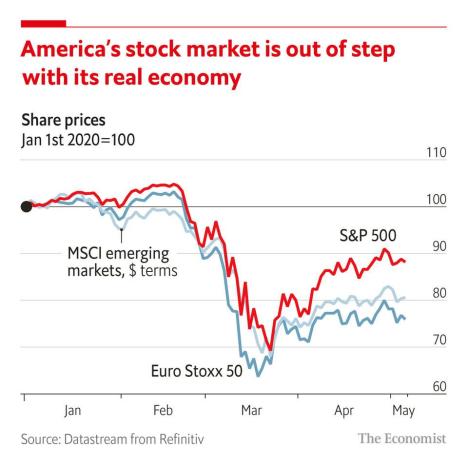

Share this:

Filed under: Experts Invited, Investing, Videos | Tagged: Dan Timotic CFA, Stock Market Insights for May 2020, stock markets | Leave a comment »

ME-P SYNDICATIONS:

WSJ.com,

CNN.com,

Forbes.com,

WashingtonPost.com,

BusinessWeek.com,

USNews.com, Reuters.com,

TimeWarnerCable.com,

e-How.com,

News Alloy.com,

and Congress.org

![]()

![]()

BOARD CERTIFICATION EXAM STUDY GUIDES

Lower Extremity Trauma

[Click on Image to Enlarge]

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

![]()

ePodiatryConsentForms.com

ePodiatryConsentForms.com

“Providing Management, Financial and Business Solutions for Modernity”

“Providing Management, Financial and Business Solutions for Modernity”

Filed under: Experts Invited, Investing, Videos | Tagged: Dan Timotic CFA, Stock Market Insights for May 2020, stock markets | Leave a comment »

Are Soaring Health-Care Costs Hurting the U.S. Economy?

![]()

By Dan Timotic CFA

About 8% of U.S. household spending went toward health care in 2015, up from 5.8% in 2007. Even though the growth of nationwide health-care spending has slowed, the cost burden is falling more heavily on consumers.1

More than 118 million people qualify for coverage through government programs such as Medicare, which serves individuals age 65 and older and the disabled, or Medicaid, which provides care for the poor. Still, more than 55% of the U.S. population rely on health insurance provided by an employer.2

The health-care landscape has changed over the last decade, but some economists believe uncontained costs still pose a threat to broader economic growth. Here’s a closer look at recent trends, and why it’s more important than ever to be an informed health-care consumer.

Public Spending

Growth in U.S. health-care spending has outpaced total economic growth over the past five decades. In 2014, health-care expenditures accounted for about 17.5% of GDP, up from 5.6% in 1965.3 Though major advances in medical technology have contributed to spending growth, they have also led to better health and well-being overall.4

Public-sector spending has grown more quickly than private spending, largely due to an aging population, rising Medicare enrollment, and the expansion of Medicaid. The share of total spending by Medicare and Medicaid increased from 6.8% in 1966 to 36.8% in 2014.5

ACA Under Way

The Affordable Care Act created state-based exchanges where self-employed individuals, part-time workers, and others without access to group coverage can buy private health insurance. Consumers can compare plans online, and families with incomes up to 400% of the federal poverty level may be eligible for tax credits that reduce premiums. As income rises, subsidies decrease. In 2016, about 85% of the 12.7 million individuals who purchased coverage from the Health Insurance Marketplace received a subsidy.6

Since 2014, all citizens and legal residents have been required to have “minimum essential” health coverage or pay a penalty. The health insurance mandate was intended to add healthy individuals to the insurance pool and counterbalance a provision that prohibits insurers from excluding people with pre-existing conditions. As a result, the uninsured rate has decreased from 13.3% in 2013 to 9.1% in 2015.7

![]()

Workplace Plans

Employers have been paying around 80% of individual health insurance premiums, but plan changes, including higher deductibles and coinsurance rates, have shifted costs to workers who use health-care services.8

For example, the average deductible for individual coverage in an employer-provided health plan was $1,318 in 2015, up from $917 in 2010. A deductible is the amount the patient must pay before the insurance payments kick in. Health insurance deductibles grew 67% between 2010 and 2015, almost three times as fast as premiums and about seven times as fast as wages and inflation.9

If health insurance premiums continue to rise, it is conceivable that employers could pass more of the costs on to workers by raising premiums and coinsurance or limiting wage increases.

