BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] E-mail: MarcinkoAdvisors1738@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on April 10, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

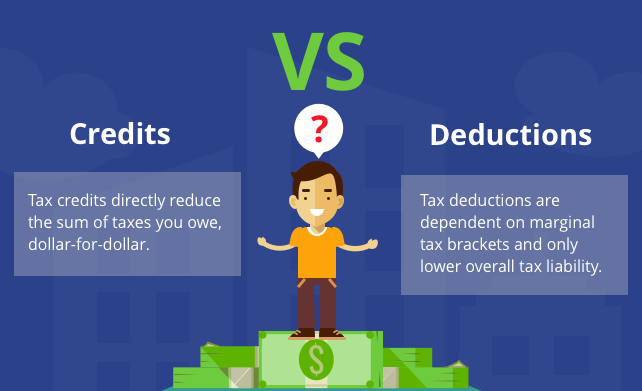

What is a tax deduction?

A deduction reduces the amount of income you pay taxes on, which means you could pay less in taxes. You subtract deductions from your income before calculating how much taxes you owe. How much a deduction saves you depends on your income tax bracket.

To calculate how much a deduction could reduce your taxes, you multiply the amount of the deduction by your marginal tax rate. For example, if a deduction is worth $5,000 and you are in the 10% tax bracket (the lowest), the deduction would reduce your taxes by $500.

A deduction’s value to you is tied to your tax rate. So if you’re paying a higher tax rate, you can reap more of a deduction’s benefit. The lower your tax rate, the less benefit a deduction will have for you. Imagine that you take a $5,000 deduction, but you’re in the 35% tax bracket — the second highest. Now you’re saving $1,750 in taxes.

On the other hand, a credit is a dollar-for-dollar reduction in the amount of tax you owe. For example, if you qualify for a $1,000 tax credit of some kind and owe $5,000 in taxes, that credit will reduce your tax burden to $4,000.

***

But – Do Not Claim Too Many Tax Deductions

Deductions are enticing to taxpayers because they can reduce the amount of your income before you calculate the tax you owe, which in turn might significantly lower how much you have to pay in taxes or increase your refund. But that doesn’t mean you should go wild writing things off on your tax returns, as experts say claiming too many deductions is the most common reason people end up getting audited by the IRS.

Don’t try writing off deductions that are no longer accepted by the IRS. The tax code has changed over the years, and there are some things the tax agency no longer recognizes. You should remember that some of the tax write-offs were terminated by the IRS, including deductions on alimony, moving expenses, and any expenses related to investing, hobbies, and tax preparation.

Posted on April 10, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

U.S. stocks ended mixed the past week with the technology-laden NASDAQ Composite and S&P 500 closing lower as investors continued to digest the Federal Reserve’s plans to aggressively raise interest rates and shrink its balance sheet. Key inflation data and corporate earnings reports loom next week.

The Dow Jones Industrial Average rose 137.55 points, or 0.4%, to close at 34,721.12.

The S&P 500 slipped 11.93 points, or 0.3%, to finish at 4,488.28.

The NASDAQ Composite shed 186.30 points, or 1.3%, to end at 13,711.

For the week, the Dow declined 0.3%, the S&P 500 fell 1.3% and the NASDAQ dropped 3.9%. The S&P 500 and NASDAQ each snapped a three-week winning streak while the Dow fell for a second week in a row, according to Dow Jones Market Data.

Hospitals, a local family practice office, a pharmaceutical company, all likely have one thing in common. Somewhere within these companies or partnerships, there are key employees or profit makers. Due to their expertise, management skills, knowledge, or “history of why,” they have become indispensable to their employers.

If this key employee were to die prematurely, what would potentially happen to the company? In many cases, especially in smaller companies, it would have a devastating effect on the bottom line, or even precipitate a bankruptcy. In these circumstances, a form of business insurance, called key person coverage, is recommended in order to alleviate the potential financial problems resulting from the death of that employee.

The business would purchase and own a life insurance policy on the key person. Upon the death of the employee, the life insurance proceeds could be used to:

Pay off bank loans.

Replace the lost profits of the company.

Establish a reserve for the search, hiring and training of a replacement.

[B] Business Continuation Funding

See the chapters on buy-sell agreements and asset protection planning.

[C] Executive Bonus Plan

An executive bonus plan (or § 162 plan) is an effective way for a company to provide valued, select employees an additional employment benefit. One of the main advantages to an executive bonus plan, when compared to other benefits, is its simplicity. In a typical executive bonus plan, an agreement is made between the employer and employee, whereby the employer agrees to pay for the cost of a life insurance policy, in the form of a bonus, on the life of the employee.

