Sad – But True

***

Share this:

Filed under: LifeStyle | Tagged: doctor jokes | Leave a comment »

ME-P SYNDICATIONS:

WSJ.com,

CNN.com,

Forbes.com,

WashingtonPost.com,

BusinessWeek.com,

USNews.com, Reuters.com,

TimeWarnerCable.com,

e-How.com,

News Alloy.com,

and Congress.org

![]()

![]()

BOARD CERTIFICATION EXAM STUDY GUIDES

Lower Extremity Trauma

[Click on Image to Enlarge]

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] E-mail: MarcinkoAdvisors1738@outlook.com

![]()

ePodiatryConsentForms.com

ePodiatryConsentForms.com

“Providing Management, Financial and Business Solutions for Modernity”

“Providing Management, Financial and Business Solutions for Modernity”

Bill of the Month Club

[By staff reporters]

Journalists from Kaiser Health News and NPR will be looking at surprising medical bills and figuring out what they can tell us about the health care system. You can share your story here.

***

LINK:

https://www.npr.org/series/651784144/bill-of-the-month

Assessment: Your thoughts are appreciated.

BUSINESS, FINANCE, INVESTING AND INSURANCE TEXTS FOR DOCTORS:

THANK YOU

![]()

***

Filed under: Health Economics, Health Insurance | Tagged: balance-billing, medical bills | Leave a comment »

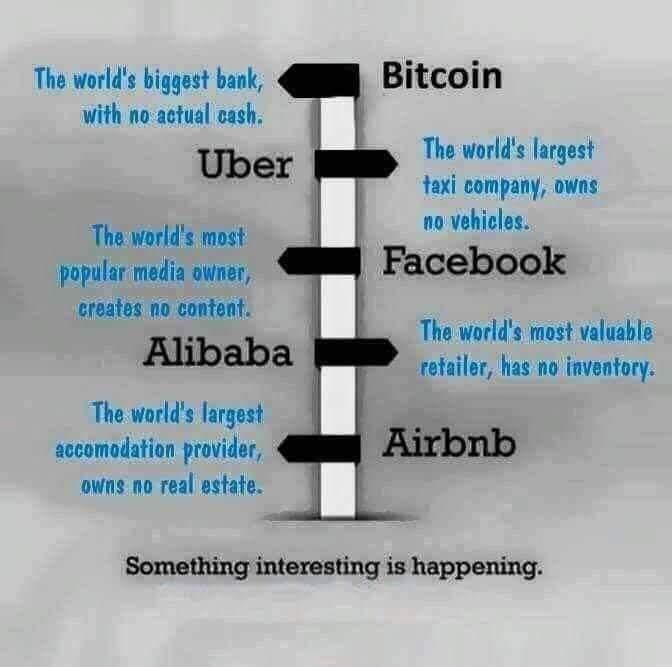

The “Have and Have Nots”

[By staff reporters]

***

***

8

8

***

Filed under: Retirement and Benefits | Tagged: Retirement Gaps | 1 Comment »

Responding to an ‘Objectivist’s’ Claim That Self-Ownership Doesn’t Exist

By Dr. David E. Marcink MBA

I was fascinated with this podcast.

It was recorded by my neighbor and Austrian economist Peter Raymond over at “The Free Man Beyond the Wall” website.

PODCAST: http://freemanbeyondthewall.libsyn.com/episode-335

Your thoughts are appreciated.

BUSINESS, FINANCE, INVESTING AND INSURANCE TEXTS FOR DOCTORS:

***

![]()

![]()

THANK YOU

Filed under: Experts Invited, Practice Management, Videos | Tagged: Peter Raymond, Self-Ownership Doesn't Exist?, The Free Man Beyond the Wall | Leave a comment »

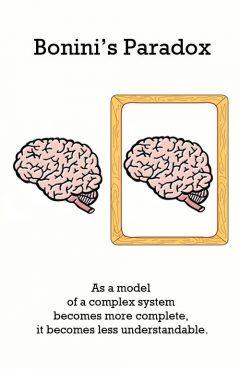

What it is – How it works!

[By staff reporters]

Bonini’s paradox, named after Stanford business professor Charles Bonini, explains the difficulty in constructing models or simulations that fully capture the workings of complex systems (such as the human brain

***

***

MORE: https://en.wikipedia.org/wiki/Bonini%27s_paradox

Your thoughts are appreciated.

