BOARD CERTIFICATION EXAM STUDY GUIDES Lower Extremity Trauma

[Click on Image to Enlarge]

ME-P Free Advertising Consultation

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

Medical & Surgical e-Consent Forms

ePodiatryConsentForms.com

iMBA Inc., OFFICES

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

ME-P Publishing

SEEKING INDUSTRY INFO PARTNERS?

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

As a new physician investor, it’s important to know the distinctions between like measurements because the market allows firms to advertise their numbers in ways not otherwise regulated. Often companies will publicize their numbers using either GAAP or non-GAAP measures. GAAP, or generally accepted accounting principles, outlines rules and conventions for reporting financial information. It is a means to standardize financial statements and ensure consistency in reporting.

When a company publicizes its earnings and includes non-GAAP figures, it means it wants to provide investors with an arguably more accurate depiction of the company’s health (for instance, by removing one-time items to smooth out earnings). However, the further a company deviates from GAAP standards, the more room is allocated for some creative accounting and manipulation.

When looking at a company that is publishing non-GAAP numbers, new physician investors should be wary of these pro forma statements, because they may differ greatly from what GAAP deems acceptable.

GAAP is set forth in 10 primary principles, as follows:

Principle of consistency: This principle ensures that consistent standards are followed in financial reporting from period to period.

Principle of permanent methods: Closely related to the previous principle is that of consistent procedures and practices being applied in accounting and financial reporting to allow comparison.

Principle of non-compensation: This principle states that all aspects of an organization’s performance, whether positive or negative, are to be reported. In other words, it should not compensate (offset) a debt with an asset.

Principle of prudence: All reporting of financial data is to be factual, reasonable, and not speculative.

Principle of regularity: This principle means that all accountants are to consistently abide by the GAAP.

Principle of sincerity: Accountants should perform and report with basic honesty and accuracy.

Principle of good faith: Similar to the previous principle, this principle asserts that anyone involved in financial reporting is expected to be acting honestly and in good faith.

Principle of materiality: All financial reporting should clearly disclose the organization’s genuine financial position.

Principle of continuity: This principle states that all asset valuations in financial reporting are based on the assumption that the business or other entity will continue to operate going forward.

Principle of periodicity: This principle refers to entities abiding by commonly accepted financial reporting periods, such as quarterly or annually.

Posted on August 15, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Changes to a popular 401(K) tax deduction are set to hit millions of high-earning Americans from next year. Workers over the aged of 50 are entitled to make catch-up contributions to their 401(K)s worth up to $7,500 this year. The annual cap on all contributions is $30,000.

But from 2024, those earning over $145,000 will no longer be able to put these catch-up payments into a traditional 401(K). Instead, the money will be only funneled into a Roth IRA account, according to new rules passed through Congress in December.

In more than 118,000 real transactions at the university bookstore, buyers tended to slap their plastic on the counter for school supplies but pay with cash for “harder-to-justify” items like a stuffed plush mascot. And when asked how they’d pay for a hypothetical Reiki session, participants leaned toward credit card when the treatment was described as doctor-recommended but toward cash when they were told it was just an impulse purchase.

Posted on July 25, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

The IRS will not come to the front / back door

The tax agency will no longer make unannounced visits to taxpayers’ homes or businesses to collect payments due (in most cases). The IRS said it was halting the controversial practice, which has been around since at least the 1950s, to protect its agents’ safety.

Instead, the agency will send letters requesting that the taxpayer schedule an appointment. In specific cases, such as to deliver a summons or subpoena or seize assets, an unannounced visit may still occur, but there are only a few hundred of those each year compared to tens of thousands of the more routine visits, according to Reuters.

Posted on July 5, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Here is where the major benchmarks ended on Monday:

The S&P 500 Index was up 5.21 points (0.1%) at 4,455.59; the Dow Jones Industrial Average (DJIA) was up 10.87 points at 34,418.47; the NASDAQ Composite was up 28.85 points (0.2%) at 13,816.78.

The 10-year Treasury note yield (TNX) was up about 4 basis points at 3.862%.

The CBOE Volatility Index® (VIX) was little changed at 13.58.

Financial companies had a good day Monday, with the KBW Regional Banking Index (KRX) rising more than 2%.

The consumer discretionary sector was also strong, while energy companies got a bump as crude oil futures reached their highest level in more than a week.

Health Care stocks lagged.

***

Wall Street is hoping for a strong start to the second half of 2023 taking cues from the recent tech rally that has boosted the overall investor sentiment. Turning toward the U.S.-China trade war, on Monday, the mainland posed restrictions on the export of gallium and germanium to the U.S. citing national security concerns. These metals are used in semiconductor manufacturing and the curb is being used as a means of retaliation to the U.S. chip ban on China.

Remarkably, Tesla (NASDAQ:TSLA) stock has been on an uphill climb lately, thanks to the growing adoption of its North American Charging Standard (NACS) charging connectors by major automakers including General Motors (NYSE:GM), Ford (NYSE:F), and Rivian (NASDAQ:RIVN). Moreover, the EV maker posted better-than-expected auto delivery and production numbers for the month and quarter ending June 30, pushing shares up 6.9% on July 3.

***

Future Salaries Will Decrease?

Median incomes are projected to drop over the next few decades, falling by 0.43 percentage points per year between now and 2020, 0.52 points per year between 2020 and 2030, and 0.2 points per year between 2030 and 2040.

Although the figures on their own are not staggering, the percentage drops over time will add up significantly. By 2050, an employee who earned $50,000 in 2013 will only make $44,000. The number is even more noticeable after accounting for inflation.

Posted on March 24, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

Mass firings at tech companies continue as Accenture (NYSE:ACN) just announced plans to lay off around 19,000 people, or 2.5% of its current workforce, in the next 18 months. Over half of the departures will consist of people in non-billable corporate functions, the professional services firm said.

***

Despite strong gains early this week, antifungal drug developers lost steam even after Cidara Therapeutics (NASDAQ:CDTX) won FDA approval for its candidemia treatment Rezzayo. Shares of Cidara (CDTX) and its rival in antifungal space Scynexis (NASDAQ:SCYX) jumped amid concerns of a fast-spreading fungal infection caused by yeast species Candida auris in the U.S. New approval of Rezzayo for fungal disease candidemia and invasive candidiasis has failed to reignite the interest, with Cidara (CDTX) and Scynexis (SCYX) trading at least 20% lower. Meanwhile, Cidara (CDTX) has not replicated its regulatory success on the financial front, reporting lower-than-expected financials for Q4 2022 on Thursday.

***

The following is a round-up of today’s market activity:

The S&P 500® Index was up 11.75 (0.3%) at 3948.72; the Dow Jones industrial average was up 75.14 (0.2%) at 32,105.25; the NASDAQ Composite was up 117.44 (1.0%) at 11,787.40.

The 10-year Treasury yield was down about 11 basis points at 3.391%.

CBOE’s Volatility Index was up 0.35 at 22.61.

The energy sector led declines Thursday as crude oil futures fell back under $70 a barrel, with financials and consumer staples also losing ground. Technology and communications stocks managed to hold onto gains.

Finally, gold futures surged over 2% to a one-year high near $2,000 an ounce.

Posted on January 6, 2023 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

Here are eight things to keep in mind as you prepare to file your 2022 taxes

1. Income tax brackets shifted somewhat

There are still seven tax rates, but the income ranges (tax brackets) for each rate shifted slightly to account for inflation. For 2022, the following rates and income ranges apply:

Taxable income brackets

Tax rate

Single filers

Married couples filing jointly (and qualifying widows or widowers)

10%

$0 to $10,275

$0 to $20,550

12%

$10,276 to $41,775

$20,551 to $83,550

22%

$41,776 to $89,075

$83,551 to $178,150

24%

$89,076 to $170,050

$178,151 to $340,100

32%

$170,051 to $215,950

$340,101 to $431,900

35%

$215,951 to $539,900

$431,901 to $647,850

37%

$539,901 or more

$647,851 or more

2. The standard deduction increased somewhat

After an inflation adjustment, the 2022 standard deduction increases to $12,950 for single filers and married couples filing separately and to $19,400 for single heads of household, who are generally unmarried with one or more dependents. For married couples filing jointly, the standard deduction rises to $25,900.

