BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on May 5, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Vitaliy Katsenelson CFA

***

***

“Any time you make a bet with the best of it, where the odds are in your favor, you have earned something on that bet, whether you actually win or lose the bet. By the same token, when you make a bet with the worst of it, where the odds are not in your favor, you have lost something, whether you actually win or lose the bet.”

– David Sklansky, The Theory of Poker

Over a lifetime, active investors will make hundreds, often thousands of investment decisions. Not all of those decisions will work out for the better. Some will lose and some will make us money. As humans we tend to focus on the outcome of the decision rather than on the process.

On a behavioral level, this makes sense. The outcome is binary to us – good or bad, we can observe with ease. But the process is more complex and is often hidden from us.

One of two things (sometimes a bit of both) can unite great investors: process and randomness (luck). Unfortunately, there is not much we can learn from randomness, as it has no predictive power. But the process we should study and learn from. To be a successful investor, all you need is a successful process and the ability (or mental strength) to stick to it.

Several years ago, I was on a business trip. I had some time to kill so I went to a casino to play blackjack. Aware that the odds were stacked against me, I set a $40 limit on how much I was willing to lose in the game.

I figured a couple hours of entertainment, plus the free drinks provided by the casino, were worth it. I was never a big gambler (as I never won much). However, several days before the trip I had picked up a book on blackjack on the deep discount rack in a local bookstore. All the dos and don’ts from the book were still fresh in my head. I figured if I played my cards right I would minimize the house advantage from 2-3 per cent to 0.5 per cent.

Wanting to get as much mileage out of my $40 as possible, I found a table with the smallest minimum bet requirement. My thinking was that the smaller the hands I played, the more time it would take for the casino’s advantage to catch up with me and take my money.

I joined a table that was dominated by a rowdy, half-drunken blue-collar worker who told me several times that it was his payday (literally: he was holding a stack of $100 bills in his hand) and that he was winning. I played by the book. But it did not matter. Luck was not on my side and my $40 was thinning with every hand.

Meanwhile, the rowdy guy was making every wrong move. He would ask for an extra card when he had a hard 18 while the dealer showed 6. The next card he drew would be a 3, giving him 21. Then the dealer would get a 10 and then a 2 (on top of the 6 that already showed), leaving him with 18. The rowdy guy barely paid attention to the cards.

Stocks were decimated yesterday in the first full trading day following President Trump’s tariff announcement. It was the biggest single-day decline since the start of the Covid-19 pandemic in March 2020. Every Magnificent Seven stock was battered—Apple worst of all. And so perhaps it is a good time to discuss the concept of “Money Scripts”.

