![]()

An ME-P Update

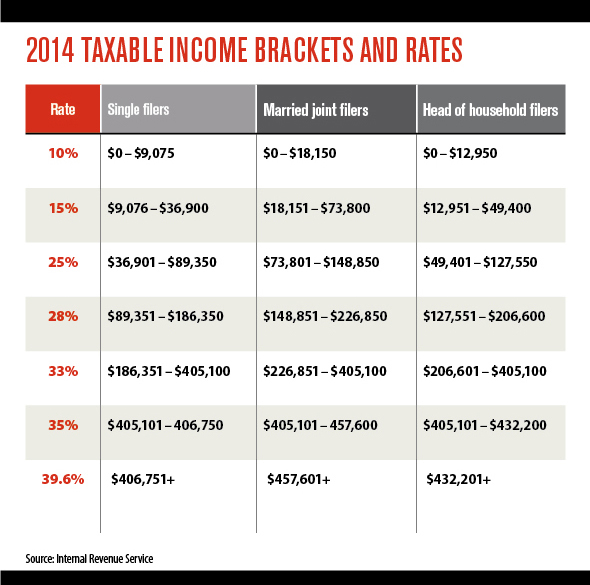

[By Internal Revenue Service]

***

***

More:

- Why You Should [Still] Know Your Marginal Tax Rate?

- Does the Method of Tax Filing Change IRS Audit Potential?

- Does the Method of Tax Filing Change IRS Audit Potential?

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

- DICTIONARIES: http://www.springerpub.com/Search/marcinko

- PHYSICIANS: www.MedicalBusinessAdvisors.com

- PRACTICES: www.BusinessofMedicalPractice.com

- HOSPITALS: http://www.crcpress.com/product/isbn/9781466558731

- CLINICS: http://www.crcpress.com/product/isbn/9781439879900

- ADVISORS: www.CertifiedMedicalPlanner.org

- BLOG: www.MedicalExecutivePost.com

- FINANCE: Financial Planning for Physicians and Advisors

- INSURANCE: Risk Management and Insurance Strategies for Physicians and Advisors

TEXTBOOK

Share this:

Filed under: Accounting, Taxation | Tagged: Income Tax Brackets and Rates 2014, IRS, tax brackets., tax rates |

Tax Rates

Many thanks for this info-graphic. The related posts are especially good.

Zafar

LikeLike

11 tax-smart ways to cut health costs

Insurers want you to pay more for your health care, so it’s important to know the tax implications so you can cut those costs and reduce your marginal tax brackets.

http://money.msn.com/health-and-life-insurance/11-tax-smart-ways-to-cut-health-costs

Horst

LikeLike

IRS warns of delays if U.S. Congress fumbles tax ‘extenders’

Severe delays and inconvenience for millions of taxpayers could result in 2015 if the U.S. Congress fails to deal soon with a list of temporary tax laws that expired at the end of 2013.

http://www.msn.com/en-us/news/politics/irs-warns-of-delays-if-us-congress-fumbles-tax-extenders/ar-BB84kky

Zafar

LikeLike

Individual Provisions our newest tax legislation in 2014

The “Tax Increase Prevention Act of 2014” or TIPA, which was passed by the senate on December 16, has various individual tax deductions that have been retroactively renewed through the end of 2014. The law has passed the House and Senate, the President is EXPECTED to sign it, but we are planning based upon expectations. I will list them below. Each specific new law is in bold followed by some detail for each. Enjoy the read!

One to specifically pay attention to is the IRA to Charity contribution. If you are required to take a required minimum distribution for 2014 and haven’t already this year, then you can transfer funds directly from your IRA to the charity and avoid income recognition but still count it as the required minimum distribution.

New law. TIPA retroactively extends the educator expense deduction one year so that it applies to expenses paid or incurred in tax years through 2014. (Code Sec. 62(a)(2)(D), as amended by Act Sec. 101(a)) This is a $250 deduction available for teachers.

New law. TIPA extends this exclusion for one year so that it applies to home mortgage debt discharged before Jan. 1, 2015. (Code Sec. 108(a)(1)(E), as amended by Act Sec. 102(a))

Exclusion for Discharged Home Mortgage Debt Extended

Discharge of indebtedness income from qualified principal residence debt, up to a $2 million limit ($1 million for married individuals filing separately) is excluded from gross income.

Under pre-Act law, this exclusion didn’t apply to any debt discharged after Dec. 31, 2013.

New law. TIPA extends for one year the parity provision, through 2014. Thus, for 2014, it increases the monthly exclusion for employer-provided transit and vanpool benefits to $250—the same as for the exclusion for employer-provided parking benefits. (Code Sec. 132(f)(2), as amended by Act Sec. 103(a))

Increase in Excludible Employer-Provided Mass Transit and Parking Benefits Extended

Under pre-Act law, for 2014, an employee may exclude from gross income up to: (1) $250 per month for qualified parking, and (2) $130 a month for transit passes and commuter transportation in a commuter highway vehicle (including van pools). However, notwithstanding the applicable statutory limits on the exclusion of qualified transportation fringes (as adjusted for inflation), for any month beginning before Jan. 1, 2014, a parity provision required that the monthly dollar limitation for transit passes and transportation in a commuter highway vehicle had to be applied as if it were the same as the dollar limitation for that month for employer-provided parking ($245 for 2013).

