By Rick Kahler CFP™

***

***

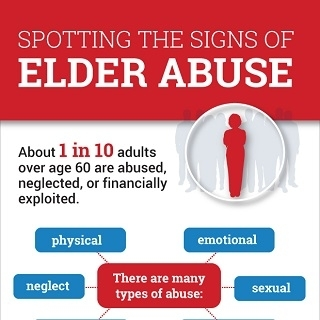

One serious risk to financial wellbeing in retirement that is difficult to talk about is financial exploitation. Someone whose cognitive abilities are declining is vulnerable to harm from both financial predators and their own financial misjudgments. Protecting such clients is a crucial part of a financial advisor’s role.

A little-known but important law, the Senior Safe Act, was enacted in 2018. It encourages financial advisors and institutions to report suspected elder abuse by offering immunity from legal liability when reports are made in good faith and with reasonable care. To qualify for these protections, financial professionals must undergo annual training to recognize the signs of exploitation and know how to act on their suspicions.

In many ways, the Senior Safe Act mirrors the duty of therapists to report when clients are threats to themselves, such as when a client becomes suicidal. Just as a therapist must balance confidentiality with the moral and legal responsibility to protect their client from harm, a financial advisor must weigh privacy against the need to prevent financial exploitation. Both roles rely on professional judgment, training, and the courage to act when the stakes are high.

Financial advisors, accountants, and attorneys are often the first to notice troubling signs that someone is being taken advantage of financially. These might include sudden large withdrawals, changes to account ownership or beneficiaries, or a newly and overly involved friend or family member. Behavioral shifts like confusion, anxiousness, secretiveness, or uncharacteristic deference are also red flags. These patterns are unsettling and demand attention, even when stepping in is uncomfortable.

Reporting possible elder abuse isn’t always straightforward, especially if the suspected abuser is a family member. As an advisor, I worry about misunderstandings, potential conflicts with the family, and even the possibility of damaging a relationship with the client. None of this is easy, But when the signs of exploitation become clear, staying silent could mean allowing harm to continue. That’s a risk I can’t take.

One of the tools I started using decades ago is the trusted contact disclosure form. This simple but powerful document allows clients to name someone my firm can contact if they notice unusual activity, such as a suspicious withdrawal or transfer. The trusted contact does not have control over the client’s account but serves as a resource to verify their well-being and ensure that their financial decisions align with their long-term goals. If you as a client have not signed such a form, it’s worth discussing with your advisor as a preventative step.

If you are concerned about the financial well-being of an elderly loved one, it’s crucial to alert not only their financial advisor but also other professionals like accountants, attorneys, or bankers. These professionals may have insights or access to information you don’t have, and by sharing your concerns, you provide a broader picture that can help them detect and address issues more effectively. Even if they are already monitoring for red flags, your input can provide valuable context to guide their next steps.

Difficult though it may be, stepping into uncomfortable territory is often essential to protecting vulnerable individuals. Whether it’s a financial advisor detecting exploitation or a therapist intervening in a mental health crisis, the goal is the same—to prevent harm while respecting the person’s autonomy.

The Senior Safe Act is a reminder that sometimes the most impactful safeguards work quietly behind the scenes. Taking simple steps like completing a trusted contact form or encouraging your loved one to work with a reputable, fiduciary advisor can make all the difference. Vigilance is an act of care that helps protect someone’s financial assets as well as their dignity and well-being.

COMMENTS APPRECIATED

Subscribe and Refer

***

***

Share this:

Filed under: "Ask-an-Advisor", Ethics, Experts Invited, Financial Planning, Glossary Terms, LifeStyle, mental health | Tagged: elder abuse, Elder Investment Fraud and Financial Exploitation Project, finance, financial exploitation, harm, kahler, mental health, news, Relationships, rick kahler, Senior abuse, Senior Act, Senior Safe, trauma | Leave a comment »