3. Itemized deductions remain essentially the same

For most filers, taking the higher standard deduction is more practical and saves the hassle of keeping track of receipts. But if you have enough tax-deductible expenses, you might benefit from itemizing.

State and local taxes: The deduction for state and local income taxes, property taxes, and real estate taxes is capped at $10,000.

Mortgage interest deduction: The mortgage interest deduction is limited to $750,000 of indebtedness. But people who had $1,000,000 of home mortgage debt before December 16, 2017 will still be able to deduct the interest on that loan.

Medical expenses: Only medical expenses that exceed 7.5% of adjusted gross income (AGI) can be deducted in 2022.

Charitable donations: The deductions for charitable donations are not as generous as they were in 2021. In 2022, the annual income tax deduction limits for gifts to public charities1 are 30% of AGI for contributions of non-cash assets—if held for more than one year—and 60% of AGI for contributions of cash.

Miscellaneous deductions: No miscellaneous itemized deductions are allowed.

4. IRA contribution limits remain the same and 401(k) limits are slightly higher

The traditional IRA and Roth contribution limits in 2022 remain the same as the prior year. Individuals can contribute up to $6,000 to an IRA, and those age 50 and older also qualify to make an additional $1,000 catch-up contribution. If you’re able to max out your IRA, consider doing so—you may qualify to deduct some or all of your contribution.

However, the 2022 contribution limits for 401(k) accounts have increased to $20,500. If you’re age 50 or older, you qualify to make an additional $6,500 catch-up contribution for this tax year as well.

5. You can save a bit more in your health savings account (HSA)

For 2022, the maximum you can contribute to an HSA is $3,650 for an individual (up $50 from 2021) and $7,300 for a family (up $100). People age 55 and older can contribute an extra $1,000 catch-up contribution.

To be eligible for an HSA, you must be enrolled in a high-deductible health plan (which usually has lower premiums as well). Learn more about the benefits of an HSA.

6. The Child Tax Credit is lower after a one-year bump

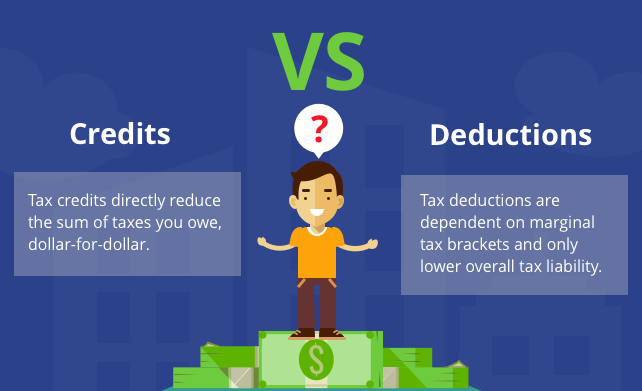

Tax credits, which reduce the tax you owe dollar for dollar, are normally better than deductions, which reduce how much of your income is subject to tax.

In 2021, the American Rescue Plan Act (ARPA) temporarily enlarged the Child Tax Credit. But in 2022, the credit returns to $2,000 per child age sixteen or younger. The credit is also subject to a phase-out starting at $400,000 for joint filers and $200,000 for single filers. For other qualified dependents, you can claim a $500 credit.

7. The alternative minimum tax (AMT) exemption is higher

Until the AMT exemption enacted by the Tax Cuts and Jobs Act expires in 2025, the AMT will continue to affect mostly households with incomes over $500,000. For 2022, the AMT exemptions are $75,900 for single filers and $118,100 for married taxpayers filing jointly. The phase-out thresholds are $1,079,800 for married taxpayers filing a joint return and $539,900 for all other taxpayers. (Once your income for the AMT hits the phase-out threshold, your AMT exemption begins to phase out at 25 cents for every dollar over the threshold.)

8. The estate tax exemption is even higher

The estate and gift tax exemption, which is indexed to inflation, rises to $12.06 million for 2022. But the now-higher exemption is set to expire at the end of 2025, meaning it could be essentially cut in half at that time if Congress doesn’t act.

The annual gift exclusion, which allows you to give money to your loved ones each year without incurring any tax liability or using up any of your lifetime estate and gift tax exemption, increases to $16,000 per recipient (up $1,000 from 2021).

Don’t get caught

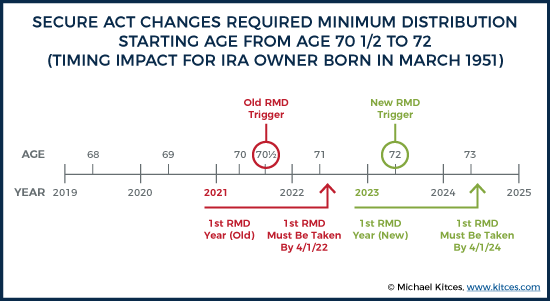

Finally, if you’re age 72 or older, make sure you’ve taken your required minimum distribution (RMD) from your retirement accounts before the end of the year or else you face a 50% penalty on any undistributed funds (unless it’s your first RMD, in which case you can wait until April 1, 2023).

A Required Minimum Distribution (RMD) is an amount of money the IRS requires you to withdraw from most retirement accounts, beginning at age 72. Due to the Coronavirus Aid, Relief, and Economic Security (CARES) Act, RMDs were not required in 2020, but RMDs are required in 2021 and each year after. RMDs can be an important part of your retirement income strategy.

Posted on November 13, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

IRS

The IRS just noted that there are no changes made to the taxability of income but only in the reporting rules for Form 1099-K. Taxpayers are still required to report all income on their tax return unless it is excluded by law. This is whether they receive a Form 1099-NEC, Nonemployee Compensation; Form 1099-K; or any other information return.

Previously businesses would generally receive a 1099-K tax form only when their gross payments exceeded $20,000 for the year and the business conducted at least 200 transactions.

According to the new 1099-K rule, the gross payments threshold has been lowered to just over $600 for the year with the transactions threshold no longer applying. Now a single transaction exceeding $600 can trigger a 1099-K. This includes transactions through credit cards, debit cards, banks, PayPal, Uber, Lyft, and other third-party payment settlement entities.

The 1099-K form includes information about the payment processor and the company receiving payments, and a monthly breakdown of total payments, among other information.

According to the IRS, the lower information reporting threshold and the summary of income on Form 1099-K will make it easier for taxpayers to track the amounts received.

