***

***

By Staff Reporters

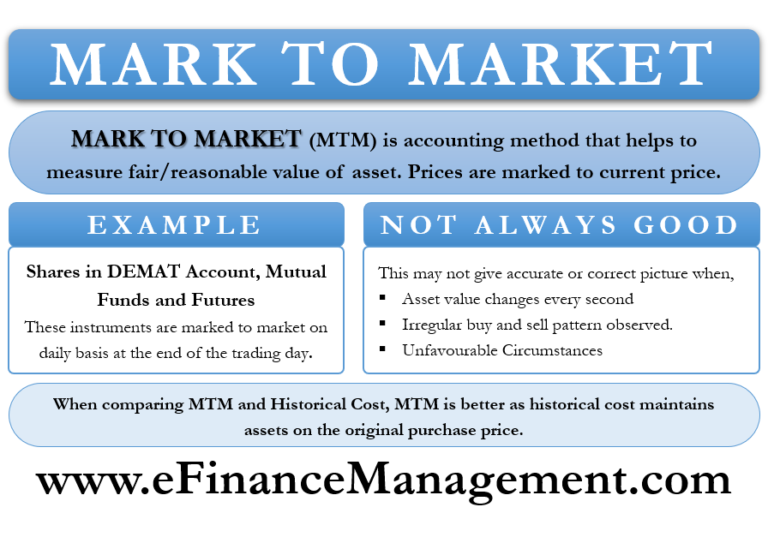

According to Wikipeida, Mark-to-market (MTM or M2M) or fair value accounting is accounting for the “fair value” of an asset or liability based on the current market price, or the price for similar assets and liabilities, or based on another objectively assessed “fair” value.[1] Fair value accounting has been a part of Generally Accepted Accounting Principles (GAAP) in the United States since the early 1990s. Failure to use it is viewed as the cause of the Orange County Bankruptcy,[2][3] even though its use is considered to be one of the reasons for the Enron scandal and the eventual bankruptcy of the company, as well as the closure of the accounting firm Arthur Andersen.[4]

Mark-to-market accounting can change values on the balance sheet as market conditions change. In contrast, historical cost accounting, based on the past transactions, is simpler, more stable, and easier to perform, but does not represent current market value. It summarizes past transactions instead. Mark-to-market accounting can become volatile if market prices fluctuate greatly or change unpredictably. Buyers and sellers may claim a number of specific instances when this is the case, including inability to value the future income and expenses both accurately and collectively, often due to unreliable information, or over-optimistic or over-pessimistic expectations of cash flow and earnings.[5]

Stock brokers allow their clients to access credit via margin accounts. These accounts allow clients to borrow funds to buy securities. Therefore, the amount of funds available is more than the value of cash (or equivalents). The credit is provided by charging a rate of interest and requiring a certain amount of collateral, in a similar way that banks provide loans. Even though the value of securities (stocks or other financial instruments such as options) fluctuates in the market, the value of accounts is not computed in real time. Marking-to-market is performed typically at the end of the trading day, and if the account value decreases below a given threshold (typically a ratio predefined by the broker), the broker issues a margin call that requires the client to deposit more funds or liquidate the account.

COMMENTS APPRECIATE

Thank You

***

***

Share this:

Filed under: Accounting, Experts Invited, Glossary Terms, Investing | Tagged: derivatives, FMV, GAAP, historical cost, margin, mark to market, market prive, MTM, MTM accounting, options |

Leave a comment