By Staff Reporters

***

***

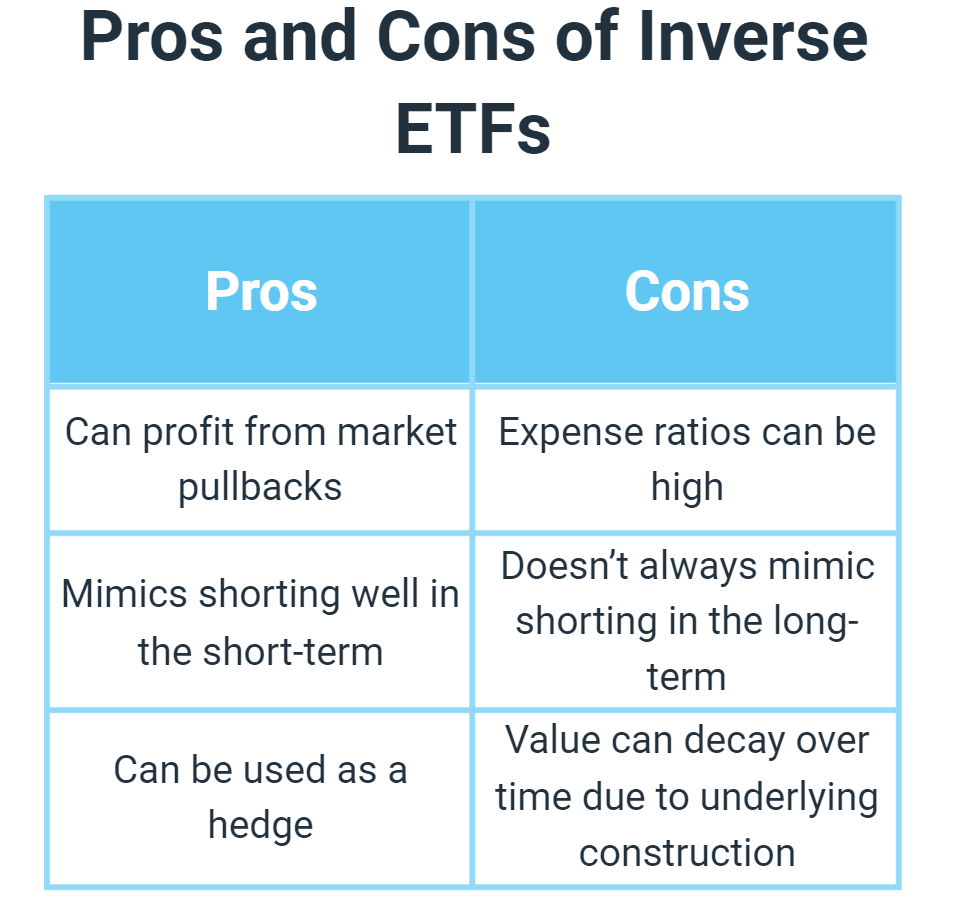

What are inverse ETFs?

An inverse ETF, often known as a bear or short ETF, is an exchange-traded fund designed to profit from a market decline. These short-term, publicly traded investments are utilized by investors who believe that a particular market or individual security will lose value in the near future. They may use inverse ETFs as a way of hedging losses during a downturn.

“Inverse ETFs are a tool to hedge a stock portfolio,” according to John DeYonker. “If the S&P 500 is your benchmark, and it goes up 1%, then your hedge will go down 1% and vice versa. Hedging with inverse ETFs can reduce volatility for investors—it’s like insurance.”

Investors may also use inverse ETFs as a way to take advantage of a predicted decline. In this way, they may be used as an alternative to short selling. For example, if an investor believes that the oil industry will have a setback in the immediate future, they may choose to purchase an inverse ETF of securities tied to energy producers. If correct in their prediction, the investor’s inverse ETF may recognize a profit. If the investor is incorrect, and the market or individual security increases in price, they may see a loss.

An investor who believes that the S&P 500 will decline, for example, may choose to purchase shares of the ProShares Short S&P 500. This inverse ETF’s value is inversely proportional to the overall S&P 500 index.

Inverse ETFs are generally considered to be highly volatile investments, as their losses typically compound daily. This makes inverse ETFs more risky than the index to which they are tied.

CITE: https://en.wikipedia.org/wiki/Exchange-traded_fund

***

COMMENTS APPRECIATED

Thank You

RELATED: https://medicalexecutivepost.com/2021/12/26/podcast-what-is-a-leveraged-etf/?preview=true

***

Share this:

Filed under: "Ask-an-Advisor", Experts Invited, Funding Basics, Glossary Terms, Investing | Tagged: Enhanced Leveraged Fund., ETF, ETFs, inverse ETFs, leveraged ETF, Short ETFs | Leave a comment »