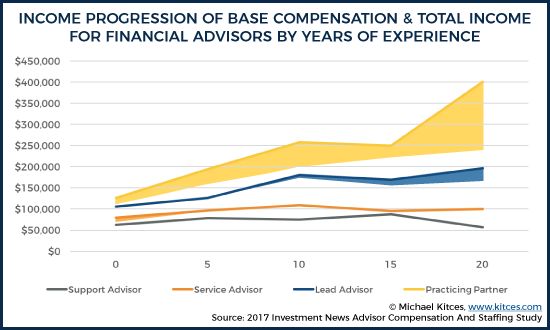

By Years of experience

Via Michael Kitces

***

***

Share this:

Filed under: Experts Invited, Investing | Tagged: financial advisor compensation, Michael Kitces | 1 Comment »

ME-P SYNDICATIONS:

WSJ.com,

CNN.com,

Forbes.com,

WashingtonPost.com,

BusinessWeek.com,

USNews.com, Reuters.com,

TimeWarnerCable.com,

e-How.com,

News Alloy.com,

and Congress.org

![]()

![]()

BOARD CERTIFICATION EXAM STUDY GUIDES

Lower Extremity Trauma

[Click on Image to Enlarge]

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

![]()

ePodiatryConsentForms.com

ePodiatryConsentForms.com

“Providing Management, Financial and Business Solutions for Modernity”

“Providing Management, Financial and Business Solutions for Modernity”

By Years of experience

Via Michael Kitces

***

***

Filed under: Experts Invited, Investing | Tagged: financial advisor compensation, Michael Kitces | 1 Comment »

![]()

By Rick Kahler MSFS CFP®

Both fee-only financial planning firms and companies that sell financial products are beginning to see some unintended consequences from the recent Department of Labor fiduciary rule.

The rule requires that all financial advisors who deal with an investor’s retirement accounts, including those who sell products, be held to a fiduciary standard. In the past, only RIA’s who are regulated by the SEC were held to such a standard.

The DoL intended the rule to discourage financial salespeople from placing high fee and commission products in retirement accounts. For fee-only advisers, one unintended consequence is an increase in documentation and paperwork, which increases the cost of doing business.

Another unintended consequence that could actually end up hurting consumers may be on the issue of churning.

Churning

Churning describes a broker excessively and needlessly making a lot of trades in a client’s account to generate extra commissions. FINRA, the agency that oversees the sale of financial products, has long discouraged churning, though often the practice only comes to light when a consumer files a complaint.

Still, regulators’ success in discouraging churning has given rise to fee-based brokerage and wrap accounts. These accounts do not compensate brokers on the number and frequency of transactions, but on an ongoing management or advisory fee. It can be a flat fee or one that is determined by a percentage of the assets in the account. This mode of compensation takes away a broker’s incentive to churn accounts. That has to be a good thing, right? Well, not necessarily, if you are a regulator.

***

***

Now, according to financial planner and writer Michael Kitces, the regulators are concerned they have been “too successful” in motivating brokers to charge management fees. Kitces notes the new DoL fiduciary rule will continue to spur a massive shift towards various forms of fee-based brokerage and advisory accounts, giving rise to an emerging new problem: reverse churning.

Reverse Churning

He says reverse churning “is where an advisor charges an ongoing investment management fee … but fails to provide any substantive ongoing investment services.” The broker places a consumer in an investment, collects the annual fee, and never touches the account again. Regulators are worried that brokers have gone from too much activity (churning) to not enough (reverse churning).

With the rise in popularity of passive investing, there is growing interest in the use of ETFs, index funds, and other passive investment vehicles. Passive investing is often framed as a “leave it and forget it” strategy that needs little attention. A lot of research validates that a passive investment strategy is usually superior to an active strategy with more buying and selling of securities.

Kitces notes that while the regulatory concern about reverse churning is appropriate, it “raises troubling concerns when paired with the growing popularity of using index funds, ETFs, and passive investment approaches. How is an advisor supposed to justify an ongoing advisory fee when the right thing for the client to do might really be to do nothing? And what if the bulk of the advisor’s AUM fee is actually for other non-investment (i.e., financial planning) services, paired together with an otherwise passive investment portfolio?”

