BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on February 21, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Dan Ariely PhD

THE IRRATIONAL ECONOMIST

***

***

Of course you don’t need a human financial advisor … until you do. Today, we’ve had unfettered internet access to a wide range of investments, opinions and models for at least two decades. So, why the bravado to go it alone; fifteen positive years for equities, since 2009! Yet, the DJIA, S&P 500 and NASDAQ just plunged and plummeted today!

The financial advisor’s role is to remove the human element and emotion from investing decisions for something as personal as your wealth. Emotion drives the retail investor to sell low (fear) and buy high (greed). This is the reason why the average equity returns for retail investors is less than half of the S&P 500’s returns.

No, of course you don’t need a human financial advisor … until you do.

Of course you don’t need a human financial advisor … until you do.

Today, we’ve had unfettered internet access to a wide range of investments, opinions and models for at least two decades. So, why the bravado to go it alone; five straight positive years for equities, since 2009!

The financial advisor’s role is to remove the human element and emotion from investing decisions for something as personal as your wealth. Emotion drives the retail investor to sell low (fear) and buy high (greed). This is the reason why the average equity returns for retail investors is less than half of the S&Ps returns.

No, of course you don’t need a human financial advisor … until you do. And when you do, it may be too late.

***

Dan Ariely PhD

[The Irrational Economist]

OUR TEXT BOOK

[BY DOCTORS – FOR DOCTORS – PEER REVIEWED]

[Chapter One]

UNIFYING THE PHYSIOLOGIC AND PSYCHOLOGIC FINANCIAL PLANNING DIVIDE [Holistic Life Planning, Behavioral Economics, Trading Addiction and the Art of Money]

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register. It is fast, free and secure.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

As human beings, our brains are booby-trapped with psychological barriers that stand between making smart financial decisions and making dumb ones. The good news is that once you realize your own mental weaknesses, it’s not impossible to overcome them.

In fact, Mandi Woodruff, a financial reporter whose work has appeared in Yahoo! Finance, Daily Finance, The Wall Street Journal, The Fiscal Times and the Financial Times among others; related the following mind-traps in a September 2013 essay for the finance vertical Business Insider; as these impediments are now entering the lay-public zeitgeist.

***

Anchoring happens when we place too much emphasis on the first piece of information we receive regarding a given subject. For instance, when shopping for a wedding ring a salesman might tell us to spend three months’ salary. After hearing this, we may feel like we are doing something wrong if we stray from this advice, even though the guideline provided may cause us to spend more than we can afford.

Myopia makes it hard for us to imagine what our lives might be like in the future. For example, because we are young, healthy, and in our prime earning years now, it may be hard for us to picture what life will be like when our health depletes and we know longer have the earnings necessary to support our standard of living. This short-sightedness makes it hard to save adequately when we are young, when saving does the most good.

Gambler’s fallacy occurs when we subconsciously believe we can use past events to predict the future. It is common for the hottest sector during one calendar year to attract the most investors the following year. Of course, just because an investment did well last year doesn’t mean it will continue to do well this year. In fact, it is more likely to lag the market.

Avoidance is simply procrastination. Even though you may only have the opportunity to adjust your health care plan through your employer once per year, researching alternative health plans is too much work and too boring for us to get around to it. Consequently, we stick with a plan that may not be best for us.

Loss aversion affected many investors during the stock market crash of 2008. During the crash, many people decided they couldn’t afford to lose more and sold their investments. Of course, this caused the investors to sell at market troughs and miss the quick, dramatic recovery.

Overconfident investing happens when we believe we can out-smart other investors via market timing or through quick, frequent trading. Data convincingly shows that people who trade most often underperform the market by a significant margin over time.

Mental accounting takes place when we assign different values to money depending on where we get it from. For instance, even though we may have an aggressive saving goal for the year, it is likely easier for us to save money that we worked for than money that was given to us as a gift.

Herd mentality makes it very hard for humans to not take action when everyone around us does. For example, we may hear stories of people making significant profits buying, fixing up, and flipping homes and have the desire to get in on the action, even though we have no experience in real estate.