BUSINESS, FINANCE, INVESTING AND INSURANCE TEXTS FOR DOCTORS:

***

![]()

![]()

THANK YOU

Filed under: Career Development, Glossary Terms | Tagged: Bonini's paradox | Leave a comment »

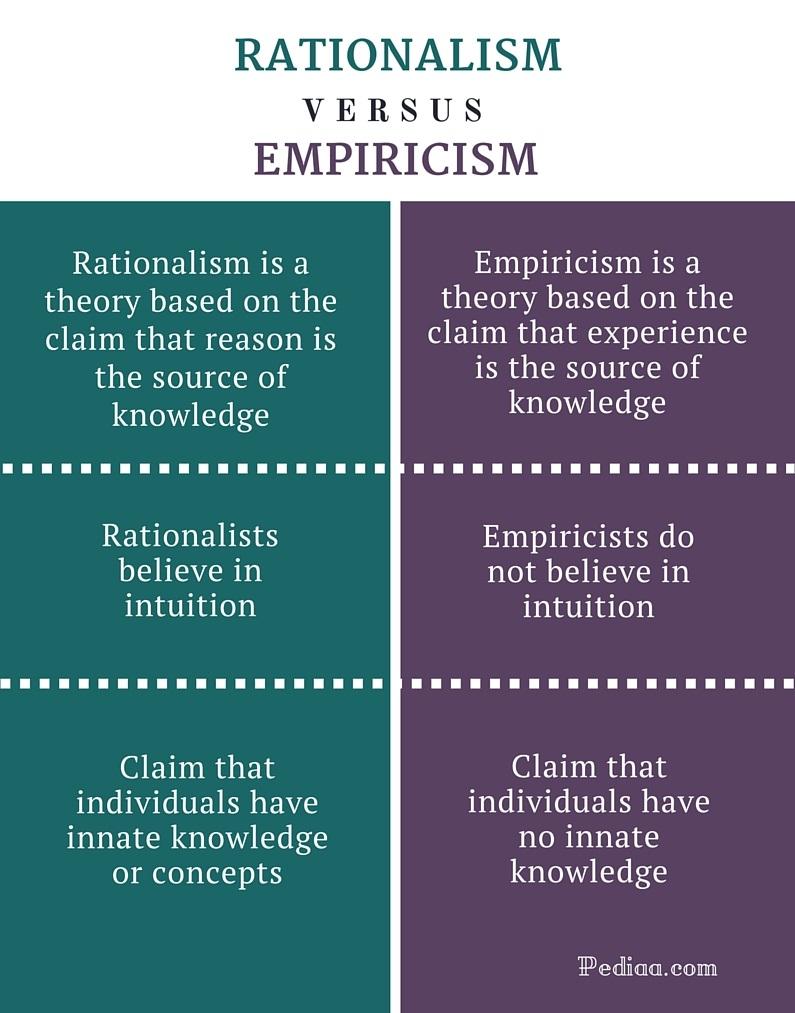

PHILOSOPHY – What is Knowledge?

***

***

***

MORE: https://medicalexecutivepost.com/2019/05/14/what-is-epistemic-ambivalence/

![]()

![]()

***

Filed under: iMBA, Inc., LifeStyle | Tagged: Empiricism, epistemology, Rationalism | Leave a comment »

REST-IN-PEACE

By Dr. David E. Marcinko MBA

Courtesy: www.CertifiedMedicalPlanner.org

The European refugee turned Wall Street legend, died at 91 lat week. Rohatyn pioneered the M&A advisory business in the 1960s. Working with companies like GE, Revlon, and AT&T, he earned the nickname “Felix the Fixer” for brokering some of the deals that created today’s corporate landscape.

With deep thoughts like that, Rohatyn was tapped to help NYC stave off bankruptcy in 1975, when lenders cut off the city from additional short-term credit.

You might not realize it from walking around Manhattan today, but 1970s-era New York was in a deep financial manhole. It had an annual deficit of $1.5 billion a year on a budget of roughly $12 billion.

In his later years, Rohatyn became the U.S. ambassador to France, an author, and a finance sage.

Assessment: I followed his career and studied his methods while in B-school, back in the day.

Your thoughts are appreciated.

BUSINESS, FINANCE, INVESTING & INSURANCE TEXTS FOR DOCTORS:

THANK YOU

8

***

Filed under: Investing | Tagged: Felix Rohatyn | Leave a comment »

