IRS Tax Implications

By Staff Reporters

***

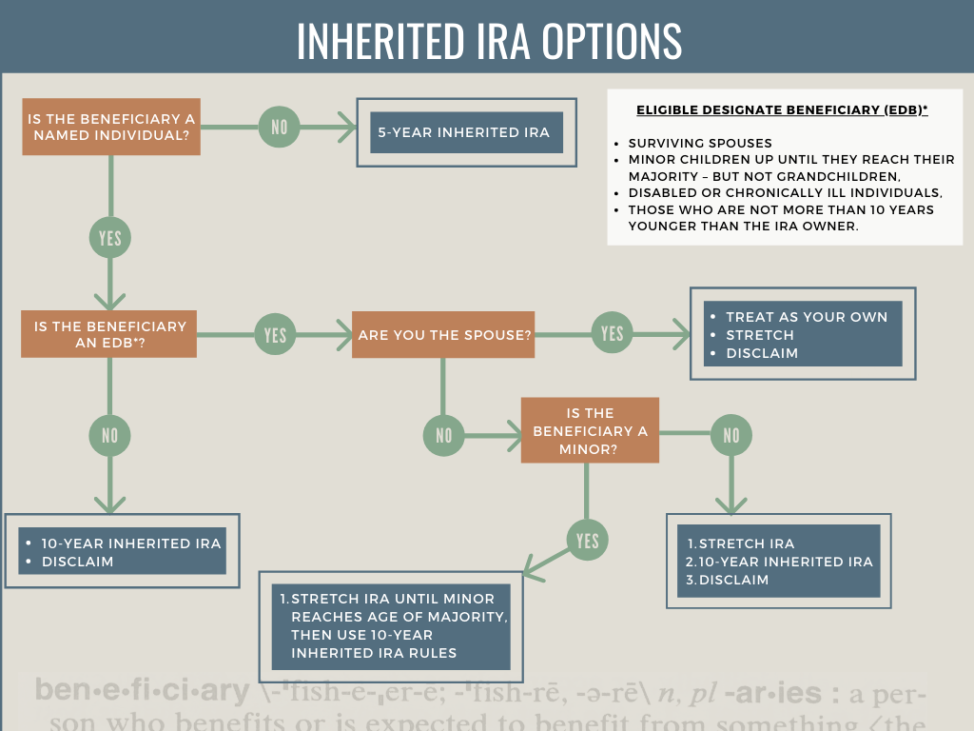

If you inherited a tax-deferred retirement plan, such as a traditional IRA, you’ll have to pay taxes on the money. But you can make the tax hit less onerous.

Spouses can roll the money into their own IRAs and postpone distributions—and taxes—until they’re 70½. All other beneficiaries who want to continue to benefit from tax-deferred growth must roll the money into a separate account known as an inherited IRA. Make sure the IRA is rolled directly into your inherited IRA. If you take a check, you won’t be allowed to deposit the money. Rather, the IRS will treat it as a distribution and you’ll owe taxes on the entire amount.

Once you’ve rolled the money into an inherited IRA, you must take required minimum distributions every year—and pay taxes on the money—based on your age and life expectancy. Deadlines are critical: You must take your first RMD by December 31st. of the year following the death of your parent (or whoever left you the account). Otherwise, you’ll be required to deplete the entire account within five years after the year following your parent’s death.

The December 31st. deadline is also important if you are one of several beneficiaries of an inherited IRA. If you fail to split the IRA among the beneficiaries by that date, your RMDs will be based on the life expectancy of the oldest beneficiary, which may force you to take larger distributions than if the RMDs were based on your age and life expectancy.

You can take out more than the RMD, but setting up an inherited IRA gives you more control over your tax liabilities. You can, for example, take the minimum amount required while you’re working, then increase withdrawals when you’re retired and in a lower tax bracket.

CITE: https://www.r2library.com/Resource/Title/0826102549

***

***

Did you inherit a Roth IRA? And so, as long as the original owner funded the Roth at least five years before he or she died, you don’t have to pay taxes on the money. You can’t, however, let it grow tax-free forever. If you don’t need the money, you can transfer it to an inherited Roth IRA and take RMDs under the same rules governing a traditional inherited IRA. But with a Roth, your RMDs won’t be taxed.

***

COMMENTS APPRECIATED

Thank You

Subscribe to the Medical Executive-Post

***

***

Share this:

Filed under: Accounting, Investing, Retirement and Benefits, Taxation | Tagged: inherited ira, inherited retirement accounts, IRAs, retirement accounts, RMD, roll over IRA, Roth IRAs | Leave a comment »