![]()

An Infographic

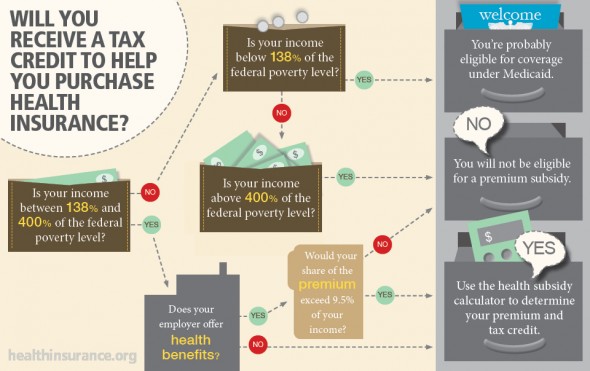

This infographic helps Americans determine whether they will be eligible for a health insurance premium subsidy under the Affordable Care Act aka Obamacare.

The infographic accompanies a story by blogger Maggie Mahar, who explains not only how eligibility for health insurance tax credits is determined, but also how much recipients should expect to receive.

The article also includes a chart with federal poverty level (FPL) numbers and links to a Kaiser Family Foundation premium subsidy calculator

Link: Healthinsurance.org

The graphic was created by Mahar, HIO editor Steve Anderson, and designer Barb Etzkorn. It was posted on the Blog of the Health Insurance Resource Center, one of the longest running sources of consumer health insurance information on the Web.

***

[Click to Enlarge]

Assessment

All healthcare and medical professionals should be aware of the information in this info-graphic; all FAs, too!

More:

- Doctors, Sole Proprietors and ObamaCare Taxes

- Taxes and the SCOTUS ACA Decision

- Supreme Court Upholds the PP-ACA Tax

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

- PRACTICES: www.BusinessofMedicalPractice.com

- HOSPITALS: http://www.crcpress.com/product/isbn/9781466558731

- CLINICS: http://www.crcpress.com/product/isbn/9781439879900

- ADVISORS: www.CertifiedMedicalPlanner.org

- FINANCE: Financial Planning for Physicians and Advisors

- INSURANCE: Risk Management and Insurance Strategies for Physicians and Advisors

- Dictionary of Health Economics and Finance

- Dictionary of Health Information Technology and Security

- Dictionary of Health Insurance and Managed Care

![]()

Share this:

Filed under: Health Insurance, Health Law & Policy | Tagged: ACA, ACA eligibility, ACA premiums, Healthinsurance.org, Kaiser Family Foundation, Maggie Mahar, Steve Anderson |

Health insurance plans?

Once upon a time, a health insurance plan offered by an employer was almost always the best option for couples and families. Group plans were able to offer affordable, broad coverage with low deductibles, and many employers paid a substantial share of the premiums.

That was then. Now, in the age of two-career families, soaring health care costs, and the changes Obamacare has brought to the health insurance market, the choices are much more complicated. It’s up to consumers to do the research to find the best options for themselves and their families.

Here are some suggestions to help with that research:

1. If both spouses are employed and both employers offer insurance, start by comparing the employers’ plans. Don’t just pick the lower premium and call it good, either. I’d suggest setting up a spreadsheet or chart to make it easier, and dig into the details of each plan. Compare the following:

• The specifics of what is covered and what is excluded

• Copays for office visits, emergency room visits, hospitalizations, and medications

• In-network and out-of-network costs

• Deductible amounts

• Annual out-of-pocket maximums

2. Also investigate each company’s employee policies related to health insurance. Some employers have restrictions or added costs that affect the availability of insurance for family members. Examples to look for include:

• Not covering spouses who can get insurance from their own employers

• Surcharges to cover spouses or dependents

• Income-adjusted premiums

3. Evaluate your health care history and probable needs for the coming year. Ask your current health insurance company for the explanation of benefits for the past year, or go through your checkbook and list all your health care expenses. Then get out your crystal ball and consider what kinds of health care your family might need in the near future.

You can’t predict everything, obviously, but you can at least make educated guesses about probable expenses like routine checkups, regular medications, visits to specialists, and elective surgeries. Take your lifestyle into account, as well. If you travel a lot, for example, you may need to use out-of-network health care more often.

4. Make sure the plans’ networks include all your doctors, including specialists like dermatologists as well as your family clinic. You can get this information from the insurance companies, but it’s often easier to call the doctors’ offices and ask which insurance companies they have agreements with.

5. Check out plans offered through your state’s insurance exchange. If you don’t qualify for subsidies, these plans may be more expensive than employer plans. Don’t assume this to be the case, though; find out.

6. Investigate Health Savings Accounts. An HSA offers a tax-advantaged way to save money for out-of-pocket medical costs. It is available to those covered by health insurance plans with high deductibles (currently $1,300 for individuals and $2,600 for families). However, not all high-deductible plans are eligible for HSA’s.

Annual pretax contributions to HSA’s are capped at $3,350 for individuals and $6,650 for families (plus another $1000 for those over 55). There is no time limit for withdrawing the funds, which are not taxed if they are used for medical costs. Before you open an HSA, make sure you’re eligible, and look for low investment fees. Ironically, because of the tax advantages, you may get the most benefit from an HSA by not using it for health care expenses but leaving the funds in the account to grow.

Doing this much research before choosing a health insurance plan may seem daunting. Yet it’s well worth your time. The more informed you are, the better able you are to select the best available coverage at the lowest cost.

Rick Kahler MS CFP®

LikeLike

1 in 4 Employers Could be Subject to the ‘Cadillac Tax’ in 2018

The Kaiser Family Foundation recently released an prospective analysis on the Affordable Care Act’s tax on high-cost health plans (‘Cadillac Tax’). Here are some key findings from the report:

• 1 in 4 employers offering health benefits could be subject to the ‘Cadillac Tax’ in 2018.

• The 2018 tax thresholds are $10,200 for single coverage and $27,500 for other coverage.

• The tax is 40% of the difference between the annual cost of health benefits and the threshold amount.

• An estimated 30% of employers would be subject to the tax by 2023.

• By 2028, 42% of employers may have plans where costs exceed the threshold for some or all employees.

• Today, 19% of employers would be taxed if the ‘Cadillac Tax’ was in effect.

Source: Kaiser Family Foundation, August 25, 2015

LikeLike