Posted on November 6, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

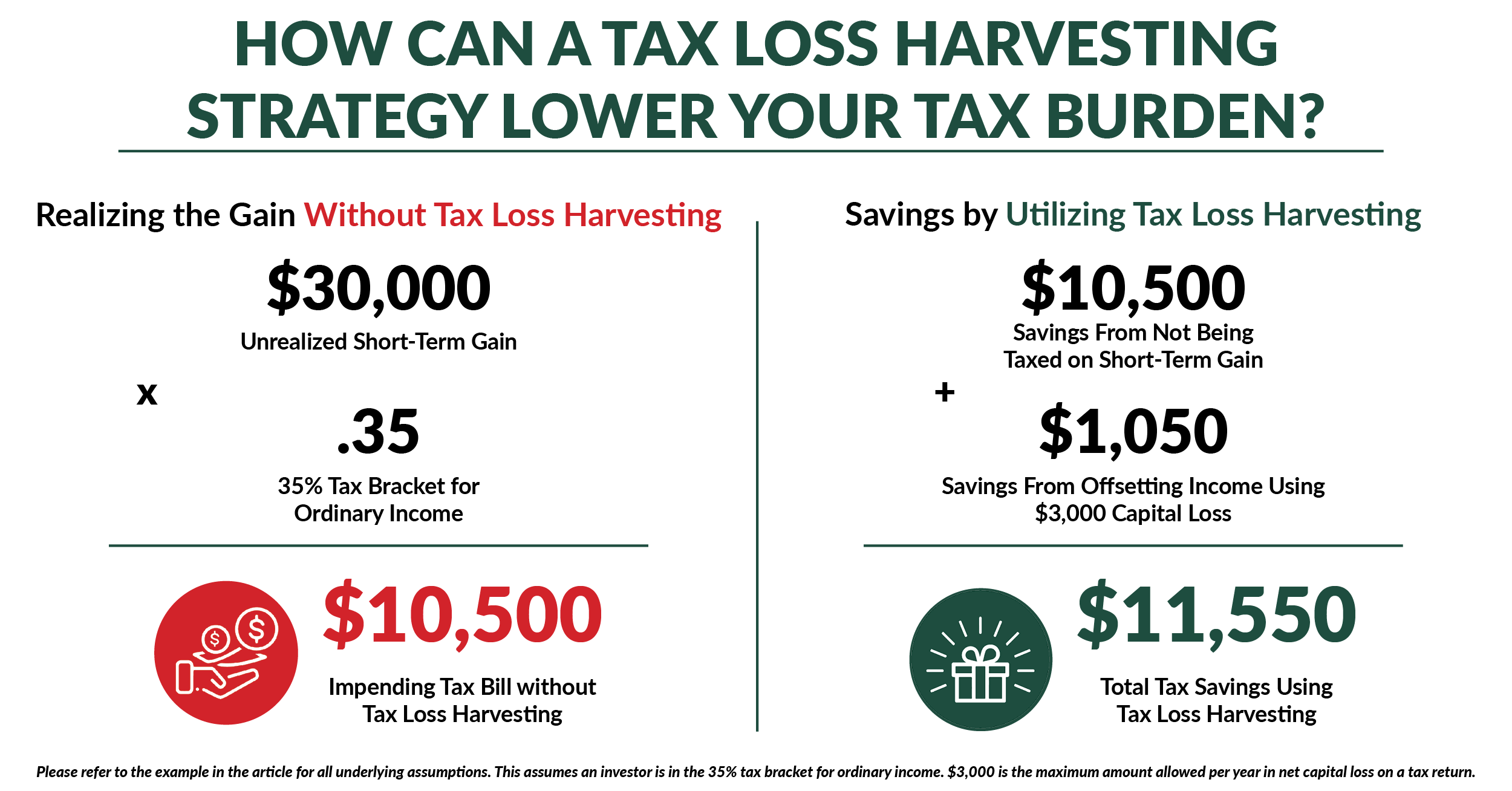

What Is Tax-Loss Harvesting?

Tax-loss harvesting is the timely selling of securities at a loss in order to offset the amount of capital gains tax due on the sale of other securities at a profit.

This strategy is most often used to limit the amount of taxes due on short-term capital gains, which are generally taxed at a higher rate than long-term capital gains. However, the method may also offset long-term capital gains. This strategy can help preserve the value of the investor’s portfolio while reducing the cost of capital gains taxes.

There is a $3,000 limit on the amount of capital gains losses that a federal taxpayer can deduct in a single tax year. However, Internal Revenue Service (IRS) rules allow additional losses to be carried forward into the following tax years.

4 Key Points

Tax-loss harvesting is a strategy investors can use to reduce the total amount of capital gains taxes due from the sale of profitable investments.

The strategy involves selling an asset or security at a net loss.

The investor can then use the proceeds to purchase a similar asset or security, maintaining the portfolio’s overall balance.

The investor must be careful not to violate the IRS rule against buying a “substantially identical” investment within 30 days.

Posted on April 15, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

***

TRIVIA QUESTION: What date has never been known as Tax Day?

A. March 1st B. March 15th C. April 15th D. May 1st

ANSWER: D—May 1st.

After the 16th Amendment cleared the way for the modern version of the federal income tax, the first filing deadline fell on March 1, 1913. Congress shifted Tax Day to March 15 after passing the Revenue Act of 1918, which introduced a progressive income tax structure to increase revenue during World War I. Since 1954, Tax Day for most Americans has been April 15 (or the next business day if the 15th falls on a weekend or holiday).

Posted on April 10, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

***

What is a tax deduction?

A deduction reduces the amount of income you pay taxes on, which means you could pay less in taxes. You subtract deductions from your income before calculating how much taxes you owe. How much a deduction saves you depends on your income tax bracket.

To calculate how much a deduction could reduce your taxes, you multiply the amount of the deduction by your marginal tax rate. For example, if a deduction is worth $5,000 and you are in the 10% tax bracket (the lowest), the deduction would reduce your taxes by $500.

A deduction’s value to you is tied to your tax rate. So if you’re paying a higher tax rate, you can reap more of a deduction’s benefit. The lower your tax rate, the less benefit a deduction will have for you. Imagine that you take a $5,000 deduction, but you’re in the 35% tax bracket — the second highest. Now you’re saving $1,750 in taxes.

On the other hand, a credit is a dollar-for-dollar reduction in the amount of tax you owe. For example, if you qualify for a $1,000 tax credit of some kind and owe $5,000 in taxes, that credit will reduce your tax burden to $4,000.

***

But – Do Not Claim Too Many Tax Deductions

Deductions are enticing to taxpayers because they can reduce the amount of your income before you calculate the tax you owe, which in turn might significantly lower how much you have to pay in taxes or increase your refund. But that doesn’t mean you should go wild writing things off on your tax returns, as experts say claiming too many deductions is the most common reason people end up getting audited by the IRS.

Don’t try writing off deductions that are no longer accepted by the IRS. The tax code has changed over the years, and there are some things the tax agency no longer recognizes. You should remember that some of the tax write-offs were terminated by the IRS, including deductions on alimony, moving expenses, and any expenses related to investing, hobbies, and tax preparation.

Posted on March 16, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

****

The IRS considers taxpayers married if they are legally married under state law, live together in a state-recognized common-law marriage, or are separated but have no separation maintenance or final divorce decree as of the end of the tax year.

Of the 150.3 million tax returns filed in 2016, the latest year for which the IRS has published statistics, 3.07 million belonged to twosomes who filed separately.

These partners reported individual income and expenses on individual tax returns.

By filing separately, their similar incomes, miscellaneous deductions or medical expenses likely helped them save taxes.

***

Filing separately with similar incomes

A couple may pay the IRS less by filing separately when both physician spouses work and earn about the same amount.

When they compare the tax due amount under both joint and separate filing statuses, they may discover that combining their earnings puts them into a higher tax bracket.

Their savings depends on a variety of other factors, however, including their investment situation and whether they have children.

The “married filing separately” status cuts the deductions for IRA contributions and eliminates certain tax credits, among other tax breaks.

Using miscellaneous deductions by filing separately (for tax years prior to 2018)

Miscellaneous deductions can lower taxable income, but in order to enter them on Schedule A, they must add up to more than 2% of adjusted gross income (AGI).

Physician or other spouses with union dues, job-search costs, tax-preparation fees and un-reimbursed business expenses may find their miscellaneous deductions don’t qualify when their higher combined income raises their AGI.

A spouse who travel frequently for business could rack up a sizable tally in airline fees for baggage and itinerary changes that makes the miscellaneous deduction worth pursuing.

Beginning in 2018, these types of miscellaneous expenses are no longer deductible.

Filing separately to save with unforeseen expenses

Unless out-of-pocket medical expenses exceed 7.5% of AGI for 2021, they don’t qualify as a deduction.

Casualty losses must also total more than 10% of AGI and occur in a federally declared disaster area.

The spouse with the loss or substantial medical outlay calculates deductibility against his or her own lower AGI when the couple files separate returns. When one spouse can lower taxable income this way, married filing separately might trim a couple’s overall tax burden.

Filing separately to guard the future

When you don’t want to be liable for your partner’s tax bill, choosing the married-filing-separately status offers financial protection: the IRS won’t apply your refund to your spouse’s balance due. Separate returns make sense to prevent the IRS from seizing a spouse’s tax refund when the other has fallen behind on child support payments.

Couples in the process of divorcing may shun joint returns to avoid post-divorce complications with the IRS, while a spouse who questions her partner’s tax ethics may feel more comfortable living a separate tax life.

Couples living in community-property states should consider state law when deciding how to file.

Devaluation is the deliberate downward adjustment of the value of a country’s money related to another currency, group of currencies or currency standard. It is often confused with depreciation and is the opposite of revaluation which refers to the readjustment of a currency exchange rate.

The government of a country may decide to devalue its currency and like depreciation it is not the result of non-governmental activities.

One reason a country made devalue its currency is to combat a trade imbalance. Devaluation reduces the cost of a country’s export rendering them more competitive in the Global market which is which in turn increases the cost of imports.