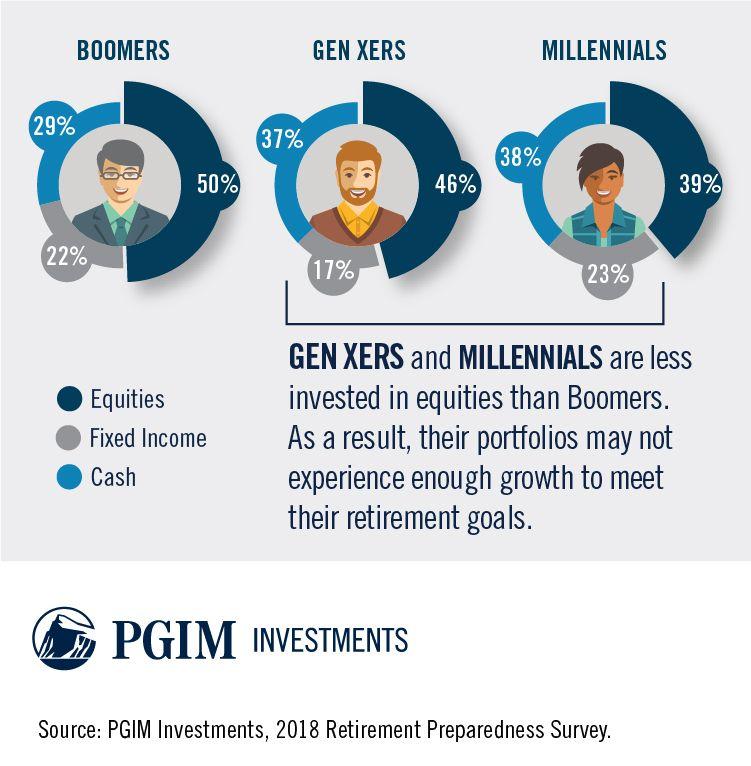

Portfolio Asset Allocations

By PGIM Investments

***

***

Assessment: Your thoughts are appreciated.

BUSINESS, FINANCE, INVESTING & INSURANCE TEXTS FOR DOCTORS:

***

8

THANK YOU

Filed under: iMBA, Inc. | Tagged: baby boomers, Gen X, Millennials | Leave a comment »

Do your credit card reward points belong to you?

By Rick Kahler CFP®

By Rick Kahler CFP®

For frequent travelers, who often choose credit cards based on reward programs, accumulated points can be worth thousands of dollars. Whether points are an asset that can be transferred to an heir is another matter.

I recently received this question: “Our friend whose husband recently passed away lost over a million points with Capital One because her husband was the primary on the account and she was just an authorized user, not a joint owner. Capital One closed the credit card since he passed and all the points were forfeited. Do you have any ideas on how to get the points back?”

Unfortunately, not much can be done after the fact. Most credit cards offering points that can be redeemed for travel expense say that points have no cash value and are not actually the property of the account owner but rather belong to the reward’s program. Most card programs’ terms and conditions say that points outstanding upon the card holder’s death are permanently forfeited.

An appeal to the issuing bank would be worth trying. Surprisingly, some will show compassion and allow the points to transfer to another account or credit their value against any outstanding balances on the card, usually at one cent per point.

Considering this issue ahead of time, however, might allow surviving spouses to avoid losing all of a loved one’s hard-earned points.

First, try to find a rewards card that will allow you to own the account jointly with your spouse rather than being an authorized user. If one spouse passes away, the points will remain in the account and the other joint owner will have full access to them. An authorized user has no risk or obligation to pay any debt, and therefore has no claim on any points that remain in the account after the death of the primary cardholder.

The downside of a joint account is that each cardholder is equally liable for any amounts the other charges to the account. If your marriage is transparent and without any financial infidelity going on, this shouldn’t be a problem. If the card is a business card, joint ownership could be more problematic.

Banks that I found that will allow joint accounts are US Bank and PNC Bank. Specific rewards cards that allow joint ownership are Bank of America Cash Rewards, Wells Fargo Cash Wise Visa, and Discover it Cash Back. Obviously, with only three rewards cards allowing joint ownership, that option isn’t widely available.

The next best choice is to be sure both partners have the login information for the account. This would allow a survivor to log on and redeem or transfer points. Many cards will allow transferring points to an airline or hotel rewards programs for 1.5 to 2.3 cents per point. Of course, both partners need to have access to those accounts as well, which generally isn’t a problem with most programs.

This is also the recommended method of accessing points with a specific airline. According to a September 19, 2019, article by Richard Kerr at thepointsguy.com, giving your next of kin access to all your airline and hotel awards accounts gives them “all the information needed to continue using the points and miles without alerting the airline.”

Including airline reward points in a will may be worthwhile. It might not make a difference with every airline or bank, but some programs will transfer such designated points without a fee.

Assessment:

Travel reward points may be a relatively minor asset. Still, a little planning can make them readily available without adding stress for a surviving spouse during a difficult time.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Link: http://feeds.feedburner.com/HealthcareFinancialsthePostForcxos

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

***

8

Filed under: Experts Invited, Investing | Tagged: credit cards, reward points, Rick Kahler CFP | Leave a comment »

Of Executives

***

***

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Link: http://feeds.feedburner.com/HealthcareFinancialsthePostForcxos

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

***

![]()

