A Real Insurance Solution

By Dr. David Edward Marcinko; MBA, CMP™

Publisher-in-Chief

Market Driven Health Insurance Alternatives

According to Michael K. Evans, former chief economist for the American Economics Group, Washington, DC, a real market driven insurance model may be a solution to the current health insurance coverage crisis.

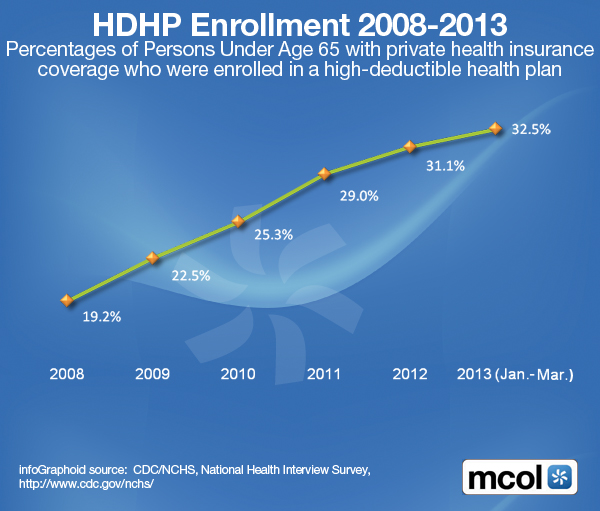

It would work like a Medical Savings Account [MSA], or Health Savings Account [HSA] or any other insurance plan; by self-payment for routine visits and medications and using the insurance only for catastrophic illness.

Ironically, this was the plan in the original Medicare legislation and the reason prescription drug costs were not covered until the adoption of Medicare Part D, a few years ago.

However, many older or sickly patients claim that the cost of doctors, hospitals and medications has risen so much that they are often forced to choose between food and medical care, since the CPI grossly understates the cost of living for the elderly. And, some experts therefore believe a one-time adjustment is needed to put those payments back where they actually cover the average market basket of goods and services they buy.

But, with adjustments must come an ironclad agreement that government aid for medical care should be used only for major costs associated with catastrophic illness, not routine care.

Furthermore, we believe that when drug companies, hospitals and physicians find that consumers are spending their own money, they will then work out more reasonable price schedules — or they won’t get paid.

Just, as not everyone can live in the most expensive neighborhood, not everyone can afford to see the most expensive doctor. As lower prices work their way through the system, employers who offer health-care benefits will find their financial situation also will benefit because costs incurred by employees will rise less rapidly.

In the long run, even though the initial effect will be to boost government spending, the net result will be lower medical-care costs, more covered recipients, less bureaucracy, more competent physicians, smaller government outlays and a greater chance that some medical manufacturing firms, or big pharma companies, will remain in the U.S. instead of outsourcing to countries where labor costs are much lower.

Your thoughts are appreciated – but it sure sounds like a HDHCP to me?

Filed under: Health Insurance | Tagged: High Deductible-HCPs | 3 Comments »