SALES PSYCHOLOGY FOR INVESTMENT ADVISORS, FINANCIAL ADVISORS, INSURANCE AGENTS, WEALTH MANAGERS AND FINANCIAL PLANNERS

By Dr. David Edward Marcinko; MBA MEd CMP®

http://www.MarcinkoAssociates.com

***

***

SPONSOR: http://www.CertifiedMedicalPlanner.org

***

***

Stocks were decimated yesterday in the first full trading day following President Trump’s tariff announcement. It was the biggest single-day decline since the start of the Covid-19 pandemic in March 2020. Every Magnificent Seven stock was battered—Apple worst of all. And so perhaps it is a good time to discuss the concept of “Money Scripts”.

***

Money Scripts are unconscious beliefs about money that are typically only partially true, are developed in childhood, and drive adult financial behaviors. Money scripts may be the result of “financial flashpoints,” which are salient early experiences around money that have a lasting impact in adulthood. Money scripts are often passed down through the generations and social groups often share similar money scripts. And so, we argue that Money scripts are at the root of all illogical, ill-advised, self-destructive, or self-limiting financial behaviors.

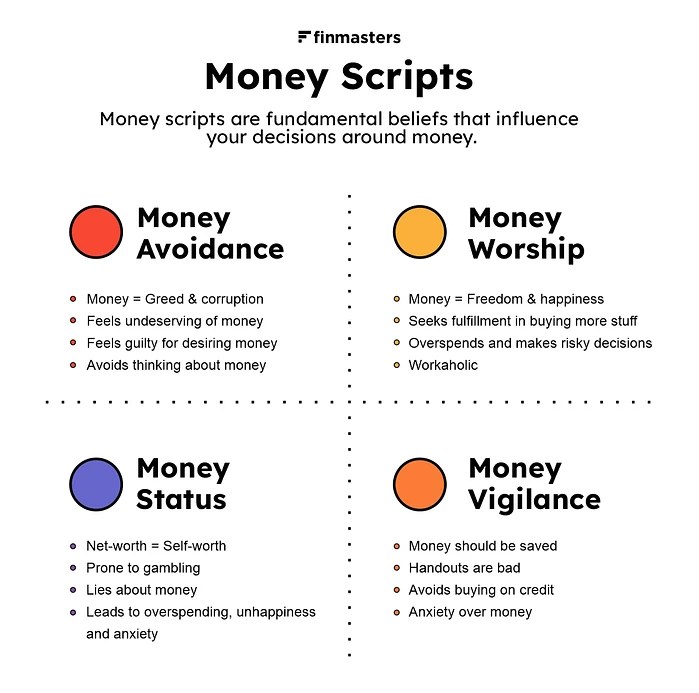

In research at Kansas State University [KSU], researchers identified four distinct Money script patterns, which are associated with financial health and predict financial behaviors. These include: (a) money avoidance, (b) money worship, (c) money status, and (d) money vigilance [personal communication Brad Klontz, PsyD, CFP®, Kenneth Shubin-Stein, MD, MPH, MS, CFA and Sonya Britt, PhD, CFP®].

And so, we all like to think our financial decisions are fully rational, but the truth is that our subconscious beliefs have a dramatic impact on our money and financial decisions. These money scripts are important to know and understand. A summary is below:

Money Avoidance

Money avoidance scripts are illustrated by beliefs such as “Rich people are greedy,” “It is not okay to have more than you need,” and “I do not deserve a lot of money when others have less than me.” Money avoiders believe that money is bad or that they do not deserve money. They believe that wealthy people are corrupt and there is virtue in living with less money. They may sabotage their financial success or give money away even though they cannot afford to do so. Money avoidance scripts may be associated with lower income and lower net worth and predict financial behaviors including ignoring bank statements, overspending, financial dependence on others, financial enabling of others, and having trouble sticking to a budget.

Money Worship

Money worship is typified by beliefs such as “More money will make you happier,” “You can never have enough money,” and “Money would solve all my problems.” Money worshipers are convinced that money is the key to happiness. At the same time, they believe that one can never have enough. Money worships have lower income, lower net worth, and higher credit card debt. They are more likely to be hoarders, spend compulsively, and put work ahead of family.

Money Status

Money status scripts include “I will not buy something unless it is new,” “Your self-worth equals you net worth,” and “If something isn’t considered the ‘best’ it is not worth buying.” Money status seekers see net worth and self-worth as being synonymous. They pretend to have more money than they do and tend to overspend as a result. They often grew up in poorer families and believe that the universe should take care of their financial needs if they live a virtuous life. Money status scripts are associated with compulsive gambling, overspending, being financially dependent on others, and lying to one’s spouse about spending.

Money Vigilance

Money vigilant beliefs include “It is important to save for a rainy day,” “You should always look for the best deal, even if it takes more time,” and “I would be a nervous wreck if I did not have an emergency fund.” The money vigilants are alert, watchful and concerned about their financial welfare. They are more likely to save and less likely to buy on credit. As a result, they tend to have higher income and higher net worth. They also have a tendency to be anxious about money and are secretive about their financial status outside of their household. While money vigilance is associated with frugality and saving, excessive anxiety can keep someone from enjoying the benefits that money can provide.

Identification

When money scripts are identified, it is helpful to examine where they came from. A simple behavioral finance technique involves reflecting on the following questions:

- What three lessons did you learn about money from your mother?

- What three lessons did you learn about money from your father?

- What is your first memory around money?

- What is your most painful money memory?

- What is your most joyful money memory?

- What money scripts emerged for you from this experience?

- How have they helped you?

- How have they hurt you?

- What money scripts do you need to change?

Conclusion

Ideally, from a balanced middle ground, we can see past the limitations of money scripts, our self and others who are polarized. Those who believe “Money is meant to be spent” or “Money is meant to be saved” have a world view that results in extreme positions. Labeling them as “correct” or “wrong” is not a useful way to try to shift anyone’s polarized money script beliefs.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit a RFP for speaking engagements: CONTACT: MarcinkoAdvisors@outlook.com

COMMENTS APPRECIATED

Read, Refer, Like and Subscribe

***

***

Share this:

Filed under: "Advisors Only", CMP Program, Ethics, Experts Invited, Financial Planning, Glossary Terms, Health Economics, Insurance Matters, Investing, Marcinko Associates, mental health, Portfolio Management | Tagged: anxiety, avoidance, behavioral economics, behavioral finance, Brad Klontz, CMP, Daivd Marcinko, financial advisors, financial planners, gambling, greed, health, insurance agents, investment advisors, Kenneth Shubin Stein, mental health, net worth, overspending, personal-development, personal-growth, psychiatry, psychology, self worth, Sonya Britt, status, subconscious, vigilance, worship | Leave a comment »