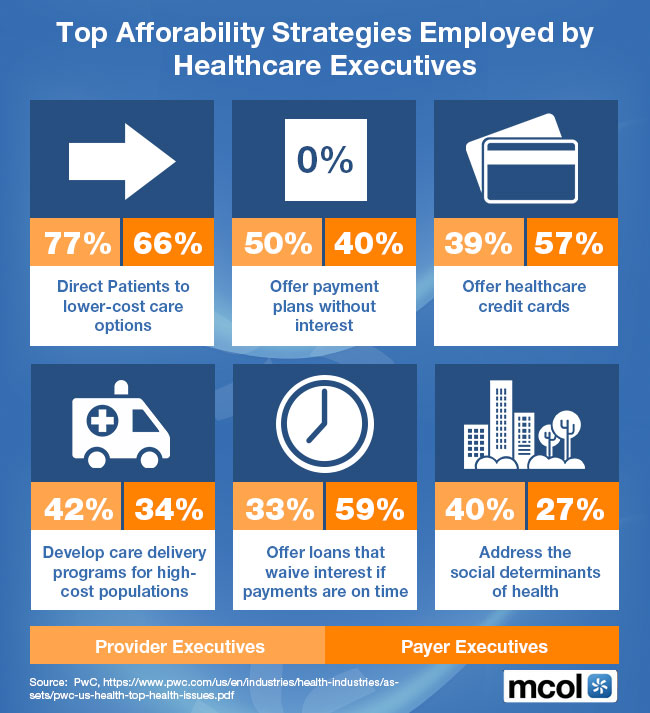

Filed under: Health Economics, Health Insurance | Tagged: Healthcare Affordability Strategies | Leave a comment »

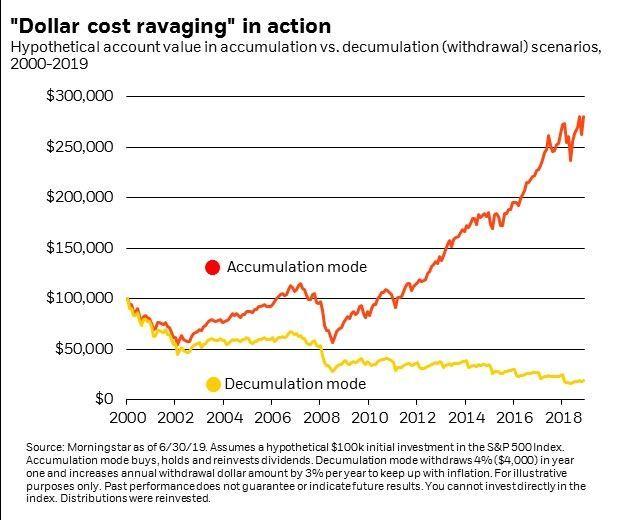

RETHINKING: Dollar Cost Averaging (DCA)?

By Dr. David E. Marcinko MBA

Dollar cost averaging (DCA) is an investment strategy with the goal of reducing the impact of volatility on large purchases of financial assets such as equities.

Dollar cost averaging is also called the constant dollar plan (in the US), pound-cost averaging (in the UK), and, irrespective of currency, as unit cost averaging or the cost average effect.

***

***

Assessment: Might DCA also be called Dollar Cost Ravaging?

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Link: http://feeds.feedburner.com/HealthcareFinancialsthePostForcxos

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

8

Filed under: Investing | Tagged: DCA, dollar cost averaging, Dollar Cost Ravaging | 1 Comment »

An Important Money Skill

By Rick Kahler CFP

“Some days adulting is a pain.” What parent of college-age children hasn’t heard something similar from their kids? The transition from kid to adult is a necessary process toward living a fulfilled and meaningful life, but it isn’t easy or smooth.

This is especially true when it comes to money. Mastering money skills can be a challenge even for older adults.

One of the earliest opportunities to learn adult financial skills comes with renting an apartment. Before you sign that first lease—or any lease—it’s important to understand it. A lease is a legal document that sets out obligations and rights for both landlord and tenant.

One of the most important features of a lease is the length of the agreement. Your lease could be “month-to-month” or for a specific period like a few months or even several years. The most common residential lease terms are six months to one year.

There are pluses and minuses to both types. A month-to-month lease gives the renter the minimum commitment and maximum flexibility. Usually, if you want to move out for whatever reason, you just need to give the landlord a 30-day notice. Unlike a longer-term lease, there is no penalty for “breaking” the lease unless you fail to give even a 30-day notice.

So why wouldn’t a tenant always want a month-to-month lease? Many tenants don’t understand that the flexibility goes both ways. If a landlord chooses to stop leasing the property, finds a tenant willing to pay higher rent, or decides to sell the property, all the lease requires is a 30-day notice for the current tenant to move out. A tenant must accept that risk.

A recent local example concerned 11 house renters who lived on the campus of the Star Academy, a former state-owned property near Custer, SD. Some of the tenants had rented for 14 years with month-to-month leases. When the state foreclosed on the property it gave the tenants 30-day notices to move. This was not received well by the renters, who faced the prospect of immediately having to find new places to live in a town with a limited supply of housing. Fortunately, the governor reversed the decision and gave the renters six months to find new housing.

As shocking and heartless as this move might have seemed to the renters, it was completely within the rights of the landlord, just as it would have been completely within the rights of any of the tenants to do the same.

It’s easy to get lulled to sleep by a month-to-month lease, especially when a tenant has lived in the property for year after year. However, if the prospect of having to vacate your home in 30 days is not appealing, it would be a really good idea to ask the landlord for a longer lease.

Assessment:

Before signing a lease, consider how long you are willing to commit to living in the property. What will best serve your situation? For some, it may be a lease that expires at the end of a school year, or in a year, or even in three to five years if you see no reason that you will need to move anytime soon. Be aware that by signing the lease, you agree to stay and to pay rent until the time is up.