If imports are more expensive domestic consumers are less likely to purchase them further strengthening domestic businesses because exports increase and imports decrease there is typically a better balance of payments because the trade deficit shrinks. In short a country that devalue its currency can produce is difficult because there is a greater demand for cheaper exports.

***

***

In accountancy, depreciation refers to two aspects of the same concept: first, the actual decrease of fair value of an asset, such as the decrease in value of factory equipment each year as it is used and wear, and second, the allocation in accounting statements of the original cost of the assets to periods in which the assets are used (depreciation with the matching principle).

Depreciation is thus the decrease in the value of assets and the method used to reallocate, or “write down” the cost of a tangible asset (such as equipment) over its useful life span. Businesses depreciate long-term assets for both accounting and tax purposes. The decrease in value of the asset affects the balance sheet of a business or entity, and the method of depreciating the asset, accounting-wise, affects the net income, and thus the income statement that they report.

Posted on February 17, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

****

Alternative Minimum Tax

DEFINITION: The alternative minimum tax (AMT) is a tax imposed by the United States federal government in addition to the regular income tax for certain individuals, estates, and trusts. As of tax year 2018, the AMT raises about $5.2 billion, or 0.4% of all federal income tax revenue, affecting 0.1% of taxpayers, mostly in the upper income ranges.

Posted on February 1, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

****

***

Tax planning can be quite a tedious process, but there are benefits for all seniors to make it less taxing. And senor medical professionals should take particular note:

Free Advice: IRS-certified volunteers will help older taxpayers with tax return preparation and electronic filing between January 1st and April 15th each year.

No Withdrawal Penalties: Anyone aged 59 years or over can withdraw money from an IRA, without incurring the common 10% tax.

Catch-Up Contributions: Healthcare Workers aged 50 or older can defer income tax on an extra $6,500 or a total of $26,000 if contributed to a 401(k) plan, resulting in a tax savings of $6,240 for an older worker in the 24% tax bracket.

Additional IRA Contribution: Workers age 50 and older can contribute an additional $1,000 to an IRA, or a total of $7,000 in 2020.

Whether you do contract work or have your own small business, tax deductions for the self-employed physician consultant and/or medical executive or nurse consultant, etc., can add up to substantial tax savings.

With self-employment comes freedom, responsibility, and a lot of expense. While most self-employed people celebrate the first two, they cringe at the latter, especially at tax time. They might not be aware of some of the tax write-offs to which they are entitled.

When it comes time to file your returns, don’t hesitate to claim the benefits you get for being the boss. As a self-employed success story, you’ve earned them.

FORM 1099NEC: Form 1099 NEC is one of several IRS tax forms used in the United States to prepare and file an information return to report various types of income other than wages, salaries, and tips. The term information return is used in contrast to the term tax return although the latter term is sometimes used colloquially to describe both kinds of returns.

“Many times an overlooked deduction is educational expenses. If one is taking courses or buying research material to be more effective in their work, this can be deductible.”

Individual Retirement Plans (IRAs)

One of the best tax write-offs for the self-employed physician consultant is a retirement plan. A person with no employees can set up an individual 401 (k). “You can contribute $19,500 in 2021 as a 401(k) deferral, plus 25 percent of net income.”

If you have employees, consider a SIMPLE (Savings Incentive Match Plan for Employees) IRA—an IRA-based plan that gives small employers a simplified method to make contributions to their employees’ retirement. As of 2021, an employee may defer up to $13,500 and employees over 50 may contribute an additional $3,000.

“A third retirement plan is Simplified Employee Pension IRA (SEP IRA).” The employer may contribute the lesser of 25 percent of income or $58,000 in 2021. If the employer has eligible employees, an equal percentage of their income must be contributed.

Recall that retirement plans are “absolutely the No. 1 tax deduction. The government is helping fund retirement.”

Business use of home or dwelling

Now, most self-employed taxpayers’ businesses start as home-based businesses. These people need to know portions of business costs are deductible and so “It is very important that you keep track of expenses relating to your housing costs.”

If your gross income from your business exceeds your total expenses, then you can deduct all of your expenses related to the business use of your home. If your gross income is less than your total expenses, your deduction will be limited to the difference between your gross income and the sum of all business expenses you would pay if the business was not in your home. Those expenses could include telephone lines, the Internet, and other costs to do business.

You must also have a home office that is truly used for work and the Internal Revenue Service may require you to document this.

***

Deducting automobile expenses

If you travel for business, even short distances within your own city, you may deduct the dollar value of business miles traveled on your tax return. The taxpayer may file the actual expense s/he incurred, or use the standard mileage rate prescribed by the IRS, which is 56 cents as of 2021. The IRS allowable mileage rates should be checked every year as they can change.

“If you decide to use actual car expenses, be sure to include payments, depreciation, registration, insurance, garage rent, licenses, repairs and maintenance, and parking and toll fees.” AND, “If you decide to use the standard mileage rate, it would be in your best interest to keep a log—daily, weekly or monthly—of miles driven to distinguish personal use from business use.”

Depreciation of property and equipment

Some self-employed people may purchase property and equipment for a business. If they expect that property to last longer than one year, it should be depreciated on the tax return.

Claims regarding property, according to the IRS, must meet the following criteria: You must own the property and it must be used or held to generate income. The property should have an estimated useful life, meaning you should be able to guess how long you can generate income with it. It may not have a useful life of one year or less, and may not be purchased and disposed of in the same year.

Certain repairs on property used for business may also be deducted.

Educational expenses

Any educational expense is potentially tax-deductible.

“Many times an overlooked deduction is educational expenses. “If one is taking courses or buying research material to be more effective in their work, this can be deductible.”

Think about any books, web courses, local college courses, or other classes or materials that you have purchased to improve your job or business. It’s easy to forget a work-related webinar or business e-book that was purchased online, so remember to save e-receipts.

Also recall that subscriptions to trade or professional publications and donations to business organizations, both of which are frequently necessary for the continuation and growth of your business.

Other areas to explore

Other deductions that can be easily missed are advertising and promotional expenses, banking fees, and air, bus, or train fare. Restaurant meals and other entertainment costs may be written off as long as they are necessary business expenses.

And, consider health insurance premiums, which in most cases represent a credit rather than a tax deduction. “A credit goes directly against one’s taxes, rather than a reduction of income.”

Regardless of which expenses you discover that you may write off, the most important thing is to keep accurate records throughout the year. Save receipts, including e-mail receipts, and file or log them so you have easy access to them at tax time. Not only does keeping receipts, mileage logs, and other expense records make filing taxes easier, but it also facilitates a system that allows you to track changes from year to year.

***

Long-term tax-saving strategies

Don’t just look at last-minute write-offs when considering self-employment tax deductions. Think about laying down some long-term strategies for money savings from year to year—particularly if you are a high earner.

“Accountants typically tell you what you have to pay but they don’t always tell you strategies to reduce your payments.”

To reduce your gross taxable income, consider setting up a defined-benefit pension plan. This plan is based on your age and income: The older you are and the higher your earnings, the more you are allowed to contribute. An alternative plan is an age-weighted profit-sharing plan, which is similar and can benefit those who have several employees.

Another strategy for high-earning business owners who own their own building through a limited liability company or similar business structure is to pay themselves rent. This rent is used to pay down the mortgage, but it is also considered a business expense for tax purposes.

Self-employed professionals required to have liability insurance should consider setting up their own insurance company. A captive insurance company is one that insures the risks of the business—or businesses, in the case of a cooperative. Its premiums can be tax-deductible.

But, if money accumulates and claims are minimal, the money taken out is taxable under capital gains. This is not a retirement strategy, but that it can save you money by allowing you to “pay yourself” instead of an insurance company and still deduct the premiums.

Assessment

With any of these more complicated, long-term strategies, consult with a business attorney, CPA/EA or financial planner to ensure you have the best plan possible for your business.

Posted on January 24, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

Stock Markets: The S&P is off to its worst start to a year since 2016. The NASDAQ is in a correction. And the week ahead features a busy earnings slate and a Federal Reserve meeting.

CovisPandemic: Tony Dr. Fauci said he is “confident as you can be” that the Omicron wave in the US will peak by mid-February. In a growing number of states, that peak has already come and gone and cases are plunging in states like New York and Florida. Other states, such as Oklahoma, Idaho, and Wyoming, are still reporting an uptick in new Covid cases.