Assessment

Regulators will probably need to address the difference between reverse churning and implementing a prudent passive investment strategy. That won’t happen before there is a lot of confusion that demands clarification. In the meanwhile, fee-only advisors who embrace a passive investment strategy will have to add another layer of busywork by documenting what they actively do for clients on an ongoing basis. Clearly, this will be easier for fiduciary advisors who also provide financial planning than for those who only provide investment advice.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

***

Filed under: Breaking News, Ethics, Retirement and Benefits, Risk Management | Tagged: AUM, Churning, DOL fiduciary ruling, FINRA, Michael Kitces, reverse churning, Rick Kahler CFP® | 1 Comment »

![]()

LTCI

By Rick Kahler MSFS CFP®

Knowing how long you may live is an important variable to consider in putting together a successful retirement plan. Many online sites can give you a scientific estimate of your life expectancy; one that I recommend is livingto100.com. When I retook the evaluation recently, I was surprised that my life expectancy had increased from 93 to 98.

In an instant I related to one of the greatest fears of older Americans: outliving your sources of income.

The greatest financial risk for depleting retirement resources is an unexpected and lengthy stay in a long-term health care facility, like a nursing home or an assisted living center. Not surprisingly then, “What do you think about long term care insurance (LTCI)?” is one of the questions I often hear.

LTCI is a difficult product to analyze and recommend. It has existed in some form for 40 years, but the industry seems to exist in a continual state of disarray. Low interest rates, low lapse rates, and rising longevity have driven premiums high enough that sales of the insurance have declined 70% from their high in 2002.

The “Guarantee”

Exacerbating the problem is that most LTCI companies issued policies with “guaranteed” premiums.

According to a report by Michael Kitces at kitces.com, just a small variation in actuarial assumptions can have a significant impact on premiums. He says “it’s estimated that as little as a 1% change in interest rates correlates to a 15% required change in premiums to keep an LTC insurance policy actuarially sound. Having a 1% lapse rate instead of a 5% lapse rate can increase future claims for an insurer by as much as 50%.”

As a result, Kitces notes, LTCI providers have struggled to be profitable. In some cases, companies were unable to honor their original prices and had to request permission from state insurance departments to increase premiums on existing policies by as much as 85%. Premiums for new policies have gone even higher.

Simply stated, a guaranteed premium LTC policy needs to be priced high enough to provide a cushion against these variables or the company may be unable to regain profitability with rate increases later.

***

***

One way of addressing this challenge is to eliminate any aspect of a “guaranteed” premium and make long-term care insurance premiums more flexible. One flexible premium policy envisions paying dividends similar to a participating life insurance policy issued by a mutual insurance company. Kitces notes, “To the extent that future claims (or the insurance company’s investment returns) turn out to be better than the original (conservative) projections, the ‘excess’ results will be returned to the policy owner in the form of either an “Insurance Credit” or an “Interest Credit”, to help reduce future premiums.” One such policy is currently priced 20 to 30% under traditionally priced policies with “guaranteed” premiums.

Naturally, there is no guarantee a flexible premium policy will end up costing less than the traditional polity with a guaranteed premium. Probably the biggest concern is the conflict of interest a shareholder-owned company will face in deliberately refunding any savings in the form of dividends to the policy holders. This conflict does not exist with a mutual insurance company, where the owners of the company are the policy holders.

Assessment

Still, the potential benefits look interesting enough that taking a hard look at a flexible premium LTCI policy makes sense. Long-term health care is one of the aspects of aging that most of us don’t want to think about but many of us will need. While LTCI is not for everyone, considering it is a worthwhile part of financial planning for retirement.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

8

***

Filed under: Financial Planning, Health Insurance | Tagged: long term care insurance, LTCI, Michael Kitces, Rick Kahler CFP® | 3 Comments »

![]()

By Rick Kahler MSFS CFP®

The Department of Labor’s groundbreaking new Fiduciary Rule may change the legal responsibilities of advisors who sell financial products for consumers’ retirement accounts.

Financial services industry pundits aren’t sure whether the new rule is a giant step in the right direction or a successful dodging of a bullet by Wall Street.