Also understand that, unless the lease specifically states otherwise, neither you nor the landlord are bound to renew when the lease expires. So it’s important to renegotiate a new lease well before the current lease expires.

Before signing any lease, read it carefully. Ask clarifying questions. Be sure you understand the legal commitment you are making.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Link: http://feeds.feedburner.com/HealthcareFinancialsthePostForcxos

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

8

***

Filed under: Experts Invited, Financial Planning, LifeStyle | Tagged: apartment leases, leasing | Leave a comment »

FROM: The Ludwig Von Mises Institute

By Dr. David E. Marcinko MBA

Courtesy: www.CertifiedMedicalPlanner.org

I was fascinated with this podcast as a rewind episode. Pete talks about a host of Liberty related topics with Ludwig Von Mises Institute President, Jeff Deist.

It was recorded by my neighbor and Austrian economist Peter Raymond over at “The Free Man Beyond the Wall” website.

PODCAST: http://freemanbeyondthewall.libsyn.com/episode-344

Your thoughts are appreciated.

BUSINESS, FINANCE, INVESTING AND INSURANCE TEXTS FOR DOCTORS:

***

![]()

![]()

THANK YOU

Filed under: Experts Invited, Videos | Tagged: Jeff Deist, Ludwig Von Mises Institute, Peter Raymond, The Free Man Beyond the Wall | Leave a comment »

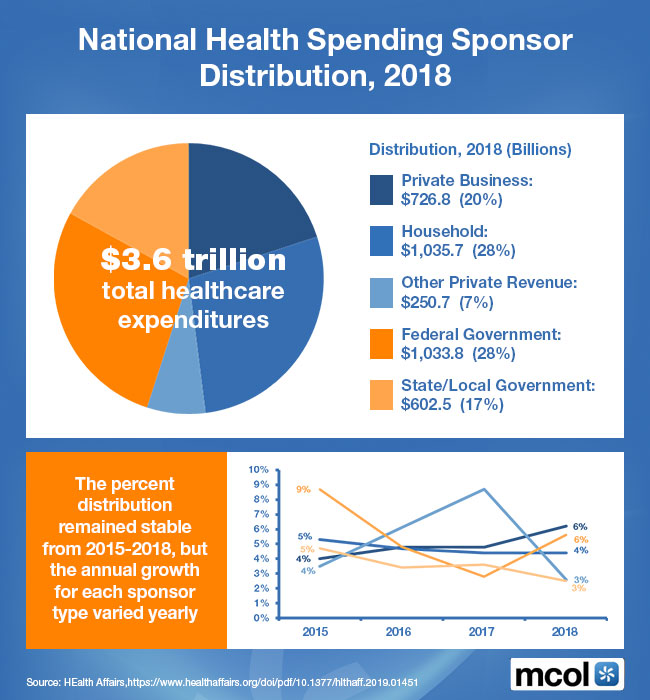

Sponsor Distribution for 2018

***

***

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Link: http://feeds.feedburner.com/HealthcareFinancialsthePostForcxos

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

![]()

***

Filed under: Health Economics, Health Insurance, iMBA, Inc. | Tagged: National Health Care Spending, www.MCOL.com | Leave a comment »

http://www.ePodiatryConsentForms.com

http://www.ePodiatryConsentForms.comBy Dr. David Edward Marcinko MBBS DPM FACFAS MBA MEd

CUSTOMIZABLE CMS & AGENCY FOR HEALTHCARE RESEARCH AND QUALITY STYLED PROTOCOLS, CHECKLISTS AND TEMPLATES

… Specifically for Podiatrists …

e-Podiatry Consent Forms™ is an innovative new suite of software programs from the Institute of Medical Business Advisors [iMBA, Inc]. Our products solve your informed consent problems and enhance the education, discussion and documentation of the informed consent process for all podiatrists performing foot, ankle and leg reconstructive surgical procedures.

THE PROBLEM

All podiatrists are being pressured by the Centers for Medicare and Medicaid Services [CMS], the Joint Commission on Accreditation of Healthcare Organizations [JCAHO], liability carriers and private insurance payers to make their consent process more patient-friendly, informed and easily understood. And, the pressure to standardize and comply is great.

Most recently, based on the need to make healthcare even safer, the Agency for Healthcare Research and Quality (AHRQ) undertook a major study to identify patient safety issues and develop recommendations for “best practices”.

The AHRQ Evidence Report

The AHRQ report identified the challenge of addressing shortcomings such as missed, incomplete or not fully comprehended informed consent, as a significant patient safety issue and opportunity for improvement.

The authors of the AHRQ report hypothesized that better informed patients:

“are less likely to experience errors by acting as another layer of protection.”

And, the AHRQ study ranked a “more interactive informed consent process” among the top 11 practices supporting more widespread implementation; especially for surgical consent forms.