Crypto-Currency: Crypto investors, meanwhile, wish they got the weekend off like stock traders, because bitcoin, ethereum, and other digital tokens continued to sink.

Federal Reserve: Federal Reserve officials will get together on Tuesday and Wednesday against the backdrop of quaking markets. Investors will want to hear an update on Chair Jerome Powell’s views on inflation. This Fed meeting will likely be the last before an anticipated interest rate hike in March. And, a blizzard of companies will report including nearly half of the Dow’s 30 giants (American Express, 3M, IBM, and more) and tech heavyweights such as Apple, Microsoft, and Tesla.

Tax Season: The income tax filing season opens today and government officials warn it could be bumpy due to a depleted IRS. The Treasury says to file early, file online, and request your refund via direct deposit to avoid the severe headaches.

Here are eight things to keep in mind as you prepare to file your 2021 taxes.

1. Income tax brackets have shifted a bit

There are still seven tax rates, but the income ranges (tax brackets) for each rate have shifted slightly to account for inflation. For 2021, the following rates and income ranges apply:

Tax rate

Taxable income brackets:Single filers

Taxable income brackets:Married couples filing jointly (and qualifying widows or widowers)

10%

$0 to $9,950

$0 to $19,900

12%

$9,951 to $40,525

$19,901 to $81,050

22%

$40,526 to $86,375

$81,051 to $172,750

24%

$86,376 to $164,925

$172,751 to $329,850

32%

$164,926 to $209,425

$329,851 to $418,850

35%

$209,426 to $523,600

$418,851 to $628,300

37%

$523,601 or more

$628,301 or more

Source: Internal Revenue Service

2. The standard deduction has increased slightly

After an inflation adjustment, the 2021 standard deduction has increased slightly to $12,550 for single filers and married couples filing separately and $18,800 for single heads of household, who are generally unmarried with one or more dependents. For married couples filing jointly, the standard deduction has risen to $25,100.

3. Itemized deductions remain the same

For most filers, taking the higher standard deduction is more practical and saves the hassle of keeping track of receipts. But if you have enough tax-deductible expenses, you might benefit from itemizing.

The following rules for itemized deductions haven’t changed much for 2021, but they’re still worth pointing out.

State and local taxes: The deduction for state and local income taxes, property taxes, and real estate taxes is capped at $10,000.

Mortgage interest deduction: The mortgage interest deduction is limited to $750,000 of indebtedness. But people who had $1,000,000 of home mortgage debt before December 16, 2017, will still be able to deduct the interest on that loan.

Medical expenses: Only medical expenses that exceed 7.5% of adjusted gross income (AGI) can be deducted in 2021.

Charitable donations: The cash donation limit of 100% of AGI remains in place for 2021, if donations were made to operating charities.1

Miscellaneous deductions: No miscellaneous itemized deductions are allowed.

4. IRA and 401(k) contribution limits remain the same

The traditional IRA and Roth contribution limits in 2021 remain the same as in 2020. Individuals can contribute up to $6,000 to an IRA, and those age 50 and older also qualify to make an additional $1,000 catch-up contribution. If you’re able to max out your IRA, consider doing so—you may qualify to deduct some or all of your contribution.

The 2021 contribution limit for 401(k) accounts also stays at $19,500. If you’re age 50 or older, you qualify to make an additional $6,500 catch-up contribution as well.

5. You can save a bit more in your health savings account (HSA)

For 2021, the max you can contribute into an HSA is $3,600 for an individual (up $50 from 2020) and $7,200 for a family (up $100). People age 55 and older can contribute an extra $1,000 catch-up contribution.

To be eligible for an HSA, you must be enrolled in a high-deductible health plan (which usually has lower premiums as well). Learn more about the benefits of an HSA.

6. The Child Tax Credit has been expanded

For 2021, the American Rescue Plan Act (ARPA) has temporarily modified the Child Tax Credit requirements and amounts for household incomes below $75,000 for single filers and $150,000 for married filing jointly.

First, the ARPA has raised the age limit for dependents from 16 to 17. In addition, the child tax credit has increased from $2,000 to $3,000 for children age 6 through 17 and up to $3,600 for children under 6. If your income exceeded the above limits but was below $200,000 for single filers or $400,000 for joint filers, you’ll receive the standard child tax credit of $2,000 per child.

The IRS began sending monthly advance Child Tax Credit payments to eligible families in July and sent its last advance in December. If your dependent didn’t qualify for the child tax credit, you may still qualify for up to $500 of tax credits under the “credit for other dependents” (see IRS Publication 972 for more details). Tax credits, which reduce the tax you owe dollar for dollar, are generally better than deductions, which reduce your taxable income.

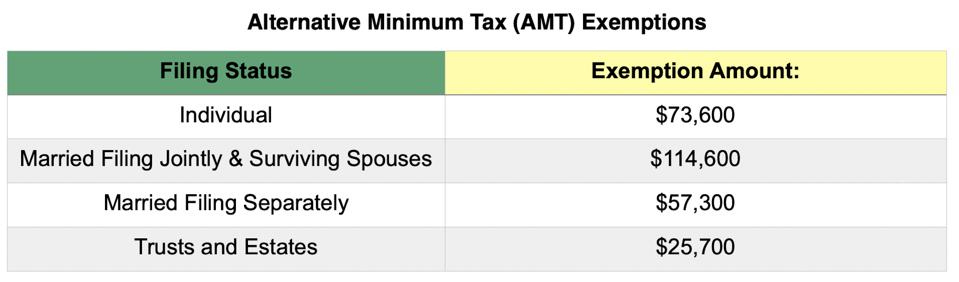

7. The alternative minimum tax (AMT) exemption has gone up

Until the AMT exemption enacted by the Tax Cuts and Jobs Act expires in 2025, the AMT will continue to affect mostly households with incomes over $500,000. Still, the AMT has investment implications for some high earners.

For 2021, the AMT exemptions are $73,600 for single filers and $114,600 for married taxpayers filing jointly. The phase-out thresholds are $1,047,200 for married taxpayers filing a joint return and $523,600 for all other taxpayers.

8. The estate tax exemption is even higher

The estate and gift tax exemption, which is indexed to inflation, has risen to $11.7 million for 2021. But the now-higher exemption is set to expire at the end of 2025, meaning it could be essentially cut in half at that time if Congress doesn’t act.

The annual gift exclusion, which allows you to give money to your loved ones each year without incurring any tax liability or using up any of your lifetime estate and gift tax exemption, stays at $15,000 per recipient.

Don’t get caught off guard

As you prepare to file your taxes for 2021, here are a few additional items to consider.

If you’re not retired, the 10% early withdrawal penalty that was waived for retirement account distributions in 2020 has been reinstated for 2021.

If you’re age 72 or older, make sure you’ve taken your required minimum distribution (RMD) from your retirement accounts or else you face a 50% penalty on any undistributed funds (unless it’s your first RMD, in which case, you can wait until April 1, 2022).

If you haven’t contributed to your retirement accounts already, now is the time. Review your earnings for the year and take advantage of any deductions that can lower your tax bill. Also, keep an eye on Washington for any last-minute tax changes that could affect your return before you file. Tax season will be here before you know it, and it’s never too early to start preparing.

1Operating charities, or qualifying public charities, are defined by Internal Revenue Code section 170(b)(1)(A). You can use the Tax Exempt Organization Search tool on IRS.gov to check an organization’s eligibility.

Posted on January 4, 2022 by Dr. David Edward Marcinko MBA MEd CMP™

By Staff Reporters

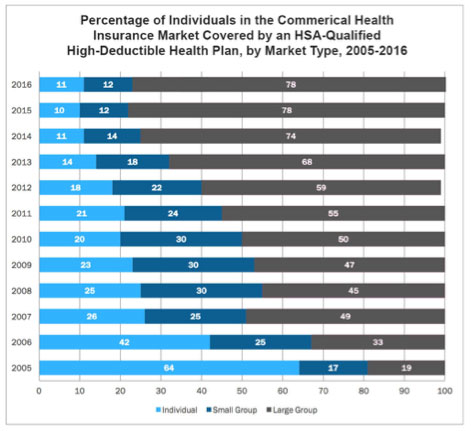

In the United States, a high-deductible health plan is a health insurance plan with lower premiums and higher deductibles than a traditional health plan. It is intended to incentivize consumer-driven healthcare. Being covered by an HDHP is also a requirement for having a health savings account. Some HDHP plans also offer additional “wellness” benefits, provided before a deductible is paid.