Accounting for Costs

It’s estimated that total U.S. health- care spending increased 5.5% to reach $3.2 trillion in 2015, and growth is projected to average 5.8% annually through 2025. Cost increases have moderated after averaging nearly 8% annually over the previous two decades, but they are still increasing much more than overall inflation.10 Prescription drug prices have been rising at a faster pace. According to one drug-benefits manager, the average price of brand-name drugs rose 16.2% in 2015, surging 98.2% since 2011.11

The research and development of breakthrough medical technologies is undoubtedly a valuable endeavor. Even so, experts say newer and more expensive treatments are not always more effective than existing lower-cost options. It has also been suggested that the fee-for-service payment model — in which insurers reimburse providers based on the number and type of treatments — may drive inefficiency and unnecessary spending by rewarding the quantity rather than the quality of care.12

Economic Impact

Even with insurance coverage, an illness or injury can cause financial pain for a middle-class family with limited disposable income. The prospect of medical bills may cause some families to skip or postpone necessary care, and those who do seek treatment have less money available to spend on other basic needs. A Brookings Institution analysis found that middle-income household spending on health care increased nearly 25% between 2007 and 2014, while spending on restaurant meals and clothing dropped significantly (–13.4% and –18.8%, respectively).13

Health spending across the economy is expected to accelerate and reach 20% of GDP by 2025, which could put additional strain on consumers, employers, and the federal budget.14

Open Enrollment

This is the time of year when employers introduce changes to their benefit offerings, so choosing — and then using — your health plan carefully could help you save money. Before you sign up for a specific plan, consider the extent to which your prescription drugs are covered, estimate your potential out-of-pocket costs based on last year’s usage, and check to see whether your doctors are in the insurer’s network.

Citations:

1, 8, 11, 13) The Wall Street Journal, August 25, 2016 2, 7) U.S. Census Bureau, 2016 3, 5, 10, 14) Centers for Medicare and Medicaid Services, 2016 4, 12) The Brookings Institution, 2015 6) U.S. Department of Health and Human Services, 2016 9) Kaiser Family Foundation, 2015.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

![]()

***

Filed under: Health Economics, Health Insurance, Healthcare Finance | Tagged: ACA, Are Soaring Health-Care Costs Hurting the U.S. Economy?, Dan Timotic CFA, Health spending | 5 Comments »

![]()

Or … Third Time Around!

By Dan Timotic CFA

[Managing Principal]

Roughly four in 10 new marriages in 2013 included at least one partner who had been married before, and altogether about 42 million Americans have been married more than once [1].

A second marriage can create numerous estate planning challenges, especially when you wish to provide for both your current spouse and your children from a previous marriage. If you remarry later in life, your spouse and your adult children may not develop a close relationship, which could complicate matters when you die.

With a traditional family, estate assets are often inherited by the surviving spouse and eventually passed down to the couple’s children. Blended families, however, may require a more detailed strategy.

Start by having an honest conversation with your spouse (or fiancée) about your separate and shared finances and goals for the future.

Think Ahead

A prenuptial agreement is a written contract between prospective spouses that states how assets will be owned and distributed during the marriage, in the event of divorce, and at death. Each spouse’s financial rights and responsibilities are predetermined and clearly spelled out, and the contract can be altered or broken only with the consent of both parties.

Prenuptial agreements are not for everyone, but they could help reduce conflict between a surviving spouse, your adult children, and other family members.

***

[Broken Heart]

***

Useful Trusts

Placing assets in a properly structured living trust makes it more difficult for someone to contest your will and also avoids probate. The assets would be available to your heirs more quickly, and your private information would be kept out of the public domain.

A qualified terminable interest property (QTIP) trust is a marital trust typically used in conjunction with a bypass trust. When you die, your spouse receives a lifelong income from the assets in the trust. After your surviving spouse dies, the remaining trust assets are distributed to your children, or other designated heirs, according to your specific instructions.

A QTIP trust might be a viable option if you’re certain that a permanent financial relationship between your spouse and adult children will not be a constant source of tension and frustration. If you are uncomfortable making your children wait until your spouse’s death to receive an inheritance, it might make more sense to eliminate the financial connection between your surviving spouse and your children.

***

[Divorce Decree]

***

Pick Your Approach

One common arrangement is simply to designate a specific percentage of estate assets to be distributed outright for the spouse, each child, and any other heirs. This way, everyone shares in the appreciation or depreciation of the assets.

Another method involves allocating assets to various heirs based on specific financial needs or benefits. For example, a surviving spouse might inherit the home and retirement accounts, while the children might receive other financial assets such as shares of a business, family heirlooms, or the proceeds of a life insurance policy.

The beneficiary designations on all your retirement accounts, brokerage accounts, and insurance policies should also be updated and consistent with your overall estate plan. If your children are adults, you may want to keep them informed about your decisions so that everyone knows what to expect.

Assessment

Remember – Trusts incur up-front costs, often have ongoing administrative fees, and involve complex tax rules and regulations. You should consider the counsel of an experienced estate planning professional and your legal and tax advisors before implementing a trust strategy.

Citation: Pew Research Center, 2014

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

8

***

Filed under: Financial Planning, Risk Management | Tagged: Dan Timotic CFA, divorce planning, QTIP | Leave a comment »

![]()

By Dan Timotic CFA

More than 73 million Americans actively participate in employer-sponsored defined-contribution plans such as 401(k), 403(b), and 457 plans.

If you are among this group, you’ve taken a big step on the road to retirement, but as with all investing, it’s important to understand your plan and what it can do for you.

Here are a few ways to make the most of this workplace benefit.

