BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on December 26, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The Icarus Paradox suggests that some businesses bring about their own downfall through their own successes.

The Icarus paradox was coined by Dan Miller in his 1990 book by the same name. The term refers to the phenomenon of businesses failing abruptly after a period of apparent success, where this failure is brought about by the very elements that led to their initial success.

It alludes to Icarus of Greek mythology, who drowned after flying too close to the Sun. The failure of the very wings that allowed him to escape imprisonment and soar through the skies was what ultimately led to his demise, hence the paradox.

Earnings per share (EPS): The portion of a company’s profits allocated to each outstanding share of its common stock. It is as an indicator of a company’s profitability.

Earnings yield: Earnings per share for the most recent 12 months, divided by the current market price per share; it is the inverse of the price to earnings (P/E) ratio.

EBITDA: Earnings before interest, taxes, depreciation and amortization (EBITDA) is an approximate measure of a company’s operating cash flow.

Posted on December 26, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITION

By Staff Reporters

***

***

Bernard Mandeville’s Paradox represent actions that may be vicious to individuals may also benefit society as a whole.

Mandeville’s Paradox challenges traditional moral and economic assumptions about selfishness and virtue. It suggests that economic systems can thrive on individual self-interest, a concept that has influenced modern economic thought, particularly in the development of free-market ideologies.

Understanding this paradox is crucial for economists, policymakers, and philosophers as it complicates the evaluation of behaviors and policies based solely on their perceived moral qualities. It invites a complex analysis of how individual actions, regardless of their intentions, contribute to the broader welfare of society.

Posted on December 26, 2024 by Dr. David Edward Marcinko MBA MEd CMP™

DEFINITION

By Staff Reporters

***

***

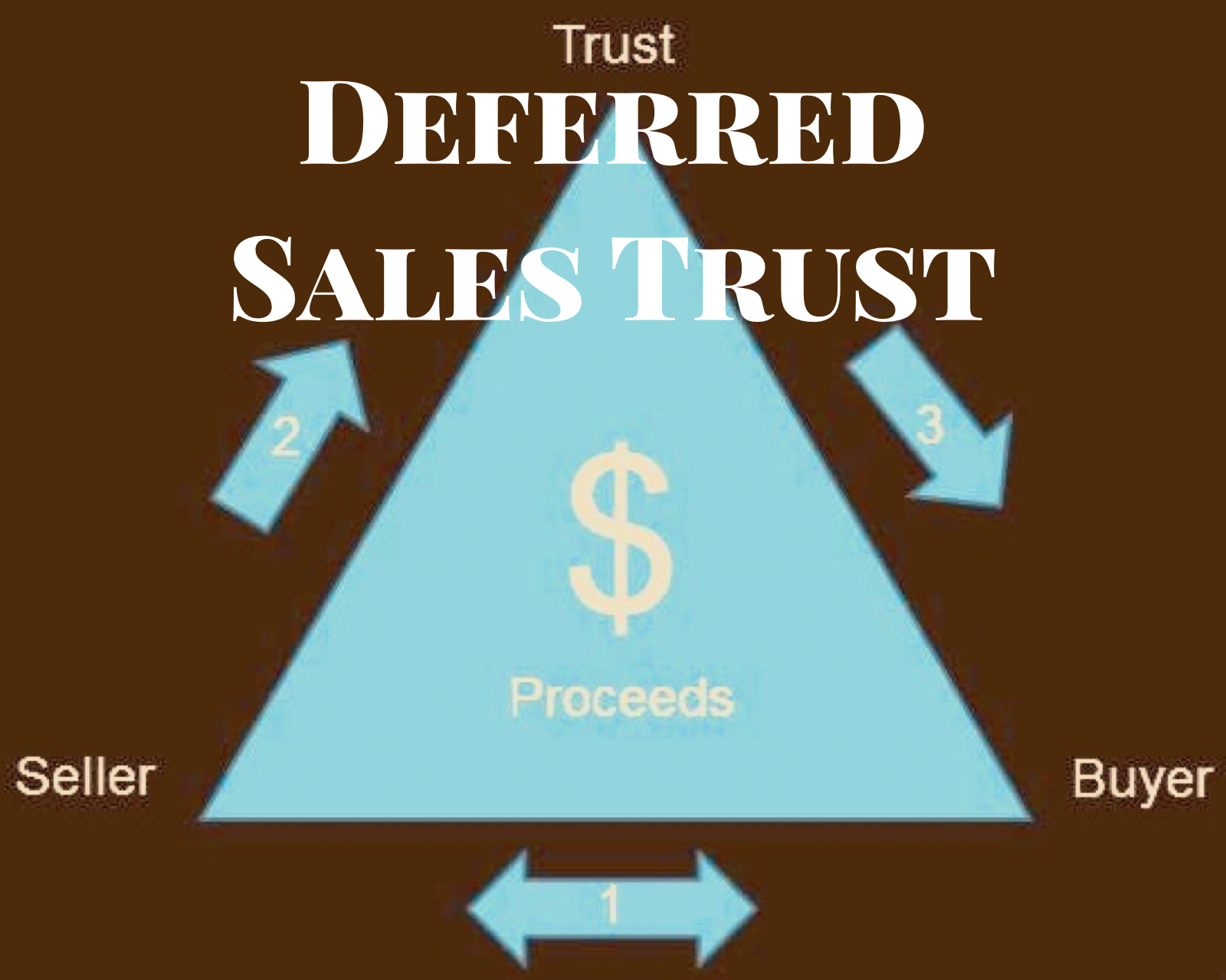

A deferred sales trust (DST) is an advanced tax strategy that allows investors to delay capital gains taxes on the sale of assets that have significantly risen in value, such as real estate or businesses. By selling the asset to a trust, the seller can receive payments over time, spreading out tax liabilities and allowing the profits to grow tax-deferred.

For example, a business owner may sell their company to a DST, avoiding a large tax bill upfront and instead receive income over multiple years. However, DSTs can be complex, and there are often fees involved in setting up and maintaining the trust.

Now, let’s point out some of the pros and cons of Deferred Sales Trusts.

One potential positive feature of using an installment sale to defer your capital gains taxes rather than a 1031 exchange is that installment sales don’t come with the same strict guidelines that govern 1031 exchanges. In particular, in light of the Tax Cuts and Jobs Act of 2017, 1031 exchanges are restricted to real property, whereas Deferred Sales Trusts and other installment sale arrangements can be used to defer capital gains for any kind of asset.

Conversely, the IRS has provided little to no guidance on how to defer taxes using an installment sale.

The basic rationale behind why you don’t receive capital gain is that you are not profiting immediately from the sale made with a Deferred Sales Trust. Given this rationale, there are various constraints on how a Deferred Sales Trust must be organized so that no capital gains taxes are in fact realized.

The third party to whom you transfer your asset generally cannot be a “related person” to you, such as a family member or a corporation in which you hold an interest. Except in special circumstances, if you attempt to set up a Deferred Sales Trust with a related person it will be viewed as a “sham trust” made just for the purposes of avoiding capital gains taxes, and will not be protected by the provisions in Section 453.

As with the 1031 exchange, you, the seller, cannot at any point in the transfer of your asset be in constructive receipt of the proceeds from the third party’s sale of that asset. To successfully defer capital gains taxes, either the third party or the trust of which they are trustee must be the only party which receives cash in the sale of the transferred asset. This includes receipt of a bond which is payable on demand.

This has been a general, informal introduction to Deferred Sales Trusts. As always, before attempting to carry out any important financial decision, investors should consult with a qualified tax or legal advisor regarding the specifics of their situation.