High-deductible health plans are a form of catastrophic coverage, intended to cover for catastrophic illnesses. Adoption rates of HDHPs have been growing since their inception in 2004, not only with increasing employer options, but also increasing government options. As of 2016, HDHPs represented 29% of the total covered workers in the United States; however, the impact of such benefit design is not widely understood.

***

% Covered Employees Enrolled in Account-Based CDHP’s

Almost everything you own and use for personal or investment purposes is a capital asset. Examples include a home, personal-use items like household furnishings, and stocks or bonds held as investments. When you sell a capital asset, the difference between the adjusted basis in the asset and the amount you realized from the sale is a capital gain or a capital loss.

Generally, an asset’s basis is its cost to the owner, but if you received the asset as a gift or inheritance, refer to Topic No. 703 for information about your basis.

For information on calculating adjusted basis, refer to Publication 551, Basis of Assets. You have a capital gain if you sell the asset for more than your adjusted basis. You have a capital loss if you sell the asset for less than your adjusted basis. Losses from the sale of personal-use property, such as your home or car, aren’t tax deductible.

Generally speaking, all income is taxable unless it’s specifically excluded, as is the case with certain gifts and inheritances. In most instances, the income you earn will be reported to both you and the government on an information return, such as a Form 1099 or W-2. If the income you report doesn’t match the IRS’s records, you could face problems down the road—so be sure you include the income from all of the following forms that are applicable to your situation:

1099-B: The form on which financial institutions report capital gains.

1099-DIV: The form on which financial institutions report dividends.

1099-MISC: The form used to report various types of income, such as royalties, rents, payments to independent contractors, and numerous other types of income.

1099-R:The form on which financial institutions report withdrawals from tax-advantaged retirement accounts.

Form 1099-INT: The form on which financial institutions report interest income.

Form SSA-1099:The form on which the Social Security Administration reports Social Security benefits (a portion of which may be taxable, depending on your level of income).

Form W-2:The form on which employers report total annual compensation, payroll taxes, contributions to retirement accounts, and other information.

If you receive an inaccurate statement of income, immediately contact the responsible party to request a corrected form and have them resend the documents to both you and the IRS as soon as possible to avoid delaying your tax return. Also, be aware that you must report income for which there is no form, such as renting out your vacation home.

When you sell an investment, you’ll need to know both the cost basis (what you paid for the investment) and the sale price to determine your net gain or loss. The cost basis of your investment may need to be adjusted to account for commissions, fees, stock splits, or other events, which could help reduce your taxable gain or increase your net loss.

Financial institutions are required to adjust your investments’ cost basis and provide that information on a Form 1099. However, brokerages aren’t required to report the cost basis for investments purchased prior to a certain date, which means you’ll be responsible for supplying that information (see the table below). Be sure to keep records of all investment purchases and sales—even those for which your brokerage is responsible.

Your reporting responsibility

Depending on security type and date of purchase, you—rather than your brokerage—could be responsible for reporting the cost basis of your investment to the IRS.

The housing market is HOT right now. Lumbar and wood is expensive. Inflation is emerging. So, owning a home can be very lucrative. Seriously, owning a home can not only give you a cheaper monthly payment than renting but in many cases, the tax benefits make the decision a no-brainer.

Here are a few of the larger deductions that you need to be sure to take:

Interest you pay on your mortgage: If you own a home and don’t have a mortgage greater than $750,000, you can deduct the interest you pay on the loan. This is one of the biggest benefits to owning a home versus renting–as you could get massive deductions at tax time. The limit used to be $1 million, but the Tax Cuts and Jobs Act of 2017 (TCJA) reduced the limit and made some clarifications on deducting interest from a home equity line of credit.

Property taxes: Another awesome benefit to owning a home is the ability to deduct your property taxes. Before TCJA, the rules were a little more flexible and you were able to deduct the entirety of your property taxes. Now things have a changed a bit. Under the new law, you can deduct up to $10,000. The deduction for state and local income taxes was combined with the deduction for state and local property taxes, too.

Tax incentives for energy-efficient upgrades: While most of the tax incentives for making energy-efficient upgrades to your home have gone away, there are still a couple worth noting. You can still claim tax deductions on solar energy–both for electric and water heating equipment, through 2021. The longer you wait, though, the less money you’ll get back. Here’s the percentage of equipment you can deduct, based on time of installation:

Between January 1, 2017, and December 31, 2019 – 30% of the expenditures are eligible for the credit Between January 1, 2020, and December 31, 2020 – 26% Between January 1, 2021, and December 31, 2021 – 22%

ASSESSMENT: But, is now the best time to buy a home? Your thoughts are appreciated.

Late on December 15th, a bipartisan agreement was reached on tax extenders—i.e., the 50 or so temporary tax provisions that are routinely extended by Congress on a one- or two-year basis—and numerous other tax provisions in the “Protecting Americans from Tax Hikes (PATH) Act of 2015” (the Act). This agreement makes permanent many of the individual and business extenders and contains provisions on Real Estate Investment Trusts (REITs), IRS administration and the Tax Courts and miscellaneous other provisions.

Below are some provisions that have been made permanent:

DEPRECIATION & EXPENSING PROVISIONS

The Act makes permanent the $500,000 expensing limitation and $2 million phase out amounts under Code Section 179

For property placed in service after Dec 31, 2015, the Act provides that air conditioning and heating units are now eligible for expensing

Assets for which the De Minimis election applies are not counted in determining the Code Section 179 expensing election or the ceiling

15 Year Write off for Qualified Leasehold , Retail Improvements & Restaurant Property

INDIVIDUALS

American Opportunity Credit

Enhanced Earned Income Tax Credit

Above the line Educator Expenses

Exclusion for Employer Provided Mass Transit & Parking

State and Local Sales deduction

Liberalized rules for Qualified Conservation Contributions

Nontaxable IRA transfers to eligible charities

BUSINESSES

Research & Development credit & offset now available against taxes in addition to income taxes

Reduction in S-Corporation recognition period for Built in Gains Tax

Exclusion of 100% Gain on certain small business stock

The above provides a brief overview of the Act. There are various provisions that have been extended through 2016 and 2019 and other miscellaneous provisions. If you need additional information or have questions, please contact your CPA.

***

***

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on June 23, 2015 by Dr. David Edward Marcinko MBA MEd CMP™

A SPECIAL ME-P REPORT

[The Ethical Pursuit of Tax Reduction and Avoidance]

[By Perry D’Alessio CPA]

The objective of tax planning is to arrive at the lowest overall tax cost on the activities performed. In as much as physicians constitute 14% of the so-called and maligned “one-percenters” [$388,905 earned-not passive income/year]; this essay will address some methods and strategies to reduce federal and state income taxes. It is applicable to all physicians and medical professionals; as independent practitioners or employees.

So, how much in income taxes do the wealthy pay? The top 10 percent of taxpayers paid over 70 percent of the total amount collected in federal income taxes in 2010, the latest year figures are available, according to the Tax Foundation, a think tank that advocates for lower taxes. That’s up from 55 percent in 1986. The remaining 90 percent bore just under 30 percent of the tax burden. And, 47 percent of all Americans pay hardly anything at all.

Realize, that’s just federal income tax and doesn’t include payroll tax for Social Security and Medicare (which the vast majority of people pay), plus state taxes and all of the other taxes we face. When you add them all together; using figures from the Tax Policy Center and the Institute on Taxation and Economic Policy. Earners in the top 1 percent pay about 43 percent of their incomes in tax. People in the middle quintile pay 25 percent while the poorest fifth pays 13 percent.

Finally, before you assume these one- and 10-percenters are living on luxury yachts and in million-dollar mansions, consider how little money it takes to be a top wage earner.

According to 2011 IRS data, the top 1 percent have adjusted gross incomes of $388,905 per year or more. To be in the top 10 percent, you need an adjusted gross income of just $120,136 or more. These are good incomes to be sure, but definitely not enough to be out work, or the medical office, for more than a few weeks each year.

