Understanding the Impending Retirement-Planning Crisis

[By Somnath Basu PhD, MBA]

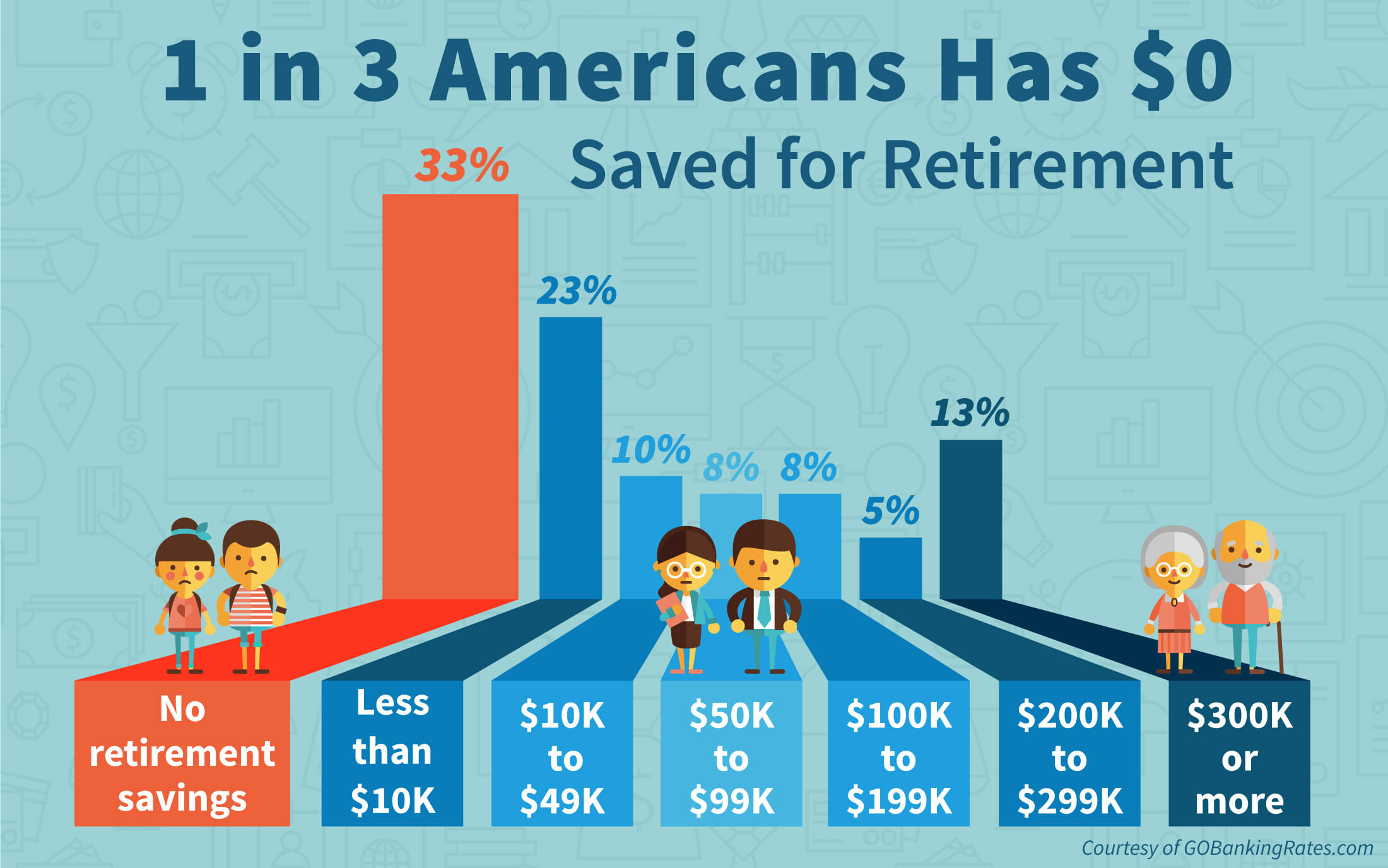

A serious retirement-planning crisis is looming in the US with many Baby Boomer physicians, and others, having already spent a portion of their nest egg and undermining any hope for a comfortable lifestyle unless they continue to work. Notwithstanding medical professionals, look no further than an annual “retirement confidence” survey conducted by the Employee Benefit Research Institute and Mathew Greenwald & Associates in each of the past 17 years. Nearly two in five of working Americans responding to the latest survey indicated that they have taken no action in the face of reductions in their employer-provided retirement benefits.