THE SOLUTION

Why Us: https://epodiatryconsentforms.com/why-us/

One answer to the modern risk-management problem of “informed consent interactivity” may be e-Podiatry Consent Forms™ We license two core interactive surgical products, and a reference library, with related concepts and products in development:

Each e-Podiatry Consent Forms™ CD-ROM [secure email delivery is now available] is increasingly trusted as the simple solution to standardized communications across the entire office-enterprise; from managing-risk, informing-patients and complying with modern regulatory requirements through enhanced patient-centric informed consent encounters.

Thus, by improving the consistency, details, documentation and effectiveness of the informed consent process, e-Podiatry Consent Forms™ equips all podiatric surgeons with the tools needed to augment quality standards, reduce litigation potential and improve patient outcomes and safety.

http://www.ePodiatryConsentForms.com

***

***

Filed under: "Doctors Only", Practice Management | Tagged: doctor podiatric medicine, DPM, e-Podiatry Consent Forms™, foot surgery, foot surgery consent forms, podiatrists, Podiatry Consent Forms | Leave a comment »

Supply Chain Service Management?

[By staff reporters]

***

***

8

Filed under: Investing | Tagged: Asset Lite Companies | Leave a comment »

Medicare Part C

***

***

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Link: http://feeds.feedburner.com/HealthcareFinancialsthePostForcxos

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

***

Filed under: iMBA, Inc. | 3 Comments »

Where Will Your Money Come From?

By Rick Kahler CFP®

The list is fairly short: Social Security, a pension, working, your assets, children, or public assistance.

According to an April 22, 2019 Bloomberg article by Suzanne Woolley, entitled “America’s Elderly Are Twice as Likely to Work Now Than in 1985“, only twenty percent of those age 65 or older are working. The rest either can’t work physically, can’t find work, or don’t want to work. According to the ADA National Network, over 30 percent of people over 65 are disabled in some manner.

According to the Center on Budget and Policy Priorities, Social Security provides the majority of income for most elderly Americans. It provides at least 50% of income for about half of seniors and at least 90% of income for about one-fourth of seniors. The average Social Security retirement benefit isn’t as high as many people think. In June 2019 it was about $1,470 a month, or about $17,640 a year.

And, as per the Pension Rights Center, around 35% of Americans receive a pension or VA benefits. The greatest percentage of pensions are government. This would include retired state and federal workers like teachers, police, firefighters, military, and civil service workers. In 2017 the median state or local government pension benefit was $17,894 a year, the median federal pension was $28,868, and the median military pension was $21,441.

Working provides the highest source of retirement income for the 20 percent of those who are over 65 and are still working. According to SmartAsset.com, Americans aged 65 and older earn an average of $48,685 per year. However, in a NewRetirement.com article dated February 26, 2019, “Average Retirement Income 2019, How Do You Compare“, Kathleen Coxwell cites a figure from AARP that the median retirement income earned from employment is $25,000 a year.

About 3% of retirees receive public assistance.

This leaves around 20% of those over 65 who depend partially or fully for their retirement income on money they set aside during their working years. According to TheStreet.com, “What Is the Average Retirement Savings in 2019“, by Eric Reed, updated on Mar 3, 2019, the average retirement account for those age 65 to 74 totals $358,000. That amount will safely provide around $15,000 a year for most retirees’ lifetime. The median savings is $120,000, which will produce only about $5,000 a year. In order to retire at age 65 with an annual investment income of $30,000 to $40,000, someone would need a retirement nest egg of over $1 million.

***

***

My conclusion from this data is that most Americans are woefully underprepared to live a comfortable lifestyle when they can no longer work. Between Social Security, pensions, and retirement savings, a retiree can expect a median income of $18,000 to a maximum of $52,000 a year. According to data I compiled from NewRetirement.com, the average median retirement income of those over age 65 is around $40,000.

What are some things you can do to increase your chances of enjoying a comfortable retirement income?

If you are under age 50, begin setting aside 15% to 25% of your income for retirement.

If you are over 60, keep working as long as you can. If you retire early, your monthly Social Security benefit is lower for the rest of your life.

Consider ways to stretch your retirement income by downsizing, sharing housing, or relocating to an area of the US or even outside the country with a lower cost of living.

Research what you can reasonably expect from Social Security and other sources of retirement income. Base your retirement expectations on informed planning, not on vaguely optimistic expectations.

Assessment: Your thoughts are appreciated.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Link: http://feeds.feedburner.com/HealthcareFinancialsthePostForcxos

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

***

8

8

***

Filed under: iMBA, Inc., Retirement and Benefits | Tagged: retirement, retirement planning, Rick Kahler CFP | Leave a comment »

