extends and modifies several provisions that were originally scheduled to expire, reshaping income tax brackets, deductions, and credits. For advisors, this means revisiting tax‑efficient investment strategies and reassessing how clients should time income, deductions, and capital gains. High‑income clients, in particular, may experience shifts in their marginal tax rates or changes in the value of certain deductions. Advisors must model these changes to determine whether clients should accelerate income, defer income, adjust charitable giving, or rebalance portfolios to maintain tax efficiency under the new structure.

Estate planning is another domain where the OBBBA has a substantial impact. The legislation adjusts estate tax exemptions and modifies rules governing wealth transfers. These changes create both opportunities and challenges for high‑net‑worth individuals. Advisors must evaluate whether clients should take advantage of temporarily favorable exemptions, make strategic gifts, or restructure trusts before certain provisions sunset. Because many of the new rules are time‑limited, advisors must act quickly to help clients secure benefits that may not be available in future years.

Investment incentives also shift under the OBBBA. Changes to credits and deductions related to specific industries—such as clean energy, real estate, or manufacturing—may alter the attractiveness of certain investment products or sectors. Advisors must reassess portfolio allocations and ensure that clients understand how the new rules affect expected returns. In addition, adjustments to retirement account rules, education savings incentives, and capital‑gains treatment require advisors to update long‑term projections and revisit asset‑location strategies. These changes highlight the need for ongoing portfolio monitoring and a willingness to adapt as the regulatory environment evolves.

The OBBBA also affects planning related to healthcare and government‑benefit programs. Adjustments to Medicaid eligibility, long‑term‑care provisions, and certain safety‑net programs may influence how clients plan for future medical expenses. Advisors must help clients anticipate potential increases in out‑of‑pocket costs and consider alternative strategies such as long‑term‑care insurance, revised withdrawal plans, or changes to retirement‑income sequencing. These shifts reinforce the importance of holistic planning that integrates healthcare, retirement, and estate considerations into a unified strategy.

Beyond technical planning, the OBBBA has operational implications for advisory firms. Advisors must update their planning software, revise internal processes, and ensure that compliance frameworks reflect the new rules. Continuing education becomes essential, as advisors must stay informed about the legislation’s nuances and communicate its effects clearly to clients. Firms that respond quickly and confidently can strengthen client relationships by demonstrating expertise during a period of uncertainty.

In summary, the OBBBA reshapes the financial planning landscape by altering tax rules, estate‑planning opportunities, investment incentives, and government‑benefit structures. For financial planners and investment advisors, the act requires a comprehensive review of client strategies and a proactive approach to communication and planning. While the legislation introduces complexity, it also creates opportunities for advisors to deliver meaningful value by guiding clients through a changing environment with clarity and confidence.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

The Eurodollar is one of the most influential yet least understood forces in modern finance. Despite the name, it has nothing to do with Europe’s common currency. Instead, the Eurodollar refers to U.S. dollars held in banks outside the United States. These offshore dollars form a vast, largely unregulated financial ecosystem that has shaped global markets, international lending, and monetary policy for more than half a century.

The origins of the Eurodollar market trace back to the years after World War II, when the U.S. dollar became the backbone of global trade. As American economic power expanded, foreign governments, corporations, and banks accumulated dollars. Many of these dollars ended up in European banks, especially in London, which was emerging as a global financial hub. During the Cold War, some countries even preferred to keep their dollar reserves outside the United States to avoid potential political risks. Over time, these offshore dollar deposits grew into a massive parallel banking system.

What makes the Eurodollar so significant is its freedom from U.S. banking regulations. Because these dollars sit outside American jurisdiction, they are not subject to the same reserve requirements, interest rate caps, or reporting rules that govern domestic banks. This regulatory gap allowed the Eurodollar market to innovate quickly and offer more competitive rates. Banks could lend more aggressively, borrowers could access cheaper credit, and financial institutions could structure deals with fewer constraints. The result was a dynamic, fast‑growing market that soon dwarfed many traditional banking channels.

By the 1970s and 1980s, the Eurodollar market had become a central pillar of global finance. It provided liquidity to multinational corporations, funded international trade, and supported the rise of global capital markets. London, in particular, became the unofficial capital of the Eurodollar world, attracting banks from around the globe eager to participate in this flexible and profitable environment. The market also played a key role in the development of new financial instruments, such as interest rate swaps and offshore bond markets, which further expanded its reach.

