Stabilization, not stagnation [Expect modest returns]

By The Vanguard Group

2017 Economic and market outlook

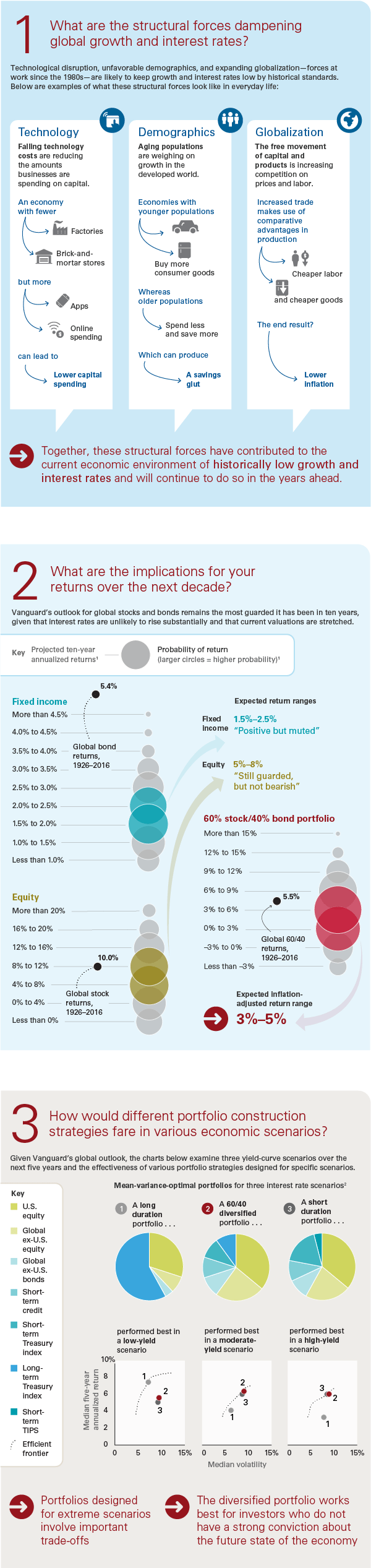

We’ve seen only a modest global recovery—at times frustratingly fragile—since the global financial crisis.

In the United States, for example, the economy has grown at an average annual rate of about 2.00%, whereas growth since 1950 has averaged an annual rate of 3.25%. Based on market and economic conditions, our outlook for the equity and fixed income markets is the most guarded it has been in ten years.

***

***

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

- PRACTICES: www.BusinessofMedicalPractice.com

- HOSPITALS: http://www.crcpress.com/product/isbn/9781466558731

- CLINICS: http://www.crcpress.com/product/isbn/9781439879900

- ADVISORS: www.CertifiedMedicalPlanner.org

- FINANCE: Financial Planning for Physicians and Advisors

- INSURANCE: Risk Management and Insurance Strategies for Physicians and Advisors

- Dictionary of Health Economics and Finance

- Dictionary of Health Information Technology and Security

- Dictionary of Health Insurance and Managed Care

***

Share this:

Filed under: iMBA, Inc. | Tagged: 2017 outlook for the equity markets, 2017 outlook for the fixed income markets, Vanguard Group |

Mid May 2017

We are anticipating significant changes to fiscal and monetary policy in the United States that could begin later this year. After two recent interest rate hikes for example, Joe Davis, Vanguard’s chief global economist, says the Federal Reserve will likely announce plans for normalizing the balance sheet and any additional hikes later this summer. On Capitol Hill, legislators are focusing on tax reform and infrastructure as many expect these policies to spur economic growth reminiscent of prerecession levels.

These changes have the potential to shape the U.S. economic and financial market environment for years to come. But there are a lot of unknowns. Just as the Fed’s initial buying program in the wake of the last recession was a real-world experiment, it is also unclear how the market will react once it starts to shed assets. If implemented with care, new fiscal policies could lead to job creation and economic growth. However, Washington gridlock threatens to chip away at the positive sentiment behind economic and market expectations.

These policy changes look like a step in the right direction. But longer-term structural headwinds such as demographics, technology, and globalization will be tough to counteract.

That said, investors shouldn’t dismiss possible 2% economic growth in the long term as a sign of weakness. Rather, such growth levels should be considered fundamentally sound given the pressures of these three forces.

Dr. David Marcinko MBA

LikeLike

How you can prepare to weather the markets

While uncertain times are unavoidable, the good news is that you can prepare for them.

Invest according to your goals. Take a careful look at your portfolio, and ask yourself if your overall long-term strategy is sound. Do you have the right asset mix for your investment goal and time horizon? Are you properly diversified?

Focus on the big picture. Your investment decisions should always be strategic and not based on whether the market is up or down. Step away from the news, and ask yourself, does this event change my investment goals?

Rebalance. Disciplined rebalancing is vital to achieving long-term goals. It keeps your investment risk in check with your long-term plan.

Save more. Putting away something extra every opportunity you get isn’t easy, but it can give you the flexibility to get through tough situations.

Dr. David Marcinko MBA

LikeLike