The major benefits of such a plan to the employee are that he or she is the immediate owner of the cash values and the death benefit provided. The only cost to the employee is the payment of income tax on any bonus received. The employer receives a tax deduction for providing the benefit, improves the morale of its selected employees, and can use the plan as a tool to attract additional talent.

[D] Non-Qualified Salary Continuation

Commonly referred to as deferred compensation, this is a legally binding promise by an employer to pay a salary continuation benefit at a specific point in the future, in exchange for the current and continued performance of its employee. These plans are normally used to supplement existing retirement plans.

Although there are different variations of deferred compensation, in a typical deferred compensation agreement, the employer will purchase and own a life insurance policy on the life of the employee. The cash value of the policy grows tax deferred during the employee’s working years. After retirement, these cash values can be withdrawn from the policy to reimburse the company for its after-tax retirement payments to the employee.

Upon the death of the employee, any remaining death benefit would likely be received income tax free by the employer (Alternative Minimum Taxes could apply to any benefit received by certain larger C corporations). The death benefit could then be used to pay any required survivor benefits to the employee’s spouse, or provide partial or total cost recovery to the employer.

In a typical plan, the terms of the agreement are negotiated as to the amount of benefit received by the employee, when retirement benefits can begin, how long retirement benefits will be paid, and if benefits will be provided for death or disability. The business has established what is commonly referred to as “golden handcuffs” for the employee. As a result, the benefit will only be received if the employee continues to work for the company until retirement. If the employee is terminated or quits prior to retirement, the plan would end and no benefits would be payed.

[E] Split Dollar Plans

Split dollar arrangements can be a complicated and confusing concept for even the most experienced insurance professional or financial advisor. This concept is, in its simplest terms, a way for a business to share the cost and benefit of a life insurance policy with a valued employee. In a normal split dollar arrangement, the employee will receive valuable life insurance coverage at little cost to them. The business pays the majority of the premium, but is usually able to recover the entire cost of providing this benefit at termination of employment, death or surrender of the policy.

Following the publication of IRS Notices 2002-8 and 2002-59, there are currently two general approaches to the ownership of business split-dollar life insurance: Employer-owned or Employee-owned.

***

[1] Employer-Owned Method

In the employer-owned method the employer is the sole owner of the policy. A written split-dollar agreement usually permits the employee to name the beneficiary for most of the death proceeds. The employer owns all the cash value and has the unfettered right to borrow or withdraw it as necessary. At the end of the formal agreement, the business can generally (1) continue the policy as key person insurance, (2) transfer ownership to the insured and report the cash values as additional income to the insured, (3) sell the policy to the insured, or (4) use a combination of these methods. This is commonly referred to as “rollout.”

Practitioners should be careful not to include rollout language in the split-dollar agreement. The reason the rollout should not be included is that if the parties formally agree that after a specified number of years—or following a specific event—related only to the circumstances surrounding the policy, that the policy will be turned over to the insured, the IRS could declare that the entire transaction was a sham and that its sole purpose was to avoid taxation of the premiums to the employee, generating substantial interest and penalties in addition to the additional taxes due.

The death proceeds available to the insured employee’s beneficiary is considered a current and reportable economic benefit (REB), and it is an annually taxable event to the employee. If an individual policy is involved, the REB is calculated by multiplying the face amount times the government’s Table 2004 rates or the insurance company’s alternative term rates, using the insured’s age. If a second-to-die policy is involved, the government’s PS38 rates or the company’s alternative PS38 rates will be used. Any part of the premium actually paid by the employee is used to offset any REB dollar-for-dollar.

[2] Employee-Owned Method

With the employee-owned method, the insured-employee is generally the applicant and owner of the policy. Any premiums paid by the business are deemed to be loans to the employee and the employee reports as income an imputed interest rate on the cumulative amount of loan based on Code § 7872. A collateral assignment is made for the benefit of the business to cover the cumulative loan amount. In some cases, the assignment may allow the assignee to have access to the cash values of the policy by way of a policy loan. This method is unavailable for officers and executives of publicly- held corporations because of the current restrictions on corporate loans (the Sarbanes-Oxley Act of 2002).

The employee-owned method is somewhat similar to the older collateral assignment form of split-dollar. The benefits for the employee are both the ability to control large amounts of death proceeds as well as developing equity in the policy. Whether or not this new method catches on will depend greatly on the imputed interest rate published by the IRS every July. If set low enough, this may be an excellent opportunity for the employee to use inexpensive business dollars to pay for life insurance.

Posted on April 10, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

SPUR INNOVATION

The Dallas Morning News Reported that Healthcare Costs Per Capita in the Dallas-Fort Worth Metro Area are Higher than New York City, Houston, Miami, Chicago, Atlanta and Washington, D.C.