One of the most important consequences of the Eurodollar system is its impact on monetary policy. Because so many dollars circulate outside the United States, the Federal Reserve does not fully control the global supply of dollars. When offshore banks create dollar‑denominated loans, they effectively expand the dollar system without the Fed’s direct oversight. This means global dollar liquidity can rise or fall independently of domestic U.S. policy decisions. During periods of financial stress, shortages of Eurodollar funding can ripple through global markets, creating pressures that central banks must scramble to address.

The 2008 financial crisis highlighted this vulnerability. As confidence collapsed, banks around the world suddenly struggled to access dollar funding. The Eurodollar system, which had grown enormous and interconnected, became a source of instability. In response, the Federal Reserve had to establish emergency swap lines with foreign central banks to supply offshore markets with dollars. This episode revealed just how deeply the Eurodollar market is woven into the fabric of global finance.

Today, the Eurodollar remains a powerful but largely invisible force. It continues to support international trade, global investment, and cross‑border banking. Even as new forms of digital money and alternative currencies emerge, the world still relies heavily on offshore dollars for liquidity and stability. The Eurodollar market illustrates how financial systems can evolve beyond the reach of national borders, creating both opportunities and challenges for policymakers and institutions.

In essence, the Eurodollar is a reminder that money is not just a domestic tool but a global network. Its rise transformed the way capital moves around the world, and its influence continues to shape the global economy in ways that are often hidden from public view.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on December 26, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

SPONSOR: Health Capital Consultants, LLC

***

***

The healthcare mergers and acquisitions (M&A) market in 2025 has been characterized by strategic recalibration, with transaction activity recovering after a slow start to the year. Hospital and health system M&A began 2025 at subdued levels but gained momentum through the third quarter, suggesting renewed dealmaker confidence. Meanwhile, healthcare services transactions have remained robust, with 231 deals in the first half of 2025, representing a 14.4% increase from the prior period.

This Health Capital Topics article examines 2025 year-to-date transaction activity and analyzes factors expected to influence healthcare M&A in 2026. (Read more…)

Posted on December 25, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

Estate Planning

By Dr. David Edward Marcinko MBA MEd

***

***

📜 Precatory Letter: Meaning and Significance

A precatory letter is a document that expresses wishes, hopes, or recommendations rather than legally binding instructions. The word precatory comes from the Latin precari, meaning “to pray” or “to entreat.” In modern usage, it refers to language that conveys a desire or request without imposing a legal obligation. Within estate planning and related contexts, a precatory letter is often used to supplement formal documents such as wills or trusts, offering guidance and emotional expression that the law itself cannot enforce.

***

***

⚖️ Legal Nature

The defining characteristic of a precatory letter is that it is non-binding. Courts distinguish between mandatory language, such as “shall” or “must,” and precatory language, such as “wish,” “hope,” or “request.” For example, if a will states, “I hope my children will keep the family home,” this is considered precatory. The heirs are free to follow the suggestion, but they are not legally compelled to do so. This distinction ensures that only clear, directive language creates enforceable obligations, while precatory language remains advisory.

💡 Practical Purposes

Despite lacking legal force, precatory letters serve important functions:

Emotional comfort: They allow individuals to leave behind words of love, encouragement, and reassurance for family members.

Moral guidance: They can express values, traditions, or charitable wishes, encouraging heirs to act in ways that reflect the writer’s principles.

Practical clarity: They may explain decisions made in a will or trust, reducing misunderstandings and potential disputes among beneficiaries.

Personal legacy: They preserve stories, hopes, and family culture that legal documents cannot capture.

For instance, a parent might leave a will dividing assets equally but include a precatory letter asking children to use part of their inheritance for education or to maintain a family property. While not enforceable, such guidance often carries moral weight and influences behavior.

🌟 Benefits and Limitations

The benefit of a precatory letter lies in its flexibility and humanity. It allows individuals to communicate beyond the rigid framework of law, offering context and emotional depth. It can reduce conflict by clarifying intentions and help heirs feel connected to the values of the deceased.

However, its limitation is clear: it cannot override or alter legally binding documents. If a will distributes property in a certain way, a precatory letter cannot change that distribution. Its power is persuasive rather than compulsory, relying on the goodwill and respect of those who receive it.