***

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

***

Filed under: Investing, Portfolio Management, Retirement and Benefits | Tagged: Dan Timotic CFA, Managing Your 401(k) | 2 Comments »

![]()

Below Zero

By Dan Timotic CFA

As of late April 2016, six central banks in Europe and Asia have adopted negative interest rates in an effort to stimulate their national economies. The experiment began in Denmark in 2012, but the big step came in June 2014 when the European Central Bank (ECB) dropped its benchmark rate below zero. Sweden and Switzerland soon followed, and Japan and Hungary went negative in early 2016. Taken together, these economies represent about one-fourth of global economic output.1–2

Although the Federal Reserve remains committed to raising the federal funds target rate, the Fed is watching the efforts of foreign central banks with an eye toward expanding its tools in the event of an economic downturn. On a more immediate level, the overseas experiment is affecting the dollar and helping to suppress interest rates in the United States.3–4

Reverse Economics

Central banks lower interest rates for two fundamental reasons: (1) to encourage business investing and consumer spending by making it cheaper to borrow and less lucrative to hold onto cash; and (2) to lower the value of the national currency in order to make exports more appealing and create an expectation of future inflation, which may further stimulate current spending.

The push into negative territory reflects the same goals, but it reverses traditional economic concepts by turning borrowers into creditors and creditors into borrowers. Although specifics vary, the central banks are pulling rates downward by assessing a negative interest rate on certain short-term deposits from commercial banks. These banks actually lose money on their deposits, which in theory should stimulate the banks to lend money to other banks, businesses, and consumers.

The greatest fear regarding negative rates is a mass exodus from the banking system. The experiments in Europe and Japan are still new and the rates relatively moderate, but so far banks and their customers seem to be weathering the transition, albeit with lower margins and additional fees.5 Deposits in eurozone banks grew by $327 billion from June 2014 (when negative rates were implemented) through October 2015.6 Some banks assess negative rates on large commercial customers, but they have been hesitant to do so with retail customers. One small Swiss bank instituted a charge of 0.125% on savings accounts and gained more customers than it lost.7

These early responses suggest that businesses and consumers may be willing to pay a premium to deposit cash assets safely in a bank. Keeping large amounts of cash outside of a bank can be expensive, requiring guards, safes, and other security measures. Average consumers might keep cash under a mattress, but it is difficult to pay bills — or buy merchandise over the Internet — with cash. This cost-benefit balance may change if rates continue to decline.

Bonds and Mortgage Rates

By April 2016, more than $8 trillion of government bonds in Europe and Japan were trading at negative interest rates.8 As with banking, this suggests that some investors are willing to accept a loss in return for the security of government bonds. However, negative or very low yields may put pressure on pension plans and insurance companies, which depend on low-risk, fixed-rate investments.9

Low rates have driven housing prices up in Denmark and Sweden, creating fears of a “bubble.” Some Danish homeowners have even seen the monthly interest on their adjustable-rate mortgages turn into monthly credits due to negative rates.10

***

***

Currency Competition

After the ECB instituted negative rates, the euro dropped sharply against the U.S. dollar and was still down about 17% in April 2016.11 A strong dollar stimulates European exports at the expense of U.S. exports and makes it more difficult to raise U.S. interest rates, which would only make the dollar more appealing for foreign investors.

Denmark, Sweden, Switzerland, and Hungary all dropped rates in large part to keep their currencies competitive with the euro.12 Denmark’s experience, the longest-running experiment, suggests that negative rates may be effective when the primary goal is to control currency but less effective as a stimulus to growth.13 On the other hand, Japan’s initial efforts have seen the yen rise unexpectedly against the dollar, unsettling markets.14

How Low Can They Go?

Early eurozone results are tepid but encouraging. Annual GDP growth improved to 1.5% in 2015 versus 0.9% in 2014, and lending by eurozone banks (which had been decreasing) increased slightly by 0.6% in 2015.15 It’s unclear how much worse the European situation might be without negative rates.

Assessment

After a tentative beginning, central banks have become more aggressive. In March 2016, the ECB dropped its deposit rate to –0.40%, and the Swiss National Bank rate was –0.75%.16 It remains to be seen how banks and consumers will respond to even lower rates, and whether reverse economics will strengthen the global economy or create new challenges.

All investments are subject to market fluctuation, risk, and loss of principal. Investments, when sold, may be worth more or less than their original cost. Investing internationally carries additional risks, such as differences in financial reporting and currency exchange risk as well as economic and political risk unique to a specific country. This may result in greater investment price volatility.

References

1, 5, 9, 16) International Monetary Fund, 2016 2, 12) Reuters, April 10, 2016 3) The New York Times, March 5, 2016 4, 11) European Central Bank, 2016 6) The New York Times, December 3, 2015 7–8, 10, 14) The Wall Street Journal, April 14, 2016 13) Bloomberg, February 15, 2016 15) The Wall Street Journal, February 28, 2016

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

***

Filed under: Financial Planning, Investing | Tagged: "Negative" Interest Rates, Dan Timotic CFA | 6 Comments »