BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

The 30-Day SEC Yield represents net investment income earned by a fund over a 30-day period, expressed as an annual percentage rate based on the fund’s share price at the end of the 30-day period. The SEC Yield should be regarded as an estimate of the fund’s rate of investment income, and it may not equal the fund’s actual income distribution rate, the income paid to a shareholder’s account, or the income reported in the fund’s financial statements.

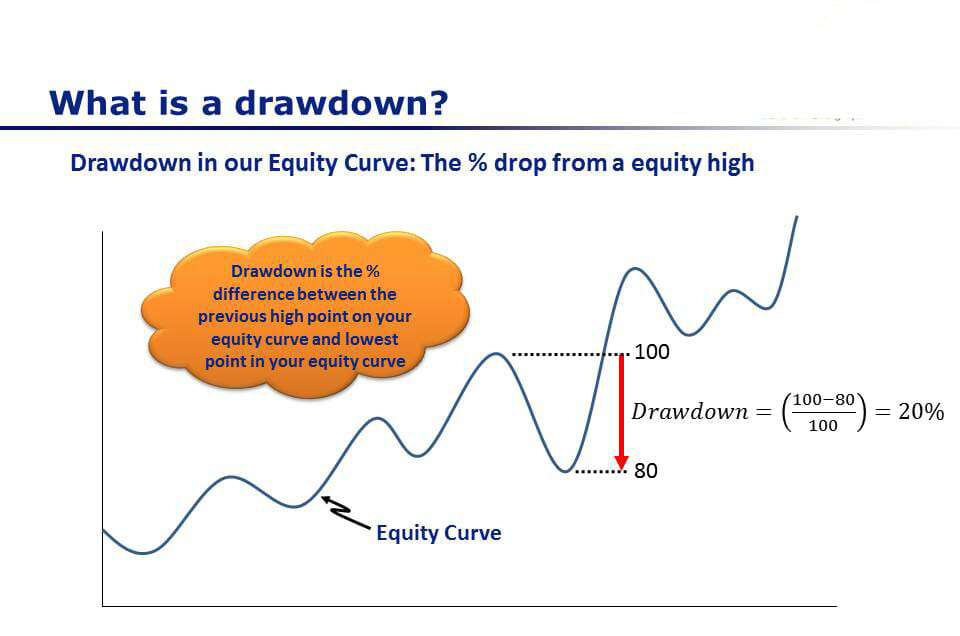

The 52-Week Drawdown is the lowest price at which a security, such as a stock, has traded during the previous 52 weeks

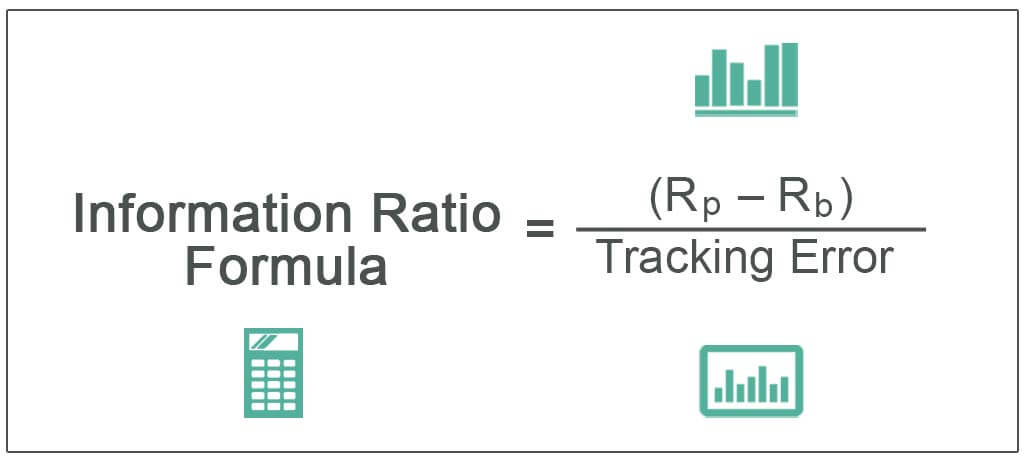

The Information Ratio (IR) is a risk-adjusted rate of return measure for comparing the performance of active investment managers over time. Its purpose is to help determine how much return an active portfolio manager has added per unit of active management risk.

