BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on June 2, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

NO DEFAULT THIS YEAR

***

***

The Senate just passed legislation to lift the nation’s debt ceiling and stave off what would’ve been an economically disastrous default days before Monday’s deadline. The final vote was 63-36. The bill will now go to President Joe Biden’s desk for his signature.

Posted on May 23, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Talks were “productive,” but no debt ceiling deal yet

As the US careens toward a June 1st deadline to avoid default, President Joe Biden and House Speaker Kevin McCarthy met last night and failed to reach an agreement to prevent economic chaos. Still, McCarthy called their discussion “productive” and “professional,” saying the tone was “better than any other time we’ve had discussions.”

Before the meeting, McCarthy acknowledged that a deal must be struck this week in order to get it through Congress prior to the deadline, but the two sides remain far apart on the Republican’s demands for spending cuts.

Posted on May 7, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Treasury Secretary Janet Yellen warned this week that the government could run out of cash to cover its expenses as early as June 1st. Congress can avert the looming economic catastrophe by authorizing more government borrowing so the US can keep paying its bills and avoid an unprecedented default on its financial obligations.

But with the deadline just weeks away, lawmakers are locked in a game of chicken.

Republicans in Congress say they won’t increase the debt limit without budget cuts. Last month, the GOP-controlled House passed a bill that would lift the borrowing cap and slash government spending by around $3.2 trillion over 10 years.

But that bill is DOA in the Democrat-led Senate. Democrats insist the debt limit should be raised with no strings attached.

If the US does run out of money…look out. The Treasury would have a range of extremely bad to absolutely terrible belt-tightening options, including delaying payments to federal contractors and Social Security recipients, all to avoid falling behind on interest payments for Treasury bonds.

Posted on May 2, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Treasury Secretary Janet Yellen warned yesterday that the US could run out of money to pay all its bills as early as June 1st if Congress does not raise or suspend the debt limit before then. The US’ first-ever default would be disastrous for financial markets, economists say.

***

Meanwhile, Europe’s painful inflation has inched higher, extending the squeeze on households and keeping pressure on the European Central Bank to unleash what could be another large interest rate increase. Consumer prices in the 20 countries using the euro currency jumped 7% in April from a year earlier, just up from the annual rate of 6.9% in March, the European Union statistics agency Eurostat said today. Food price inflation eased a little, falling to an annual rate of 13.6% from March’s 15.5%, while energy prices rose a more modest 2.5%. Core inflation, which excludes volatile food and fuel, slowed slightly but was still high at 5.6%, underlining the expectation that the ECB will press ahead with its campaign to beat inflation into submission with rate hikes.

Posted on January 21, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

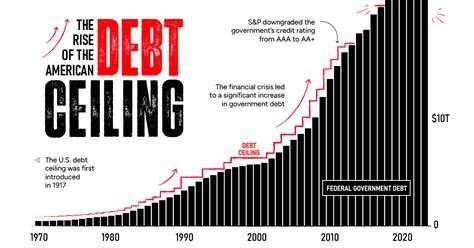

As the US just crashed into the $31.4 trillion debt ceiling as the Treasury Department began taking what it called “extraordinary measures” to prevent the government from defaulting on its debts and sparking an economic crisis.

These measures are a series of deep-cut accounting moves that allow the Treasury to continue making its payments. They include:

Suspending reinvestments into government funds for retired federal employees, such as the Civil Service Retirement and Disability Fund.

Selling existing investments in those funds to free up more outstanding debt.

And while these measures definitely aren’t ordinary…they probably aren’t so “extra,” either. The Treasury has resorted to them more than 12 times since 1985, including during the last debt-ceiling standoff in 2021.

Still, these steps amount to chugging water after eating a ghost pepper—the pain will return. Treasury Secretary Janet Yellen said her extraordinary measures will last through early June, giving lawmakers about five months to work out a deal to raise the debt ceiling.

NOTE: The US has never defaulted on its debt, but even the threat of it could be disastrous. The country’s first credit downgrade in history came during a debt-ceiling showdown in 2011.

A cap on how much the US government can borrow to finance its operations.

It was introduced during World War I so that Congress wouldn’t have to approve every bond issuance by the Treasury Department as it had done previously—freeing up more time for name-calling.

The debt ceiling has been suspended dozens of times over the years, including 3x during the Trump administration.

Without suspending the debt ceiling, the US wouldn’t be able to borrow money to pay its bills—and things would get ugly if that happened. The federal government would have to slash spending for programs like Medicaid, local governments would find it harder to borrow, and financial markets could go haywire.

In short, a failure to act would “produce widespread economic catastrophe,” Treasury Secretary Janet Yellen wrote in the Wall Street Journal.

Important note: The debt ceiling doesn’t account for new spending, like the $3.5 trillion proposal the Democrats have on the table. Instead, it’s about spending Congress has already authorized, such as paying out Social Security. Over the years, the debt ceiling has become a “political weapon,” according to the AP, as each party tries to blame the other for their spending habits and for heaping more debt on the US.

/u-s-debt-ceiling-why-it-matters-past-crises-9ee4f4a3337c4203997fb191a9858b8c.gif)