![]()

Remember the Ace Up Your Sleeve!

By Lon Jefferies MBA CFP® CMP®

After the historic growth the stock market has experienced since early 2009, many physician investors have felt that a healthy pullback may not be a completely negative thing.

After the historic growth the stock market has experienced since early 2009, many physician investors have felt that a healthy pullback may not be a completely negative thing.

After all, we certainly don’t want another bubble, or stock prices that are clearly out of line with the earning potential of the underlying companies.

Unfortunately, market corrections never feel healthy when they occur. Physicians, investors and almost all people get uncomfortable when the market declines, the media fans the flames by giving investors reason after reason to be afraid, and worries that this is the beginning of the next crash begin to develop.

While many investors admit that a 5% pullback is manageably unpleasant, concerns expand when the market decline hits 10% — right when the media can officially throw around the word “correction.”

Of course, we have no idea when the next drop will occur, but why not mentally prepare ourselves by exploring what has traditionally happened to stock prices once that 10% decline is crossed?

The Data

Ben Carlson, an institutional investment portfolio manager, looked at the S&P data going back to 1950, and found that there have been 28 instances when stocks fell by 10% or more. Thus, on average, the market has entered an official correction every 2.25 years. The last market correction occurred in 2011, so another 10% drop at this time would correlate pretty close to the average amount of time between corrections.

Obviously, the market has done pretty well since that last temporary correction in 2011. Clearly, such a drop is quite normal and far from historically concerning.

- S&P 500 Losses of 10% or More Since 1950

- Total Occurrences: 28 Times

- Average Loss: -21.6%

- Median Loss: -16.5%

- Average Length: 7.8 Months

- Greater Than 20% Loss: 9 Times

- Greater Than 30% Loss: 5 Times

Your Advantage

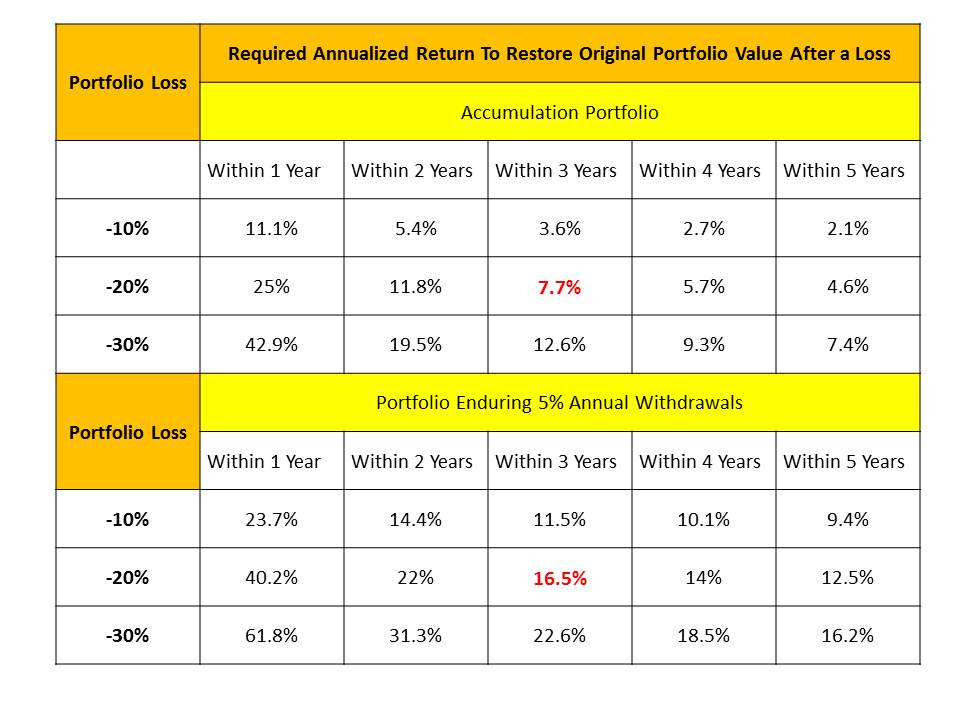

Are you thinking “I don’t think I can stomach that median loss of 16.5%?” Then it’s time to pull out the ace up your sleeve. Remember that the data above represents the historical performance of the S&P 500 – an index that is composed of 100% stocks. A capable financial planner would ensure you have an asset allocation mix between stocks, bonds, and cash that represents your tolerance for risk.

Consequently, your portfolio likely isn’t 100% stocks. In fact, the appropriate allocation for an average investor approaching or already enjoying retirement might be closer to only 50% stocks. This means that on average, your portfolio should decline only half as much as the S&P 500 during market downturns.

This ace may bring the loss endured by our sample investor with a 50% stock portfolio down to around 8.25% during the median decline. Are you now back in the “manageably unpleasant” range? If so, you likely have an appropriately constructed portfolio. If not, your risk tolerance may need to be reevaluated to ensure you are not exposing your nest egg to a larger loss than you can endure.

Avoid Harmful Reactions to the Market

Although the recent market pullback produces what seems like a foreign feeling, we’ve been here before. The S&P 500 declined in value by 18.64% over a 5 month period in 2011. However, an investor with a 50% stock portfolio likely only saw their account values drop around 9%-10% — still not fun, but manageable.

Assessment

Of course, we don’t know whether the market will continue to bounce back or again drop into official correction territory. If you continue to hear about the broad markets declining, remember that the average historical correction has been far from catastrophic, and that you have the ace of an appropriate asset allocation up your sleeve.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

- PRACTICES: www.BusinessofMedicalPractice.com

- HOSPITALS: http://www.crcpress.com/product/isbn/9781466558731

- CLINICS: http://www.crcpress.com/product/isbn/9781439879900

- ADVISORS: www.CertifiedMedicalPlanner.org

- FINANCE: Financial Planning for Physicians and Advisors

- INSURANCE: Risk Management and Insurance Strategies for Physicians and Advisors

- Dictionary of Health Economics and Finance

- Dictionary of Health Information Technology and Security

- Dictionary of Health Insurance and Managed Care

![]()

![]()

Share this:

Filed under: Investing | Tagged: Lon Jefferies MBA CFP®, S&P 500, Stock Market Correction | 1 Comment »