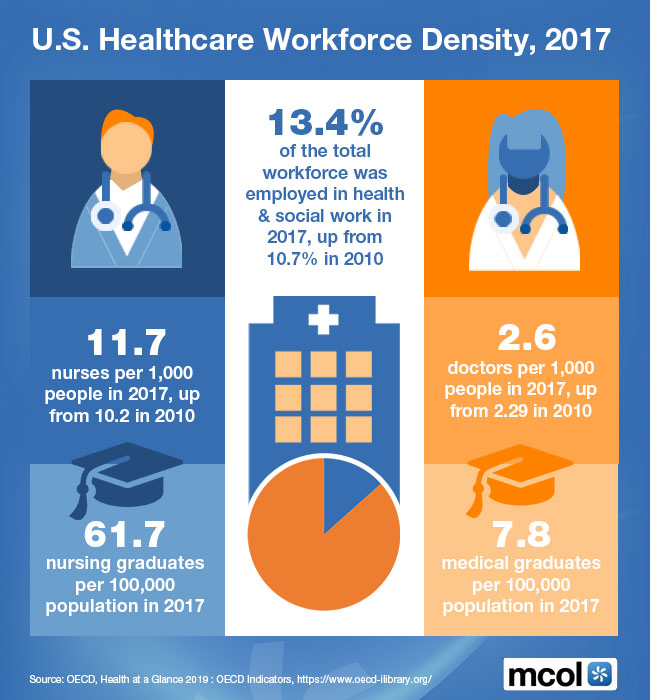

Circa 2017

***

***

Assessment: Your thoughts are appreciated.

BUSINESS, FINANCE, INVESTING AND INSURANCE TEXTS FOR DOCTORS:

THANK YOU

Filed under: Practice Management | Tagged: U.S Healthcare Workforce Density | Leave a comment »

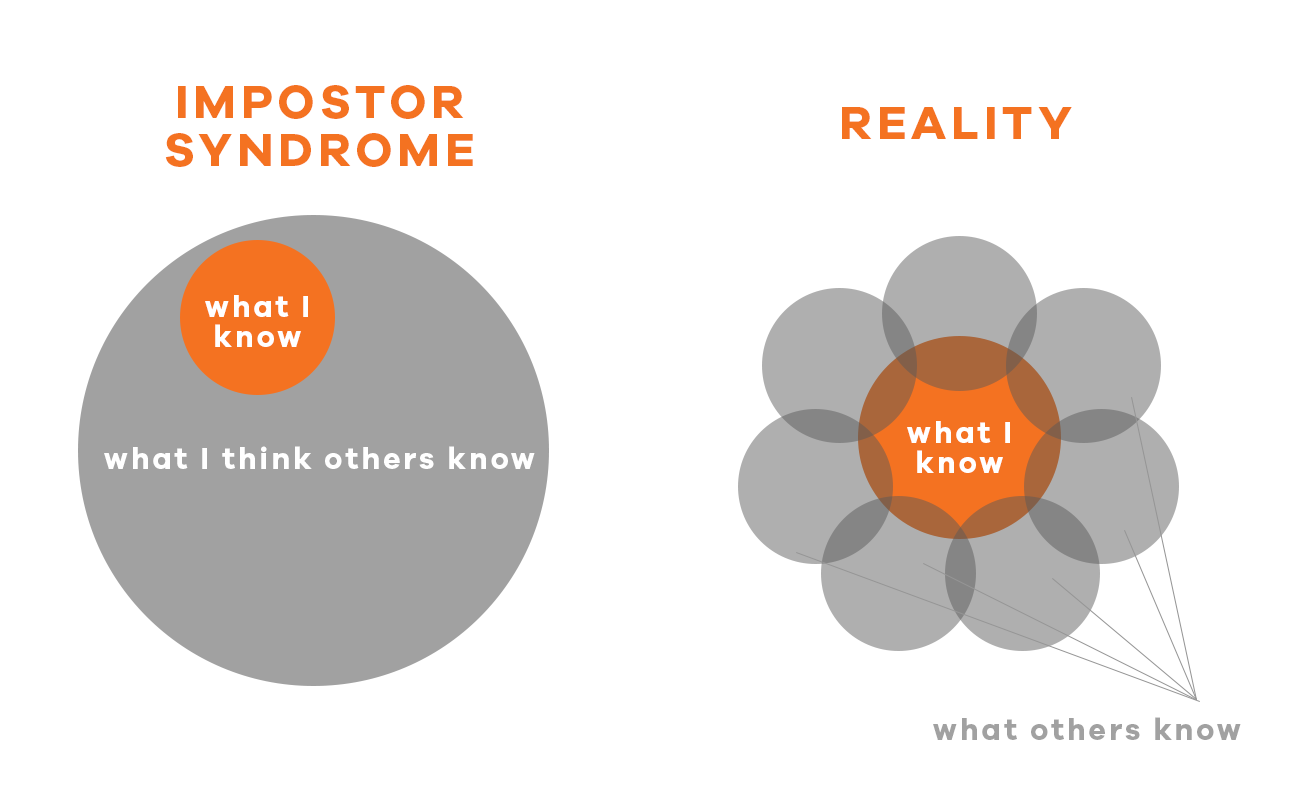

What is Imposter Syndrome and how can you beat it?

