![]()

There is No Investing Crystal Ball

By Lon Jefferies, MBA CFP CMP™

By Lon Jefferies, MBA CFP CMP™

As the Dow has risen greatly since March 9, 2009, some physicians and investors worry that the market is overheated and due for a severe pullback; as recently experienced very minor events have illustrated.

But, an opposing view is that the current price of the S&P 500 is comparable to its value in 1999, despite the fact that its earnings and dividends have doubled since that time, and suggesting the market has additional room to grow.

The Future is UnKnown

There is no crystal ball. What the stock market will do in the near future is anyone’s guess. As uncertainty is always a factor when investing, developing a portfolio that represents your risk tolerance and investment time horizon is critical.

Many physicians and investors realize they need to scale back the assertiveness of their portfolio as they approach retirement, but why is this important? The mechanics of an investment portfolio are very different for a portfolio in the distribution phase than for a portfolio still accumulating assets. If an investor is taking withdrawals from their account, it is much more difficult to recover from losses because distributions only serve to exacerbate the market decline.

Dr. Israelsen Speaks

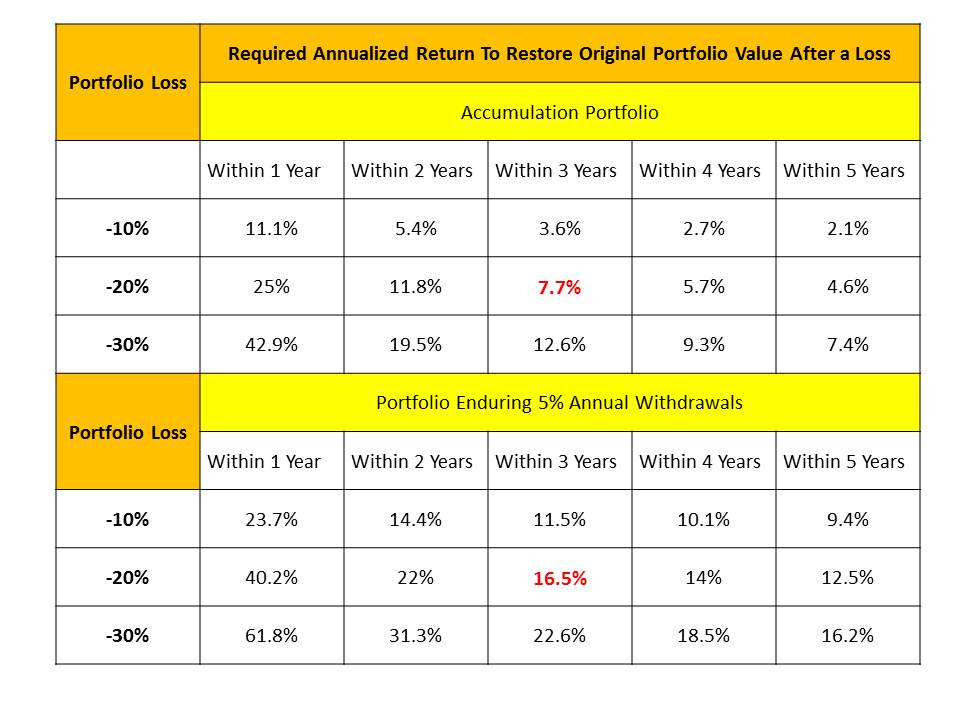

As Craig Israelsen PhD points out in the February 2013 issue of Financial Planning Magazine with the following illustration, a portfolio enduring annual 5% withdrawals faces a much steeper climb back to break even after a loss than does an accumulation portfolio:

Clearly, the conclusion is if you are taking distributions from your account, or intend to do so soon, it is vitally important to avoid large losses. As it may be realistic for investors still accumulating assets to recover from a -20% loss by obtaining an average annualized return of 7.7% for three years, it is unlikely that a retiree taking distributions from his account will get the 16.5% annual return required for three years in order to recover from a similar loss.

Diversify

Protect yourself from unsustainable losses by maintaining adequate diversification within your portfolio. Bonds serve as a buffer against volatility and will likely decrease your loss during stock market corrections.

Additionally, ensure your portfolio has sufficient exposure to various asset classes: large cap, mid cap, and small cap stocks; US, international, and emerging market stocks; government, corporate, international, and emerging market bonds. Investing in multiple asset categories will protect your portfolio from a catastrophic loss next time a bubble in a market sector pops.

Assessment

Speak with a Certified Medical Planner™ or fiduciary and physician focused financial advisor to ensure your portfolio is assertive enough to meet your retirement goals while maintaining an acceptable level of risk. If you wait for the market to turn before taking action, it may be too late.

www.CertifiedMedicalPlanner.org

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Link: http://feeds.feedburner.com/HealthcareFinancialsthePostForcxos

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

***

8

8

Share this:

Filed under: CMP Program, Investing | Tagged: certified medical planner, Craig Israelsen, DJIA, emerging market stocks, financial planning magazine, Investing, Lon Jefferies, NASDAQ, S&P 500, stock market crash |

Lon,

The Fed will probably wait to see six months of strong employment and at least two quarters of 3.0 percent gross domestic product growth before it seriously considers tightening.

Your thoughts?

Jethro

LikeLike

You really can time the stock market

Yes, most people who try to time the market screw it up, but that doesn’t mean the idea is flawed.

http://money.msn.com/investing/you-really-can-time-the-stock-market

So, these few key statistics can help average investors buy low and sell high.

Edmund

LikeLike

The “CRASH”

Predictors of the 1929 Crash See a 65% Chance of a 2015 Global Recession

http://www.msn.com/en-us/money/markets/predictors-of-1929-crash-see-65percent-chance-of-2015-global-recession/ar-AA7qeix

What about you?

Rohan

LikeLike

The crash?

When the stock market last crashed, these sectors fared best.

http://www.msn.com/en-us/money/markets/when-the-stock-market-last-crashed-these-sectors-fared-best/ar-BBlXRVB?li=AA4Zjn&ocid=iehp

And … why the market crashed?

http://www.msn.com/en-us/money/markets/why-stocks-are-tumbling-6-years-into-the-bull-market/ar-BBm0cPw?li=AA4Zjn&ocid=iehp

Roy

LikeLike