***

***

Now consider the following more specifically:

42 percent of all federal tax revenue came from individual income taxes in 2010 and it has been the largest single source of revenue since 1950.

Individuals paid more than $2.2 trillion in 2010.

Bush-era tax cuts have finally expired, giving us the 20th century tax rates with the top income tax rate of 39.6%, we have not seen rates this high in almost 15 years.

39.6% tax rate kicks in at $400,000 for individual taxpayers and $450,000 for married couples filing jointly.

Taxpayers who make over $200,000 ($250,000 for married taxpayers) will be subject to the Medicare surtax. If that’s you, Medicare surtax will be tacked on to your wages, compensation, or self-employment income over that amount. The amount of the surcharge is .9%.

Net Investment Income Tax (NIIT) new as of 2013; if you have both net investment income and modified adjusted gross income (MAGI) of at least $200,000 for an individual taxpayer and $250,000 for taxpayers filing as married an additional 3.8 percent of the net investment income is an added tax.

ASSESMENT

So, where do you fall on this schematic, doctor?

Channel Surfing

Have you visited our other topic channels? Established to facilitate idea exchange and link our community together, the value of these topics is dependent upon your input. Please take a minute to visit. And, to prevent that annoying spam, we ask that you register.

Perry D’Alessio has twenty years’ experience in public accounting. He specializes in the taxation of closely held businesses and their owners, as well as high wealth individuals. He has a broad range of experience that includes individual, corporate, partnership, fiduciary, estate, and gift taxation. Business development has also been a focus. Particularly in the Healthcare and Fitness Industry, he worked with successful entities whose emphasis was on growth through development of strategic relationships and unit building. Mr. D’Alessio received his Bachelor of Business Administration degree in Accounting from Baruch College. He is a Certified Public Accountant in New York. He is a member of the American Institute of Certified Public Accountants (AICPA), the New York State Society of Certified Public Accountants (NYSSCPA). He served on several New York State Society tax committees including: PCAOB and HealthCare. Mr. D’Alessio presents at financial and medical associations throughout the region, and authored a book chapter in the “Financial Management Strategies for Hospitals and Healthcare Organizations” for the Institute of Medical Business Advisors, Inc.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on July 10, 2014 by Dr. David Edward Marcinko MBA MEd CMP™

On Entirely Legal AUTOMOBILE Employment Fringe Benefit Strategies

[By Perry Dalessio CPA]

When an employment fringe benefit does not qualify for exclusion under a specific statute or regulation, the benefit is considered taxable to the recipient. It is included in wages for withholding and employment-tax purposes, at the excess of its fair market value over any amount paid by the employee for the benefit.

Examples:

For example, hospitals often provide automobiles for use by employees. Treasury regulations exclude from income the value of the following types of vehicles’ use by an employee:

Vehicles not available for the personal use of an employee by reason of a written policy statement of the employer

Vehicles not available to an employee for personal use other than commuting (although in this case commuting is includable)

Vehicles used in connection with the business of farming [in which case the exclusion is equal to the value of an arbitrary 75% of the total availability for use, and the value of the balance may be includable or excludable, depending upon the facts (Treas. Regs. § 1.132-5(g)) involved)]

Certain vehicles identified in the regulations as “qualified non-personal-use vehicles,” which by reason of their design do not lend themselves to more than a de minimus amount of personal use by an employee [examples are ambulances and hearses].

Vehicles provided for qualified automobile demonstration use

Vehicles provided for product testing and evaluation by an employee outside the employer’s work place

If the employer-provided vehicle does not fall into one of the excluded categories, then the employee is required to report his personal use as a taxable benefit. The value of the availability for personal use may be determined under one of several approaches.

Assessment

Under any of the approaches, the after-tax cost to the employee is substantially less than if the employee used his or her own dollars to purchase the automobile and then deducted a portion of the cost as a business expense.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

For individuals, these year-end 2013 tax planning strategies include: the option to deduct state and local sales and use taxes instead of state and local income taxes; the above-the-line deduction for qualified higher education expenses; and tax-free distributions by those age 70-1/2 or older from IRAs for charitable purposes.

For businesses, tax breaks that are available through the end of this year but won’t be around next year unless Congress acts include: 50% bonus first-year depreciation for most new machinery, equipment and software; an extraordinarily high $500,000 expensing limitation; the research tax credit; and the 15-year writeoff for qualified leasehold improvements, qualified restaurant buildings and improvements and qualified retail improvements.

High-income-earners have other factors to keep in mind when mapping out year-end plans.

For the first time, they have to take into account the 3.8% tax surtax on unearned income and the additional 0.9% Medicare (hospital insurance, or HI) tax that applies to individuals receiving wages with respect to employment in excess of $200,000 ($250,000 for married couples filing jointly and $125,000 for married couples filing separately).

The surtax is 3.8% of the lesser of: (1) net investment income (NII), or (2) the excess of modified adjusted gross income (MAGI) over an unindexed threshold amount ($250,000 for joint filers or surviving spouses, $125,000 for a married individual filing a separate return, and $200,000 in any other case). As year-end nears, a taxpayer’s approach to minimizing or eliminating the 3.8% surtax will depend on his estimated MAGI and NII for the year. Some taxpayers should consider ways to minimize (e.g., through deferral) additional NII for the balance of the year, others should try to see if they can reduce MAGI other than unearned income, and others should consider ways to minimize both NII and other types of MAGI.

The additional Medicare tax may require year-end actions. Employers must withhold the additional Medicare tax from wages in excess of $200,000 regardless of filing status or other income. Self-employed persons must take it into account in figuring estimate tax. There could be situations where an employee may need to have more withheld toward year end to cover the tax.

For example, consider an individual who earns $200,000 from one employer during the first half of the year and a like amount from another employer during the balance of the year. He would owe the additional Medicare tax, but there would be no withholding by either employer for the additional Medicare tax since wages from each employer don’t exceed $200,000.

Also, in determining whether they may need to make adjustments to avoid a penalty for underpayment of estimated tax, individuals also should be mindful that the additional Medicare tax may be over-withheld. This could occur, for example, where only one of two married spouses works and reaches the threshold for the employer to withhold, but the couple’s income won’t be high enough to actually cause the tax to be owed

We have compiled a checklist of additional actions based on current tax rules that may help you save tax dollars if you act before year-end. Not all actions will apply in your particular situation, but you will likely benefit from many of them. We can narrow down the specific actions that you can take once we meet with you to tailor a particular plan.

In the meantime, please review the following list to help determine which tax-saving moves to make.

Year-End Tax Planning Moves for Individuals

Increase the amount you set aside for next year in your employer’s health flexible spending account (FSA) if you set aside too little for this year.

If you become eligible to make health savings account (HSA) contributions in December of this year, you can make a full year’s worth of deductible HSA contributions for 2013.

Realize losses on stock while substantially preserving your investment position. There are several ways this can be done. For example, you can sell the original holding, then buy back the same securities at least 31 days later. It may be advisable for us to meet to discuss year-end trades you should consider making.

Postpone income until 2014 and accelerate deductions into 2013 to lower your 2013 tax bill. This strategy may enable you to claim larger deductions, credits, and other tax breaks for 2013 that are phased out over varying levels of adjusted gross income (AGI). These include child tax credits, higher education tax credits, the above-the-line deduction for higher-education expenses, and deductions for student loan interest. Postponing income also is desirable for those taxpayers who anticipate being in a lower tax bracket next year due to changed financial circumstances. Note, however, that in some cases, it may pay to actually accelerate income into 2013. For example, this may be the case where a person’s marginal tax rate is much lower this year than it will be next year or where lower income in 2014 will result in a higher tax credit for an individual who plans to purchase health insurance on a health exchange and is eligible for a premium assistance credit.

If you believe a Roth IRA is better than a traditional IRA, and want to remain in the market for the long term, consider converting traditional-IRA money invested in beaten-down stocks (or mutual funds) into a Roth IRA if eligible to do so. Keep in mind, however, that such a conversion will increase your adjusted gross income for 2013.