Original Intent

The original intent was to require those selling financial products for retirement plans to act as fiduciaries—advisors required to put clients’ interests ahead of their own.

One proposed provision was a “restricted asset list” which would have banned the sale of high-commission products like private REITs and annuities to IRAs and other retirement plans. Wall Street brokers were “expecting a punch in the face that would force a dramatic overhaul of how they dealt with their customers,” notes Joshua Brown, CEO of Ritholtz Wealth Management, in an April 6 article at Fortune.com.

As adopted, the final rule allows financial salespeople to still sell all the controversial illiquid high-commissioned products they currently sell, as long as the brokerage firm can document the product is in the client’s best interest. Brown says this amounts to a “love tap.”

The Pundits

Bob Veres, editor of Inside Information, sees the new Fiduciary Rule as still a big win for consumers and fiduciary advisors. In an April 8 column, he writes, “professional financial planners and advisors have achieved a victory, and the Wall Street and independent broker-dealer service models have been dealt a blow.”

Veres argues that the new fiduciary duty to act in the client’s best interest will by itself preclude financial salespeople from justifying the sale of high-commissioned products in IRAs. He also points out that salespeople will no longer be allowed to receive “fat commissions” for recommending annuities and non-traded REITS, and therefore are unlikely to recommend these products.

Financial planner and writer Michael Kitces [a friend of this ME-P and advocate of iMBA’s online Certified Medical Planner® fiduciary focused professional charter education certification program] suggests the DOL’s concession allowing the current questionable financial products to still be purchased by IRAs may be “a brilliantly executed strategy of conceding to the financial services industry the exact parts that didn’t actually matter in the long run . . . yet keeping the key components that mattered the most,” the fiduciary duty to the client.

MORE: http://www.CertifiedMedicalPlanner.org

Brown believes salespeople will continue recommending higher-cost products “so long as a justification can be made for their being recommended (quality, performance, etc.).”

He adds, “Advisors will still be able to sell the proprietary products of their own firm so long as they can enunciate the reason why these products are in their customers’ “best interests” – a hurdle whose height will probably be adjusted on a case-by-case basis as no one really knows what it means yet.”

Kitces contends the new law will ultimately give the consumer the power through the courts to define what is and isn’t in their best interests. He points out:

***

***

“In other words, while the DOL fiduciary rule didn’t outright regulate what Wall Street can and cannot do, it did change the legal standard by which those actions will be judged and ensure that eventually the courts will have the opportunity to rule on these fiduciary conflicts.”

While the new rule only applies to retirement assets, Veres and Brown see it as a step toward requiring a fiduciary standard for all investment advice. I tend to agree.

Assessment

Since so many small investors hold retirement accounts, applying a fiduciary standard to those investments may help more consumers understand the difference between fiduciary advisors and product salespeople. As the industry moves toward full compliance with the rule by the April 2017 deadline, we may see an increase in consumer demand for financial advisors who put clients’ interests first.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

***

Filed under: CMP Program, Ethics, Investing, Risk Management | Tagged: Bob Veres, certified medical planner, DOL's New Fiduciary Rule, Michael Kitces, rick kahler, Ritholtz Wealth Management | 2 Comments »

![]()

Guaranteed living Benefits

By Rick Kahler CFP® www.KahlerFinancial.com

Many investors, panicked by the market crash of 2008-2009, started a search for some type of investment vehicle to protect them from the next market downturn. Some decided the answer was a variable annuity with a “guaranteed living benefit” rider.

Insurance

At first blush, this seems to be a good use of insurance. For a nominal cost, insurance helps us spread the risk of a catastrophe. Consider auto insurance. There is a very small chance I will total my car in the next year. It’s hard to predict whether that will happen, but one thing is sure, it is all or nothing. Either I will or I won’t.

However, predicting the number out of a large group of people who will total their cars becomes much easier. While we don’t know who will total their cars, we do know about what percentage of people will. This predictability allows an insurance company to determine the average number of claims and set an annual premium that covers the anticipated claims and generates the company a profit.

Market Crashes

Insuring market crashes works much differently. Michael Kitces, in his Nerd’s Eye View blog post of November 20, explains, “The problem with trying to insure against a market catastrophe is that the risks don’t ‘average out’ over time, instead, they clump together.” In other words, the insurance company has either no claims or 100% of their policy holders having claims.