📝 Conclusion

In essence, a precatory letter is a bridge between law and emotion. It complements formal estate planning documents by expressing wishes, values, and guidance in a personal voice. Though it lacks binding authority, its significance lies in the comfort, clarity, and moral influence it provides. By writing a precatory letter, individuals ensure that they leave behind not only material possessions but also a legacy of values, memories, and heartfelt direction for loved ones.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on December 25, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dr. David Edward Marcinko; MBA MEd

***

***

The 50/30/20 budgeting rule is a widely embraced personal finance strategy that offers a straightforward framework for managing income. This rule divides after-tax income into three categories: 50% for needs, 30% for wants, and 20% for savings and debt repayment. Its simplicity and flexibility make it an ideal starting point for individuals seeking financial stability and long-term growth.

🏠 50% for Needs

The first category, “needs,” encompasses essential expenses that are non-negotiable for daily living. These include housing costs (rent or mortgage), utilities, groceries, transportation, insurance, and minimum loan payments. The goal is to keep these necessities within half of one’s income to avoid financial strain. If needs exceed 50%, it may signal the need to reassess lifestyle choices—such as downsizing housing or reducing commuting costs—to maintain balance.

🎉 30% for Wants

“Wants” refer to discretionary spending—things that enhance life but aren’t essential. Dining out, entertainment, travel, hobbies, and luxury purchases fall into this category. This portion of the budget allows for enjoyment and personal fulfillment, which is crucial for mental well-being. However, distinguishing between wants and needs can be tricky. For example, a basic phone plan is a need, but the latest smartphone upgrade is a want. Practicing mindful spending helps ensure this category doesn’t encroach on essentials or savings.

💰 20% for Savings and Debt Repayment

The final 20% is allocated to financial growth and security. This includes building an emergency fund, contributing to retirement accounts, investing, and paying off debts beyond minimum payments. Prioritizing this category helps individuals prepare for unexpected expenses and achieve long-term goals like homeownership or early retirement. For those with high-interest debt, allocating more of this portion toward repayment can yield significant financial benefits over time.

📊 Benefits of the 50/30/20 Rule

One of the rule’s greatest strengths is its simplicity. Unlike complex budgeting systems that require meticulous tracking of every expense, the 50/30/20 rule offers a high-level view that’s easy to implement and maintain. It’s also adaptable—users can tweak percentages based on personal circumstances. For instance, someone aggressively saving for a home might shift to a 40/20/40 model temporarily.

Moreover, this rule promotes financial discipline without sacrificing enjoyment. By clearly defining boundaries for spending, it encourages intentional choices and reduces impulsive purchases. It also fosters a habit of saving, which is often overlooked in traditional budgeting approaches.

🧭 Conclusion

The 50/30/20 budgeting rule is a powerful tool for anyone seeking to take control of their finances. Its balanced approach ensures that essential needs are met, personal desires are fulfilled, and future goals are actively pursued. Whether you’re just starting your financial journey or looking to simplify your budget, this rule offers a clear, effective roadmap to financial wellness.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com

Posted on December 25, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

CHRISTMAS 2025

Dr. David Edward Marcinko; MBA MEd

***

***

Mapping the Blueprint of Life

The Human Genome Project (HGP) stands as one of the most ambitious and transformative scientific endeavors in modern history. Launched in 1990 and completed in 2004, the project brought together an international coalition of researchers with a singular goal: to decode the full sequence of human DNA and identify all human genes. This monumental achievement reshaped the fields of biology, medicine, and biotechnology, opening new pathways for understanding human health and disease.

At its core, the Human Genome Project sought to map the approximately 3 billion base pairs that make up the human genome and to identify the tens of thousands of genes embedded within it. Before the HGP, scientists understood that DNA carried hereditary information, but the full structure and sequence of the human genome remained a mystery. By determining this sequence, researchers hoped to create a foundational reference that would accelerate scientific discovery for generations.

The project was coordinated primarily by major scientific institutions in the United States, but it quickly grew into a global collaboration involving researchers from multiple countries. This international effort underscored the universal importance of understanding human genetics and ensured that the resulting data would be freely accessible to scientists worldwide.

One of the most remarkable aspects of the HGP was the speed at which it progressed. Initially projected to take 15 years, rapid technological advances in DNA sequencing shortened the timeline, allowing the project to be completed ahead of schedule. These technological breakthroughs not only accelerated the HGP but also laid the groundwork for modern genomic sequencing techniques, which today allow entire genomes to be sequenced in hours rather than years.

The accomplishments of the Human Genome Project extend far beyond the creation of a reference genome. The project also developed powerful new tools for data analysis, established vast genetic databases, and advanced computational biology as a discipline. These innovations made it possible for scientists to compare genetic sequences across species, identify genes associated with diseases, and explore the complex interactions between genes and the environment.