***

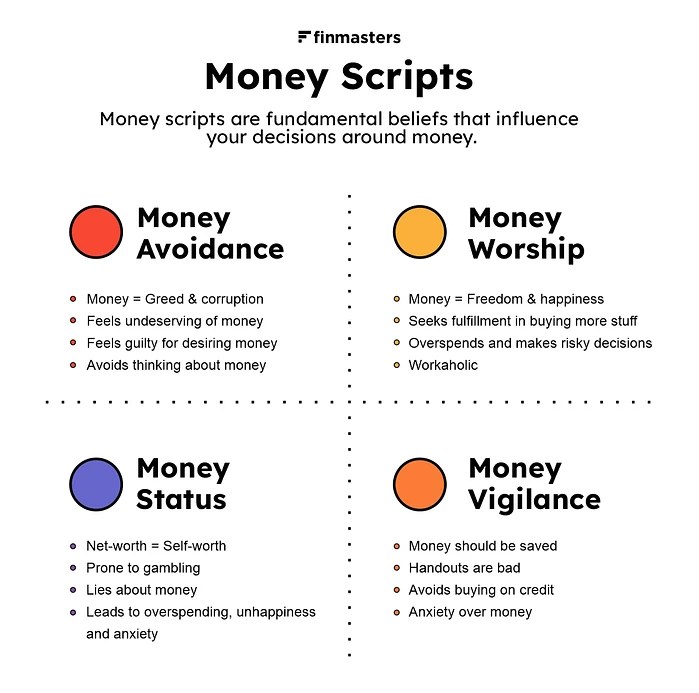

Money Scripts are unconscious beliefs about money that are typically only partially true, are developed in childhood, and drive adult financial behaviors. Money scripts may be the result of “financial flashpoints,” which are salient early experiences around money that have a lasting impact in adulthood. Money scripts are often passed down through the generations and social groups often share similar money scripts. And so, we argue that Money scripts are at the root of all illogical, ill-advised, self-destructive, or self-limiting financial behaviors.

In research at Kansas State University [KSU], researchers identified four distinct Money script patterns, which are associated with financial health and predict financial behaviors. These include: (a) money avoidance, (b) money worship, (c) money status, and (d) money vigilance [personal communication Brad Klontz, PsyD, CFP®, Kenneth Shubin-Stein, MD, MPH, MS, CFA and Sonya Britt, PhD, CFP®].

And so, we all like to think our financial decisions are fully rational, but the truth is that our subconscious beliefs have a dramatic impact on our money and financial decisions. These money scripts are important to know and understand. A summary is below:

Money Avoidance

Money avoidance scripts are illustrated by beliefs such as “Rich people are greedy,”“It is not okay to have more than you need,” and “I do not deserve a lot of money when others have less than me.” Money avoiders believe that money is bad or that they do not deserve money. They believe that wealthy people are corrupt and there is virtue in living with less money. They may sabotage their financial success or give money away even though they cannot afford to do so. Money avoidance scripts may be associated with lower income and lower net worth and predict financial behaviors including ignoring bank statements, overspending, financial dependence on others, financial enabling of others, and having trouble sticking to a budget.

Money Worship

Money worship is typified by beliefs such as “More money will make you happier,” “You can never have enough money,” and “Money would solve all my problems.” Money worshipers are convinced that money is the key to happiness. At the same time, they believe that one can never have enough. Money worships have lower income, lower net worth, and higher credit card debt. They are more likely to be hoarders, spend compulsively, and put work ahead of family.

Money Status

Money status scripts include “I will not buy something unless it is new,” “Your self-worth equals you net worth,” and “If something isn’t considered the ‘best’ it is not worth buying.” Money status seekers see net worth and self-worth as being synonymous. They pretend to have more money than they do and tend to overspend as a result. They often grew up in poorer families and believe that the universe should take care of their financial needs if they live a virtuous life. Money status scripts are associated with compulsive gambling, overspending, being financially dependent on others, and lying to one’s spouse about spending.

Money Vigilance

Money vigilant beliefs include “It is important to save for a rainy day,” “You should always look for the best deal, even if it takes more time,” and “I would be a nervous wreck if I did not have an emergency fund.” The money vigilants are alert, watchful and concerned about their financial welfare. They are more likely to save and less likely to buy on credit. As a result, they tend to have higher income and higher net worth. They also have a tendency to be anxious about money and are secretive about their financial status outside of their household. While money vigilance is associated with frugality and saving, excessive anxiety can keep someone from enjoying the benefits that money can provide.

Identification

When money scripts are identified, it is helpful to examine where they came from. A simple behavioral finance technique involves reflecting on the following questions:

What three lessons did you learn about money from your mother?

What three lessons did you learn about money from your father?

What is your first memory around money?

What is your most painful money memory?

What is your most joyful money memory?

What money scripts emerged for you from this experience?

How have they helped you?

How have they hurt you?

What money scripts do you need to change?

Conclusion

Ideally, from a balanced middle ground, we can see past the limitations of money scripts, our self and others who are polarized. Those who believe “Money is meant to be spent” or “Money is meant to be saved” have a world view that results in extreme positions. Labeling them as “correct” or “wrong” is not a useful way to try to shift anyone’s polarized money script beliefs.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com