Why? When insuring against a stock market decline, there are absolutely no claims when markets trend upward. However, when markets head down, every policyholder potentially has a claim. Kitces notes that usually “companies are very cautious not to back risks that could result in a mass number of claims all at once. This is why most insurance policies have exclusions for terrorist attacks and war.”

Policies

To help insure against this concentrated risk, the companies use several methods to design these policies. One is to collect a fee for the guarantee that funds a reserve to offset potential losses. Kitces says this fee is so “tiny” that it “just doesn’t cut it.” He gives an example of a company with $300 billion of guaranteed annuities where the market declines 25%, exposing the company to a $75 billion loss. A guarantee fee of 0.5% is only $1.5 billion, not enough to even begin to cover the losses.

Loss Mitigation

Another way the companies mitigate their loss is that, unlike auto insurance, these policies do not pay immediate benefits. If the market drops by 50%, you don’t get a check for your original investment plus a fair return for the time they had your money. What you get is a promise to pay you a lifetime stream of income, usually at some date in the future. If you had a portfolio of mutual funds holding thousands of companies and purchased a “guaranteed living benefit,” you actually transfer the diversified risk to one insurance company that has actually concentrated, rather than spread, the risk.

Variable Annuities?

Does this mean you should avoid variable annuities? No, as not all of them concentrate their risk. Most allow you to invest in a broad range of securities and spread your risk. Consider avoiding annuities that have a “guaranteed living benefit” and fees of over 1%.

Other Options

Kitces cites two other options for investors. One is to keep your portfolio invested in mutual funds that hold a broad selection of securities and simply lower your risk by owning less equity and equity-like investments and more bonds.

A second is to spend less, keeping your withdrawal rate under 3%.

Assessment

Practicing both of these strategies is a way of providing your own insurance against market crashes.

More:

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Link: http://feeds.feedburner.com/HealthcareFinancialsthePostForcxos

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

DICTIONARIES: http://www.springerpub.com/Search/marcinko

PHYSICIANS: www.MedicalBusinessAdvisors.com

PRACTICES: www.BusinessofMedicalPractice.com

HOSPITALS: http://www.crcpress.com/product/isbn/9781466558731

CLINICS: http://www.crcpress.com/product/isbn/9781439879900

BLOG: www.MedicalExecutivePost.com

FINANCE: Financial Planning for Physicians and Advisors

INSURANCE: Risk Management and Insurance Strategies for Physicians and Advisors

![]()

![]()

Filed under: Insurance Matters, Investing | Tagged: "guaranteed living benefit", Michael Kitces, Rick Kahler CFP®, variable annuity | 1 Comment »

![]()

Option of Last Resort -OR- Something Else?

By Rick Kahler CFP® MS ChFC CCIM

Like most financial planners, I generally recommend not thinking of your home as a part of an investment portfolio or a source of retirement income. One possible exception to this rule, for medical professionals to consider, is a reverse mortgage.

Lenders

Lenders which are FHA-approved can offer Home Equity Conversion Mortgages, or HECM’s. These are insured by the U.S. government and allow homeowners age 62 and older to borrow against the equity in their homes. When the homeowner dies or moves out, the property is sold to repay the loan. Any equity left over belongs to the owners or their heirs. Any outstanding loan balance must be forgiven by the lender.

Reverse mortgages may be useful for elderly people in good health who have limited income or assets but who are living in paid-for homes.

Until now, I have viewed them as options of last resort. But, a new report by financial planner Michael Kitces CFP® has given me some cause to re-evaluate that position.

Link: http://www.kitces.com/index.php

Disadvantages

Typical Uses

Example

Kitces uses the example of a 70-year old couple paying $1000 a month for a $175,000 traditional mortgage on a $450,000 property. A $175,000 reverse mortgage would eliminate the $1,000 payment. Assuming the net principal limit for the borrower was $250,000 on the property, they could use the reverse mortgage to extract an additional $75,000 of equity. They could receive this in a lump sum payment, create a $75,000 line of credit, or receive lifetime monthly payments based on the $75,000.