New law. TIPA retroactively extends this provision for one year so that a taxpayer can deduct, as qualified residence interest, mortgage insurance premiums paid or accrued before Jan. 1, 2015 (and not properly allocable to any period after 2014). (Code Sec. 163(h)(3)(E), as amended by Act Sec. 104(a))

Mortgage Insurance Premiums as Deductible Qualified Residence Interest Extended

Mortgage insurance premiums paid or accrued by a taxpayer in connection with acquisition indebtedness with respect to the taxpayer’s qualified residence are treated as deductible qualified residence interest, subject to a phase-out based on the taxpayer’s adjusted gross income (AGI). The amount allowable as a deduction is phased out ratably by 10% for each $1,000 by which the taxpayer’s adjusted gross income exceeds $100,000 ($500 and $50,000, respectively, in the case of a married individual filing a separate return). Thus, the deduction isn’t allowed if the taxpayer’s AGI exceeds $110,000 ($55,000 in the case of married individual filing a separate return).

Under pre-Act law, this provision only applied to premiums paid or accrued before Jan. 1, 2014 (and not properly allocable to any period after that date).

New law. TIPA retroactively extends this provision for one year so that itemizers can elect to deduct state and local sales and use taxes instead of state and local income taxes for tax years beginning before Jan. 1, 2015. (Code Sec. 164(b)(5)(I), as amended by Act Sec. 105(a))

State and Local Sales Tax Deduction Extended

Taxpayers who itemize deductions may elect to deduct state and local general sales and use taxes instead of state and local income taxes.

Under pre-Act law, this choice was unavailable for tax years beginning after Dec. 31, 2013.

New law. TIPA retroactively extends for one year the 50% and 100% limitations on qualified conservation contributions of appreciated real property so that they apply to contributions made in tax years beginning before Jan. 1, 2015. (Code Sec. 170(b)(1)(E) and Code Sec. 170(b)(2)(B) , as amended by Act Sec. 106(a) and 106(b))

Liberalized Rules for Qualified Conservation Contributions Extended

A taxpayer’s aggregate qualified conservation contributions (i.e., contributions of appreciated real property for conservation purposes) are allowed up to the excess of 50% of the taxpayer’s contribution base over the amount of all other allowable charitable contributions (100% for qualified farmers and ranchers), with a 15-year carryover of such contributions in excess of the applicable limitation.

Under pre-Act law, these rules didn’t apply to any contribution made in a tax year beginning after Dec. 31, 2013, and contributions made thereafter were to be subject to the otherwise applicable 30% limit for capital gain property (50% limit for qualified farmers and ranchers).

New law. TIPA retroactively extends the qualified tuition deduction for one year so that it can be claimed for tax years beginning before Jan. 1, 2015. (Code Sec. 222(e), as amended by Act Sec. 107(a))

Above-the-Line Deduction for Higher Education Expenses Extended

Eligible individuals can deduct higher education expenses—i.e., “qualified tuition and related expenses” of the taxpayer, his spouse, or dependents—as an adjustment to gross income to arrive at adjusted gross income. The maximum deduction is $4,000 for an individual whose AGI for the tax year doesn’t exceed $65,000 ($130,000 in the case of a joint return), or $2,000 for individuals who don’t meet the above AGI limit, but whose adjusted gross income doesn’t exceed $80,000 ($160,000 in the case of a joint return). No deduction is allowed for an individual whose adjusted gross income exceeds the relevant adjusted gross income limitations, for a married individual who does not file a joint return, or for an individual for whom a personal exemption deduction may be claimed by another taxpayer for the tax year.

Under pre-Act law, this deduction wasn’t available for tax years beginning after Dec. 31, 2013.

New law. TIPA retroactively extends this provision for one year so that it’s available for charitable IRA transfers made in tax years beginning before Jan. 1, 2015. (Code Sec. 408(d)(8)(F), as amended by Act Sec. 108(a))

Nontaxable IRA Transfers to Eligible Charities Extended

Taxpayers who are age 70 1/2 or older can make tax-free distributions to a charity from an Individual Retirement Account (IRA) of up to $100,000 per year. These distributions aren’t subject to the charitable contribution percentage limits since they are neither included in gross income nor claimed as a deduction on the taxpayer’s return.

Under pre-Act law, these rules didn’t apply to distributions made in tax years beginning after Dec. 31, 2013.

Robert Whirley CPA

[Managing Partner]

Whirley & Associates, LLC + ProActive Advisory

LikeLike

Tax Time 2015

As a CPA, do your clients bug you every year that they’re paying too much in taxes, and there’s no way that their buddies at work or down the street are paying as much as they are?

Or, if you are a doctor, are you itching to know your tax burden for this year?

Well, Kiplinger has created a simple tax calculator to determine just how everyone ranks.

http://www.kiplinger.com/tool/taxes/T055-S001-your-tax-burden-calculator/index.php

By simply putting in the AGI from the most recent tax return (or annual salary), anyone can find out how their income compares and what portion of the tax burden they bear.

Lambert

LikeLike