BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

Posted on October 4, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

By Health Capital Consultants, LLC

***

***

On September 5, 2025, the Federal Trade Commission (FTC) voted to dismiss its appeals in two court cases, effectively terminating the Biden Administration’s pursuit of a comprehensive noncompete ban. The 3-1 Commission vote represents a fundamental shift in federal competition enforcement strategy.

This Health Capital Topics article reviews the history of the noncompete ban, the FTC’s recent activities regarding competition, and the implications for healthcare organizations. (Read more…)

After a lifetime of hard work practicing medicine and saving, you’re at the retirement finish line. Instead of a paycheck, you’re relying on your nest egg and investment income to cover the bills. Picking the right investments is even more important, as you won’t have much chance to recover as a retired MD, DO, DPM or DDS.

“You made it to the top of the mountain through a systematic approach and are trying to make your way down safely,” says retirement planner John Gillet John Gillet in Hollywood, Fla. “Why throw all caution to the wind and try something different now?”

***

***

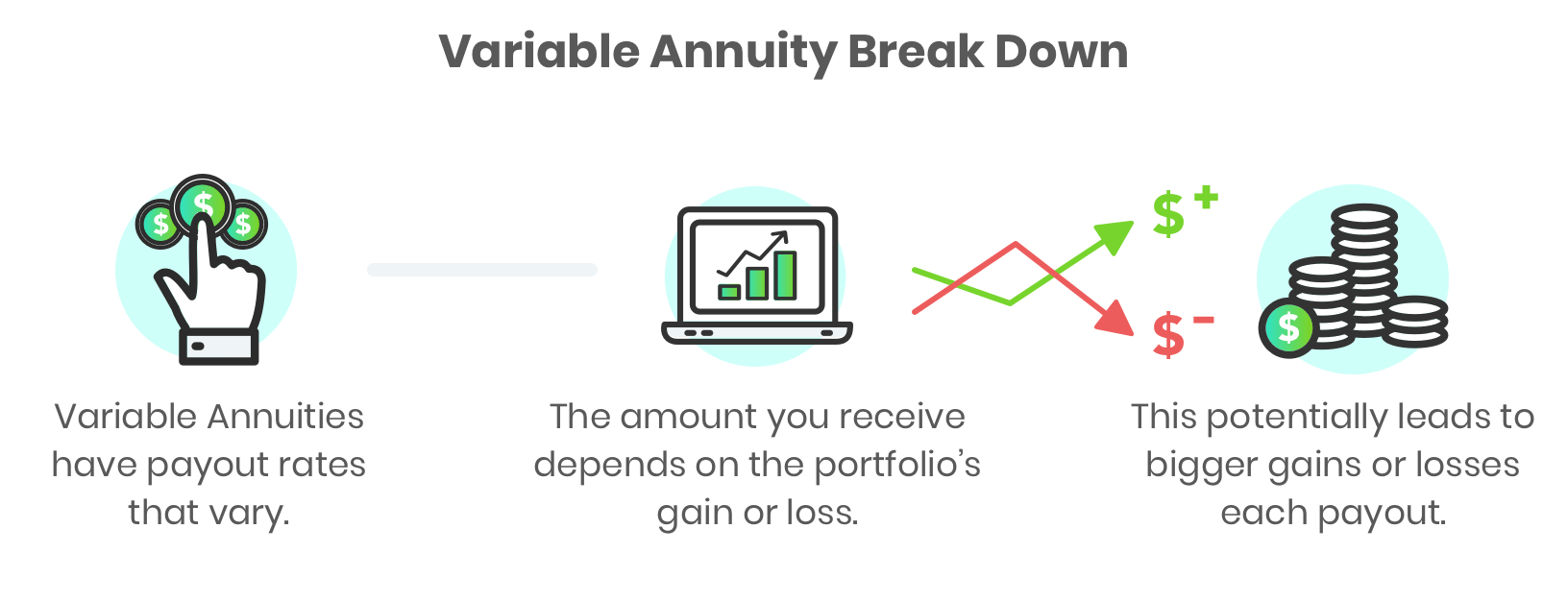

Definitions

An annuity is an insurance contract designed to grow your money and then repay it as income. There are different versions. An immediate annuity turns your lump sum into future guaranteed income payments, like your own personal pension. They are simple to understand with no or small fees.

Fixed annuities pay a guaranteed interest rate over a set period to grow your money, like 5% a year for five years. These options could make sense as part of a retirement plan.

A variable annuity, on the other hand, invests your savings in mutual funds. While you can buy riders that guarantee a minimum income, you’ll be paying very much for it. “All in, the annual fees can be 3% or more of your balance,” says Jeff Bailey, an advisor from Nashville. “That’s a huge withdrawal rate from your portfolio versus investing on your own.”

The variable annuity will lock up your money for years. If you cancel early, you owe a surrender charge that could start at 7% or more of your annuity balance before gradually going down as time goes by. “Clients believe they can walk away with their contract value, but that’s often not true,” says Bailey.

SPEAKING: Dr. Marcinko will be speaking and lecturing, signing and opining, teaching and preaching, storming and performing at many locations throughout the USA this year! His tour of witty and serious pontifications may be scheduled on a planned or ad-hoc basis; for public or private meetings and gatherings; formally, informally, or over lunch or dinner. All medical societies, financial advisory firms or Broker-Dealers are encouraged to submit an RFP for speaking engagements: CONTACT: Ann Miller RN MHA at MarcinkoAdvisors@outlook.com -OR-http://www.MarcinkoAssociates.com

Posted on October 4, 2025 by Dr. David Edward Marcinko MBA MEd CMP™

OVERHEARD IN THE DOCTOR’S LOUNGE

***

***

By D. Kellus Pruitt DDS

According to money journalists Max Tailwagger and Allan Roth of MoneyWatch, the trade publication Medical Economics Magazine [“advertising supplement”] nearly listed a dog on its’ 2013 list of Best Financial Advisors for Doctors. Indeed, being listed as a top financial advisor in this publication would enhance any advisor’s credibility as well as reach a high income readership.

For example, several advisors in the Financial Planning Association, mentions this prestigious award year after year. And, the NAPFA organization of fee-only financial planners has issued press releases when member advisors make this annual list. In fact, in 2008, it touted that 52/150 listed FAs were NAPFA members.

Yet, the dog is well known in the financial advisory world, having allegedly received a plaque as one of 2009 America’s Top Financial Planners by the Consumers’ Research Council of America, and has appeared in several books including Pound Foolish and Money for Life. The fee for Maxwell Tailwagger CFP® [a five year old Dachshund] was reported to be $750 with $1,000 for a bold listing. Colorado Securities Commissioner Fred Joseph is reported to have said, “Once again, Max is gaining national notoriety for his astute, and almost superhuman, abilities in the financial arena.”

The only two qualifications for the listing were to pay the fee and not have a complaint against them. In 2009, James Putman, then the NAPFA chairman who touted his own Medical Economics award, was charged by the SEC for securities fraud. NAPFA spokesperson Laura Fisher allegedly opined that “NAPFA no longer promotes the Medical Economics Top Advisors for Doctors list. We felt promoting a list that included stock-brokers was inconsistent with NAPFA’s mission to advance the fee-only profession.” When an advisor name drops an honor to you, congratulate him and then ask how s/he achieved the award. Ask how many nominees versus award recipients there were. What were the criteria for selection and how were they nominated. Ask if they had to pay for the honor, and go online to check out the organization.

Then ask yourself this question: If your financial advisor is buying credibility, do you really want to trust your financial future to him or her?