If you converted assets in a traditional IRA to a Roth IRA earlier in the year, the assets in the Roth IRA account may have declined in value, and if you leave things as-is, you will wind up paying a higher tax than is necessary. You can back out of the transaction by recharacterizing the rollover or conversion, that is, by transferring the converted amount (plus earnings, or minus losses) from the Roth IRA back to a traditional IRA via a trustee-to-trustee transfer. You can later reconvert to a Roth IRA.

It may be advantageous to try to arrange with your employer to defer a bonus that may be coming your way until 2014.

Consider using a credit card to prepay expenses that can generate deductions for this year.

If you expect to owe state and local income taxes when you file your return next year, consider asking your employer to increase withholding of state and local taxes (or pay estimated tax payments of state and local taxes) before year-end to pull the deduction of those taxes into 2013 if doing so won’t create an alternative minimum tax (AMT) problem.

Take an eligible rollover distribution from a qualified retirement plan before the end of 2013 if you are facing a penalty for underpayment of estimated tax and the increased withholding option is unavailable or won’t sufficiently address the problem. Income tax will be withheld from the distribution and will be applied toward the taxes owed for 2013. You can then timely roll over the gross amount of the distribution, as increased by the amount of withheld tax, to a traditional IRA. No part of the distribution will be includible in income for 2013, but the withheld tax will be applied pro rata over the full 2013 tax year to reduce previous underpayments of estimated tax.

Estimate the effect of any year-end planning moves on the alternative minimum tax (AMT) for 2013, keeping in mind that many tax breaks allowed for purposes of calculating regular taxes are disallowed for AMT purposes. These include the deduction for state property taxes on your residence, state income taxes (or state sales tax if you elect this deduction option), miscellaneous itemized deductions, and personal exemption deductions. Other deductions, such as for medical expenses, are calculated in a more restrictive way for AMT purposes than for regular tax purposes in the case of a taxpayer who is over age 65 or whose spouse is over age 65 as of the close of the tax year. As a result, in some cases, deductions should not be accelerated.

Accelerate big ticket purchases into 2013 in order to assure a deduction for sales taxes on the purchases if you will elect to claim a state and local general sales tax deduction instead of a state and local income tax deduction. Unless Congress acts, this election won’t be available after 2013.

You may be able to save taxes this year and next by applying a bunching strategy to miscellaneous itemized deductions, medical expenses and other itemized deductions.

If you are a homeowner, make energy saving improvements to the residence, such as putting in extra insulation or installing energy saving windows, or an energy efficient heater or air conditioner. You may qualify for a tax credit if the assets are installed in your home before 2014.

Unless Congress extends it, the up-to-$4,000 above-the-line deduction for qualified higher education expenses will not be available after 2013. Thus, consider prepaying eligible expenses if doing so will increase your deduction for qualified higher education expenses. Generally, the deduction is allowed for qualified education expenses paid in 2013 in connection with enrollment at an institution of higher education during 2013 or for an academic period beginning in 2013 or in the first 3 months of 2014.

You may want to pay contested taxes to be able to deduct them this year while continuing to contest them next year.

You may want to settle an insurance or damage claim in order to maximize your casualty loss deduction this year.

Purchase qualified small business stock (QSBS) before the end of this year. There is no tax on gain from the sale of such stock if it is (1) purchased after September 27, 2010 and before January 1, 2014, and (2) held for more than five years. In addition, such sales won’t cause AMT preference problems. To qualify for these breaks, the stock must be issued by a regular (C) corporation with total gross assets of $50 million or less, and a number of other technical requirements must be met. Our office can fill you in on the details.

If you are age 70-1/2 or older, own IRAs and are thinking of making a charitable gift, consider arranging for the gift to be made directly by the IRA trustee. Such a transfer, if made before year-end, can achieve important tax savings.

Take required minimum distributions (RMDs) from your IRA or 401(k) plan (or other employer-sponsored retired plan) if you have reached age 70-1/2. Failure to take a required withdrawal can result in a penalty of 50% of the amount of the RMD not withdrawn. If you turned age 70-1/2 in 2013, you can delay the first required distribution to 2013, but if you do, you will have to take a double distribution in 2014 the amount required for 2013 plus the amount required for 2014. Think twice before delaying 2013 distributions to 2014 bunching income into 2014 might push you into a higher tax bracket or have a detrimental impact on various income tax deductions that are reduced at higher income levels. However, it could be beneficial to take both distributions in 2014 if you will be in a substantially lower bracket that year, for example, because you plan to retire late this year.

Make gifts sheltered by the annual gift tax exclusion before the end of the year and thereby save gift and estate taxes. You can give $14,000 in 2013 to each of an unlimited number of individuals but you can’t carry over unused exclusions from one year to the next. The transfers also may save family income taxes where income-earning property is given to family members in lower income tax brackets who are not subject to the kiddie tax.

Year-End Tax-Planning Moves for Businesses & Business Owners

Businesses should consider making expenditures that qualify for the business property expensing option. For tax years beginning in 2013, the expensing limit is $500,000 and the investment ceiling limit is $2,000,000. And a limited amount of expensing may be claimed for qualified real property. However, unless Congress changes the rules, for tax years beginning in 2014, the dollar limit will drop to $25,000, the beginning-of-phaseout amount will drop to $200,000, and expensing won’t be available for qualified real property. The generous dollar ceilings that apply this year mean that many small and medium sized businesses that make timely purchases will be able to currently deduct most if not all their outlays for machinery and equipment. What’s more, the expensing deduction is not prorated for the time that the asset is in service during the year. This opens up significant year-end planning opportunities.

Businesses also should consider making expenditures that qualify for 50% bonus first year depreciation if bought and placed in service this year. This bonus writeoff generally won’t be available next year unless Congress acts to extend it. Thus, enterprises planning to purchase new depreciable property this year or the next should try to accelerate their buying plans, if doing so makes sound business sense.

Nail down a work opportunity tax credit (WOTC) by hiring qualifying workers (such as certain veterans) before the end of 2013. Under current law, the WOTC won’t be available for workers hired after this year.

Make qualified research expenses before the end of 2013 to claim a research credit, which won’t be available for post-2013 expenditures unless Congress extends the credit.

If you are self-employed and haven’t done so yet, set up a self-employed retirement plan.

Depending on your particular situation, you may also want to consider deferring a debt-cancellation event until 2014, and disposing of a passive activity to allow you to deduct suspended losses.

If you own an interest in a partnership or S corporation you may need to increase your basis in the entity so you can deduct a loss from it for this year.

Assessment

These are just some of the year-end steps that can be taken to save taxes.

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Posted on November 4, 2012 by Dr. David Edward Marcinko MBA MEd CMP™

A Brief Audio Teaser

By @PhilBumann – #AcctgChat

Accountants are an important part of healthcare organizations and economies. Whether they work in private practice, corporate enterprise or government, accounts do have vital perspectives and understandings of the language of business.

The Accounting profession has been slow to adopt social and other digital software, but there are value propositions that these financial professionals ought to consider.

This SoundCloud is a brief tease of why accountants should intelligently consider the use of social media to further their professional development, find and strengthen connections, and even market (in a human way) their services.

Assessment

Not the sexiest topic, but even accountants can get something out of social media. The hashtag that has been around for years is #AcctgChat. Tell your accountant friends.

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com and http://www.springerpub.com/Search/marcinko

Posted on March 21, 2010 by Dr. David Edward Marcinko MBA MEd CMP™

Repo 105 and Why Auditors Have Some “Splainen to Do”

[By Staff Reporters]

According to ProPublica on March 16, 2010 on 9:07 am EDT, a post-mortem report on Lehman Brothers revealed a shady accounting maneuver through which the bank hid its financial troubles for nearly a decade.

Pleading Ignorance

In this repot, Marian Wang takes a closer look at the parties pleading ignorance and the auditors who admit they knew, but insist they did no wrong.

And so, your thoughts and comments on this ME-Pare appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, be sure to subscribe to the ME-P. It is fast, free and secure.

Subscribe Now: Did you like this Medical Executive-Post, or find it helpful, interesting and informative? Want to get the latest ME-Ps delivered to your email box each morning? Just subscribe using the link below. You can unsubscribe at any time. Security is assured.

Posted on August 25, 2009 by Dr. David Edward Marcinko MBA MEd CMP™

Summer 2009

By Linda B. Trugman; CPA, MBA