Think of IR as a Sharpe Ratiofor active investment management; the IR is more focused than the Sharpe Ratio. Starting with the Sharpe Ratio’s formula, if we replace the excess return in the numerator with a portfolio’s active return (the average annualized return of an actively managed portfolio minus the average annualized return of the portfolio’s benchmark over a given period, adjusted for the portfolio’s market risk exposure), and you replace the Sharpe Ratio’s standard deviation of excess returns in the denominator with the standard deviation of a portfolio’s active returns over the period, you have the IR.

While the Sharpe Ratio expresses the amount of excess return per unit of overall risk, the IR computes only the active management-driven (alpha) returns per unit of alpha-driven risk. And while the Sharpe Ratio’s excess returns are calculated with regard to what is considered to be a relatively risk-free asset, such as a U.S. Treasury bill, the IR’s active returns are calculated with regard to each portfolio’s specific market benchmark.

The higher the IR, the better. The IR should be measured over a meaningful period of time, typically at least three to five years. The IR is not perfect–it can be influenced by external factors such as changes in market volatility. The standard deviation of active returns in the IR’s denominator is called tracking error. Tracking error will tend to increase in volatile markets for even the best active managers.

Collateralized Mortgage Obligations (CMOs) are a form of securitized debt derived from mortgage-backed securities. It’s a form of derivative security. Like most MBS pass-through securities, CMOs are typically backed by pools of residential mortgages and their payments. But not all investors want to receive the monthly payments of principal and interest that “plain vanilla” MBS pass-throughs offer–some prefer just the principal, some prefer just the interest, or some want payments with other particular/special characteristics.

For them, the cash flows from MBS can be pooled and structured into many classes of CMOs with different maturities and payment schedules, creating securities with very specific characteristics and behaviors. These characteristics and behaviors can vary widely. Some CMOs can offer less risk than “plain-vanilla” MBS, or can help offset other forms of risk in a diversified portfolio, but others can be much more volatile.

CMOs typically have two or more bond classes, called tranches. Each tranche has its own expected maturity and cash flow pattern. The unique cash flow patterns of each CMO tranche allow investors to tailor their mortgage exposure to meet a range of investment objectives, since different classes can have different risk/return characteristics.

Posted on December 13, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

What Is a Public Benefit Corporation?

A benefit corporation—also known as a B Corporation—has shareholders who own the company, unlike a non-profit. So making money is the point, just not the whole point.

While non-profits (or not-for-profits) serve a public benefit and don’t make any profits, benefit corporations want to make money while still serving a greater purpose than itself “and a desire for the corporation to help make the world a better place,” according to Rick Bell of Harvard Business Services.

Posted on December 13, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

MEDICAL EXECUTIVE-POST–TODAY’SNEWSLETTERBRIEFING

FRIDAY 13th = Triskaidekaphobia

***

Essays, Opinions and Curated News in Health Economics, Investing, Business, Management and Financial Planning for Physician Entrepreneurs and their Savvy Advisors and Consultants

“Serving Almost One Million Doctors, Financial Advisors and Medical Management Consultants Daily“

A Partner of the Institute of Medical Business Advisors , Inc.

The Dow Jones Industrial Average (^DJI) was down and the S&P 500 (^GSPC) were both about 0.5%. The tech-heavy NASDAQ Composite (^IXIC) fell roughly 0.6% while shares of Apple (AAPL) rallied less than 1% to close at a record high.

In bonds, the 10-year Treasury yield (^TNX) added 5 basis points to hit 4.32%, its highest closing level since November 22nd.

On a day where President-elect Donald Trump rang the opening bell at the New York Stock Exchange, Wall Street failed to build on a furious rally that has picked up steam after his election win. In focus was fresh inflation data, which helped cast doubt on investor confidence for the path of interest rates ahead.