Posted on October 20, 2021 by Dr. David Edward Marcinko MBA MEd CMP™

OVERHEARD IN THE DOCTOR’S LOUNGE

By Jaan E. Sidorov MD

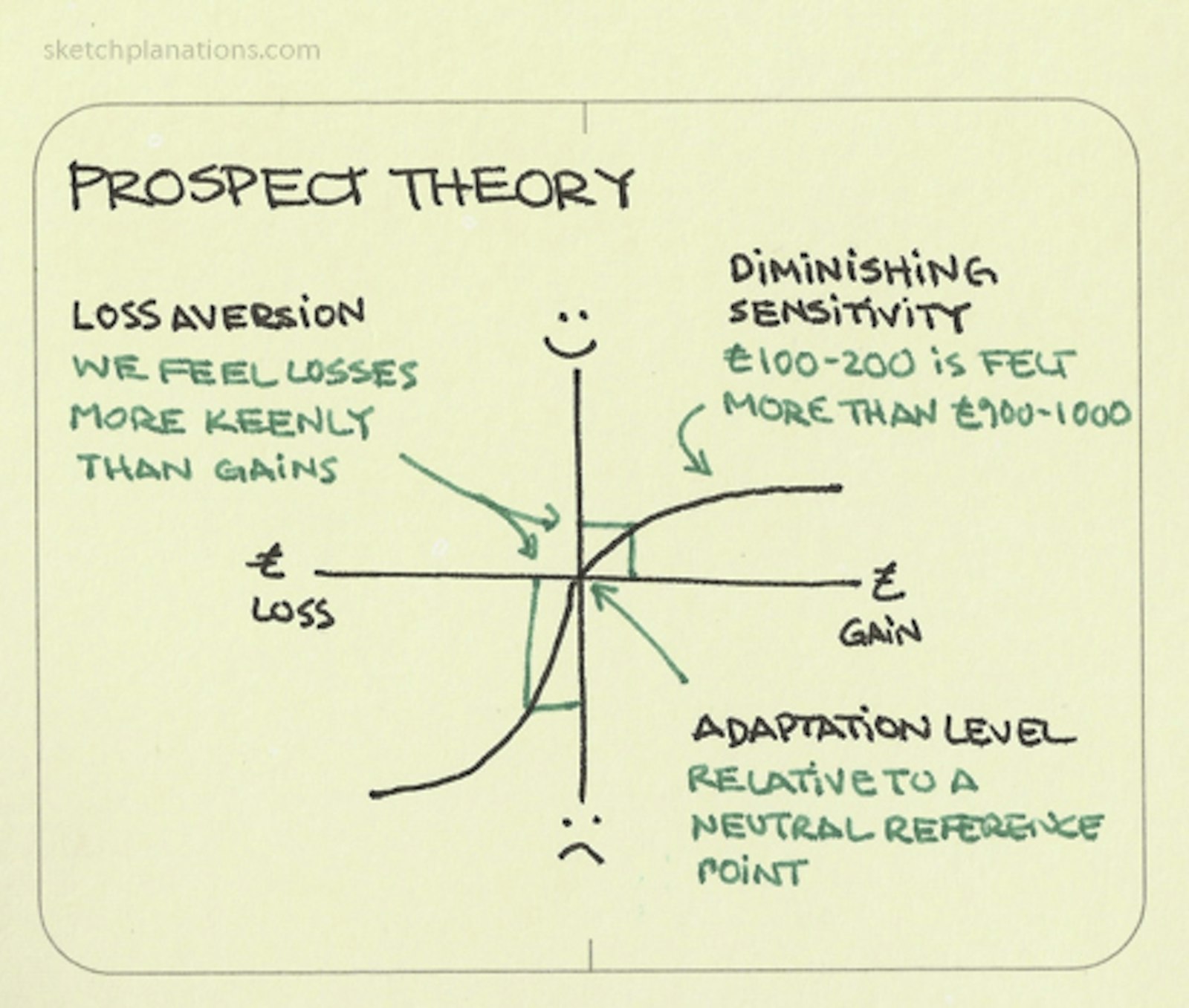

*** DEFINITION: Prospect theory is a theory of behavioral economics and behavioral finance that was developed by Daniel Kahneman and Amos Tversky in 1979. The theory was cited in the decision to award Kahneman the 2002 Nobel Memorial Prize in Economics.

Amanda, an RN client, was just informed by her financial advisor that she needed to re-launch her 403-b retirement plan. Since she was leery about investing, she quietly wondered why she couldn’t DIY. Little does her FA know that she doesn’t intend to follow his advice, anyway! So, what went wrong?

The answer may be that her advisor didn’t deploy a behavioral economics framework to support her decision-making. One such framework is the “prospect theory” model that boils client decision-making into a “three step heuristic.”

Prospect theory makes the unspoken biases that we all have more explicit. By identifying all the background assumptions and preferences that clients [patients] bring to the office, decision-making can be crafted so that everyone [family, doctor and patient] or [FA, client and spouse] is on the same page.

****

*** Briefly, the three steps are:

Simplify choices by focusing on the key differences between investment [treatment] options such as stock, bonds, cash, and index funds.

Understanding that clients [patients] prefer greater certainty when it comes to pursuing financial [health] gains and are willing to accept uncertainty when trying to avoid a loss [illness].

Cognitive processes lead clients and patients to overestimate the value of their choices thanks to survivor bias, cognitive dissonance, appeals to authority and hindsight biases.

ASSESSMENT

Much like in healthcare today, the current mass-customized approaches to the financial services industry fall short of recognizing more personalized advisory approaches like prospect theory and assisted client-centered investment decision-making.