Consumption Equals Happiness?

The population is constantly told that consumption equals happiness. At the same time they are not being asked to understand about the implications of borrowing to fund for such consumption. Before we can expect to effect a change in the ensuing pattern of a vicious cycle, the population mass must have a clear understanding of the difference between needs (e.g., retiring with peace of mind) and desires (e.g., cruises or living the high life).

Negative Savings Rate

When savings first dipped into negative territory during the Great Depression in 1932 and 1933, people didn’t have enough to eat, whereas there has been no such urgency to raid nest eggs since the repeat of this performance in 2005 when the rate fell to minus 0.5 percent. Our grandparents were shining stars in the way they worked hard to build this country’s infrastructure and manufacturing sector, saved every red cent they could get their hands on and created affluence on a mass scale. Today we’re able to enjoy the fruit of their labor. But, somehow their values were lost on future generations.

Changing American Culture

Many of the nation’s top engineers and scientists now hail from China, India and other Asian countries as American culture has undergone a dramatic change to the point where jocks and cheerleaders are more valued than computer geeks and science nerds in our schools. We inherited so much affluence that it made us lazy as a society. The seeds of our destruction have been sown, but it’s up to our politicians, educators and other leaders, including financial advisors, to help reverse this disturbing pattern before it’s too late.

Many people fall into the trap of rushing through dinner and unwinding in front of the TV where a big part of the problem lies in slick and subtle, and hard to resist, primetime advertising and marketing messages (prime time for subtle messages) that seduce viewers into purchasing luxury cars or flying to far-flung resorts where they can sip umbrella-clad cocktails alongside affluent vacationers.

Americans in Debt

A recent wave of foreclosures has put Americans deeper in debt, with the sub-prime crisis exposing despicable predatory lending practices. But, research has shown the wreckage also could be found strewn across in the mid-prime and prime markets as middle-class borrowers struggled to pay adjustable rate mortgages. High hopes have been pinned on the stock market helping people crawl out from this crisis just like when the real estate market had softened the blow when the tech-bubble burst at the turn of this century. So far, this has happened, to an extent. But, if the stock market starts reeling again, then it will spell even bigger trouble. Add to this the international trade imbalance, which implies foreign governmental funding of our conspicuous consumption, and which comes with high interest rates that need to be paid to the lenders, again to such countries as China, India and other emerging economies, and a bigger, worse picture emerges.

Personal Bankruptcies

Personal bankruptcies have an even more devastating effect on an individual’s ability to plan for the future, particularly since the laws pertaining to this area were toughened to a point where reckless spenders will need to muster fiscal and financial discipline as never before. The doomsday scenario is that children now run the risk of inheriting debt instead of wealth, and it’s unconscionable to think future generations would have a standard of living that’s worse than their parents or grandparents.

Assessment

The true grit associated with being an American is to rise up in the face of adversity – a frontier spirit that drew me this remarkable country. We’ve weathered numerous storms and can do it again. But, it requires a serious commitment to stopping mindless consumption of goods and services, as well as understanding there’s a difference between basic needs and pie-in-the-sky desires.

NOTE: Dr. Somnath Basu is a Professor of Finance at California Lutheran University and the Director of its California Institute of Finance. He is also the creator of the innovative AgeBander technology www.agebander.com for planning retirement needs.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Filed under: Experts Invited, Financial Planning, Retirement and Benefits, Risk Management | Tagged: California Institute of Finance, california lutheran university, Employee Benefit Research Institute, Negative Savings Rate, Personal bankruptcies, physician debt, retirement planning, Somnath Basu, www.agebander.com | 3 Comments »