Courtesy: www.CertifiedMedicalPlanner.org

Imposter Syndrome is a psychological phenomenon whereby a person has serious doubts about their accomplishments. It’s an inability to believe that what you have achieved is due to you and not some form of “luck” or misunderstanding. If you have Imposter Syndrome, you may feel that your success is not truly “yours,” and you may dread being uncovered as the fraud you believe you are.

PODCAST: https://www.bing.com/videos/search?q=imoister+syndrome&&view=detail&list=Vr4FzCkwi0yHUg&FORM=VRPPLA

Assessment: Your thoughts are appreciated.

BUSINESS, FINANCE, INVESTING AND INSURANCE TEXTS FOR DOCTORS:

THANK YOU

Filed under: Health Insurance | Tagged: Imposter Syndrome | 1 Comment »

![]()

The Last Generation of Extreme Frugality … or Another Re-Start?

By Rick Kahler MS CFP® ChFC CCIM www.KahlerFinancial.com

“Be frugal.” “Save for the future.” “Live on less than you make.”

That’s my usual financial advice, and it’s well worth repeating even though most medical professionals aren’t following it.

[Very] occasionally however, I find it necessary to work with clients to overcome a different problem—underspending.

A Problem?

Huh? How can underspending possibly be a problem? Isn’t it a virtue to save and accumulate? Of course it is. Accumulating wealth typically requires people to live on much less than they earn. Being frugal is the common denominator of almost every first-generation wealth builder. But, don’t confuse living on less than you make with underspending.

To Every Season

Like almost everything, saving is but for a season. Once people retire and stop earning money from a medical practice, business or a job, a new era begins where it’s time to consume the fruits of their frugality. The problems start when the wise frugality of the earning years continues long past the time that it’s necessary. Frugality then can turn to under-consumption.

Be Thrifty – Not Frugal

What’s wrong with someone living on less than they could? Is it bad to continue to be thrifty? Of course not. The habit of frugality isn’t something people can turn off at a flip of a switch, and maybe that’s part of the problem. Wealth accumulators have lived with the money script of “Don’t consume your investments or savings” for so long, that when the time comes to begin living off of their investments it poses a significant challenge.

Extreme Frugality

The result can be under-spending is frugality taken to extremes. As I define underspending, it is spending significantly less than the amount you could conservatively spend annually and still have a 99% chance of never running out of money.

Under-spending is not the same as continuing to make frugal choices during retirement and economizing when possible. Typically, underspending results in people failing to get adequate medical care, eat a healthy diet, live in a well-maintained and comfortable home, or use help and support that would make life easier.

Example

Take Dr. Martin and his wife Eleanor, for example. They worked hard all their lives and managed to save $2,000,000. Today they are age 72. Based on a very conservative withdrawal rate of 3%, they could easily afford to take $60,000 from their portfolio each year. Instead, they withdraw $10,000. With the $30,000 they get from Social Security, they live on $40,000 a year.

What’s wrong with that?

What’s wrong is what they don’t spend money on. Both of them have neglected their health. They do get annual checkups from their family doctor, which are covered by Medicare. Yet, neither of them has seen a dentist for several years. Eleanor needs hearing aids but won’t get them because they “cost too much.” Even though Martin’s eyesight is beginning to fail and night driving is difficult, they insist on driving thousands of miles to visit their children because airline fares are “so outrageous.”

They sleep on a mattress that is 20 years old. Their house needs painted inside and out. Only two burners work on the kitchen stove, but they get by because it isn’t really a problem except at Thanksgiving when the family comes to visit.

The Cure

The cure to underspending is not running out and spending money frivolously or indulgently on things or experiences that don’t really add value to your life. Instead, it’s using what you have to make your life more comfortable and enjoyable.

Assessment

There is a season to plant for the future, with hard work, frugality, and saving. There is also a season of harvest. That’s the time to use what you have accumulated to support your health and well-being.

How many under-spending doctors are left? Do you know any? Is this the last generation of same? OR, the start of next gen 2.0 frugality.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Link: http://feeds.feedburner.com/HealthcareFinancialsthePostForcxos

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

***

8

***

Filed under: Research & Development, Retirement and Benefits | Tagged: extreme frugality, Rick Kahler CFP®, Under Spending Doctors | Leave a comment »

By Rick Kahler MSFS CFP

|

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Link: http://feeds.feedburner.com/HealthcareFinancialsthePostForcxos

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

Our Other Print Books and Related Information Sources:

***

| 8 |

Filed under: Health Economics, Health Insurance | Tagged: medicare, Rick Kahler CFP | Leave a comment »

Come to the Mütter Museum for World AIDS Day; December 1st 2019

***

I went to medical school in Philadelphia PA, and visited the Mutter Museum many times. If you’ve never been there – I urge you to check it out!

***

ESSAY: https://medicalexecutivepost.com/2019/11/19/national-hiv-testing-day/

Your thoughts are appreciated.

BUSINESS, FINANCE, INVESTING AND INSURANCE TEXTS FOR DOCTORS:

THANK YOU

Filed under: Research & Development | Tagged: AIDS, HIV, NATIONAL HIV TESTING WEEK 2019 | Leave a comment »