Is it still relevant today?

Courtesy: www.CertifiedMedicalPlanner.org

The law was named in 1860 by Henry Dunning Macleod, after Sir Thomas Gresham (1519–1579), who was an English financier during the Tudor dynasty. However, there are predecessors.

The law had been stated earlier by Nicolaus Copernicus. It was also stated in the 14th century, by Nicole Oresme in his treatise On the Origin, Nature, Law, and Alterations of Money, and by jurist and historian Al-Maqrizi (1364–1442) in the Mamluk Empire; and noted by Aristophanes in his play The Frogs, which dates from around the end of the 5th century BC.

***

***

IOW: It is the tendency for money of lower intrinsic value to circulate more freely than money of higher intrinsic and equal nominal value (often expressed as “Bad money drives out good”).

***

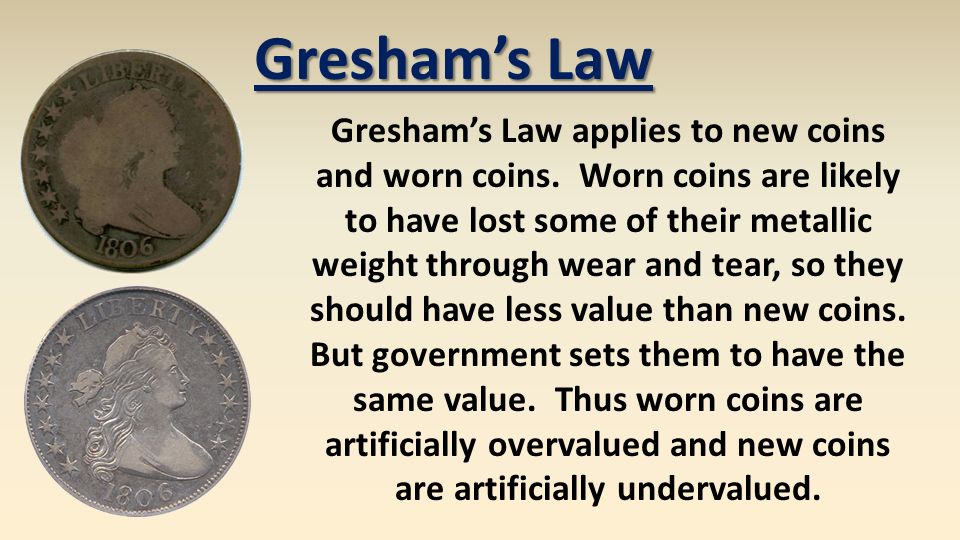

Gresham’s Law applies to new coins and worn coins. Worn coins are likely to have lost some of their metallic weight through wear and tear, so they should have less value than new coins. But government sets them to have the same value. Thus worn coins are artificially overvalued and new coins are artificially undervalued.

***

So, is Gresham’s Law still relevant today?

THINK: The modern Bitcoin, and related crypto-currency, controversy? We asked colleague Timothy J. McIntosh CFP® MPH CFA for some insights.

ESSAY: https://medicalexecutivepost.com/2014/01/23/understanding-currencies-bitcoins/

Assessment

Your thoughts are appreciated.

Conclusion

Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements.

Book Marcinko: https://medicalexecutivepost.com/dr-david-marcinkos-bookings/

Subscribe: MEDICAL EXECUTIVE POST for curated news, essays, opinions and analysis from the public health, economics, finance, marketing, IT, business and policy management ecosystem.

DOCTORS:

“Insurance & Risk Management Strategies for Doctors” https://tinyurl.com/ydx9kd93

“Fiduciary Financial Planning for Physicians” https://tinyurl.com/y7f5pnox

“Business of Medical Practice 2.0” https://tinyurl.com/yb3x6wr8

HOSPITALS:

“Financial Management Strategies for Hospitals” https://tinyurl.com/yagu567d

“Operational Strategies for Clinics and Hospitals” https://tinyurl.com/y9avbrq5

***

8

8

Share this:

Filed under: Alternative Investments, Experts Invited, Glossary Terms, Investing | Tagged: Bitcoin, crypto-currency, GRESHAM’S LAW, Timothy J. McIntosh CFP® | 2 Comments »