Let’s assume this couple’s monthly expenses, including the mortgage payment, are $5,000. They receive $1,500 a month from Social Security and withdraw $3,500 a month from their $600,000 investments. The total $42,000 annual withdrawal is an unsustainably high 7% of their portfolio.

The reverse mortgage would eliminate the $1,000 mortgage payment and reduce the investment withdrawal to $2,500 a month. This totals $30,000 annually, a more sustainable withdrawal rate of 5%. Investing the $75,000 of excess proceeds would produce additional monthly income and reduce the withdrawal rate even further. Using a reverse mortgage in this way makes sense if the lost home equity is offset by an increase in investment assets.

Assessment

We’ll look at some other reverse mortgage options another time, so stay tuned to this ME-P, and subscribe today!

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

![]()

Filed under: Financial Planning, Mortgage Electronic Registry System, Retirement and Benefits | Tagged: FHA, HECMs, Home Equity Conversion Mortgages, Michael Kitces, Rethinking the Reverse Mortgage Paradigm, reverse mortgages, rick kahler | 10 Comments »

![]()

Follow Paretto’s Law – or Learn Something Unique and Compete?

By Dr. David Edward Marcinko; FACFAS, MBA, CMP™

[Publisher-in-Chief]

Michael Kitces is an industry pundit, and well known certified financial planner [CFP], who writes for a financial advisory and financial planner audience at thewebsite Nerd’s Eye View:

He is a bright guy, who holds the following professional degrees and designations:

Yet, in a recent essay, he laments that all the CFPs® in the country added together don’t have as much reach, or impact, as three mass marketing gurus: Suze Orman, David Bach, and Dave Ramsey. And, he is correct.

Markets Vary

These gurus, and the CFPs®, serve different markets for sure. The gurus’ products are free or inexpensive. Their messages are simple and actionable. Once you go beyond the simple messages, however, you will find the gurus no longer satisfying. So, it’s no coincidence that the three gurus focus on controlling spending and getting out of debt. Why?

Eighty percent of us do need to get out of debt and control our spending, period!

Link: Do Financial Planners Have Something To Learn From Suze Orman and Dave Ramsey?

Pareto’s Law

Here is where the mass market is located, said economist V. Pareto PhD more than a century ago. The Pareto principle (also known as the 80-20 rule, the law of the vital few, or the principle of scarsity) states that, for many events, roughly 80% of the effects come from 20% of the causes. It is a common thumb-rule in business; e.g., “80% of your sales come from 20% of your clients”.

Look, most clients can’t control their income but they can be taught to control spending and debt habits [needs versus wants]. Most patients need a family doctor; not a brain surgeon. And, most of us do not have Einstein’s intelligence, Gate’s wealth, or Hercules’s strength.

But, our lives can vastly be improved by 80%, with just 20% more effort and cost. This is what the gurus know – most of us are average – not so the CFPs® who believe we all need a comprehensive financial plan and have the ability to pay for it and the time to execute and monitor it.

Assessment

And so, CFPs® can’t charge an 80% premium – to 80% of the population – when clients don’t need or want a comprehensive financial plan. Or, when clients can be better off by 80%, and such success can be had for 20% of the cost and effort offered by the CFPs®.

Basic supply-demand economics 101! Ford autos are fine – we all don’t need or want a Mercedes.

More confusing is the fact that even the CFPs® themselves are suspect since prior to 2008 a college degree was not required for the certification mark. And, having same allows the practitioner no additional diagnostic or interventional tools.

IOW: Whatever a CFP® can do – a non-CFP® can do. And, it is increasingly considered by the well-informed …. to be a marketing mark …. to hold a marketing mark. This is akin to being famous; for being famous. That’s why I resigned my CFP® mark years ago.

Full Disclosure: I am the Founder of the: http://www.CertifiedMedicalPlanner.org online program. CMP™ certificants – like doctors – hold fiduciary accountability at all times and with unique healthcare industry specificity.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

![]()

Filed under: "Advisors Only", Career Development, CMP Program, Financial Planning, Practice Management | Tagged: CFP, CMP, Dave Ramsey, david marcinko, Michael Kitces, Suze Orman, www.CertifiedMedicalPlanner | 6 Comments »