ME-P SYNDICATIONS:

WSJ.com,

CNN.com,

Forbes.com,

WashingtonPost.com,

BusinessWeek.com,

USNews.com, Reuters.com,

TimeWarnerCable.com,

e-How.com,

News Alloy.com,

and Congress.org

BOARD CERTIFICATION EXAM STUDY GUIDES

Lower Extremity Trauma

[Click on Image to Enlarge]

The “Medical Executive-Post” is about connecting doctors, health care executives and modern consulting advisors. It’s about free-enterprise, business, practice, policy, personal financial planning and wealth building capitalism. We have an attitude that’s independent, outspoken, intelligent and so Next-Gen; often edgy, usually controversial. And, our consultants “got fly”, just like U. Read it! Write it! Post it! “Medical Executive-Post”. Call or email us for your FREE advertising and sales consultation TODAY [678.779.8597] Email: MarcinkoAdvisors@outlook.com

ePodiatryConsentForms.com

Suite #5901 Wilbanks Drive, Norcross, Georgia, 30092 USA [1.678.779.8597]. Our location is real and we are now virtually enabled to assist new long distance clients and out-of-town colleagues.

If you want the opportunity to work with leading health care industry insiders, innovators and watchers, the “ME-P” may be right for you? We are unbiased and operate at the nexus of theoretical and applied R&D. Collaborate with us and you’ll put your brand in front of a smart & tightly focused demographic; one at the forefront of our emerging healthcare free marketplace of informed and professional “movers and shakers.” Our Ad Rate Card is available upon request [678-779-8597].

“Providing Management, Financial and Business Solutions for Modernity”

Whether you’re a mature CXO, physician or start-up entrepreneur in need of management, financial, HR or business planning information on free markets and competition, the "Medical Executive-Post” is the online place to meet for Capitalism 2.0 collaboration.

Support our online development, and advance our onground research initiatives in free market economics, as we seek to showcase the brightest Next-Gen minds.

THE ME-P DISCLAIMER: Posts, comments and opinions do not necessarily represent iMBA, Inc., but become our property after submission. Copyright © 2006 to-date. iMBA, Inc allows colleges, universities, medical and financial professionals and related clinics, hospitals and non-profit healthcare organizations to distribute our proprietary essays, photos, videos, audios and other documents; etc. However, please review copyright and usage information for each individual asset before submission to us, and/or placement on your publication or web site. Attestation references, citations and/or back-links are required. All other assets are property of the individual copyright holder.

Sex differences in utilization with high-deductible coverage

Jason Hockenberry comments on a new study by Katy Kozhimannil and colleagues; from the IE by Austin Frakt PhD:

This study includes interesting descriptive evidence that suggests that men’s use of the ED decreased to a greater extent than women’s during the period immediately following their employers’ switch from an HMO to an HDHP [high deductible health plan].

The pattern of reduction by sex was also quite different by severity of the visit. Womens’ relative reduction in ED use was concentrated in low-severity visits, whereas men’s relative reductions were similar in magnitude in the low and intermediate category but was markedly higher in the high severity category.

In addition, there was an immediate reduction in inpatient hospitalizations in the first year among men who worked for employers who switched to HDHPs, followed by what could be interpreted as a reversion to the preperiod level in the second year.

https://blu171.mail.live.com/default.aspx#n=1380891100&fid=1&mid=35381946-f387-11e2-a2d0-00237de4a660&fv=1

Any comments or thoughts?

Ben

LikeLike

HDHCPs are Ruling

Quote: “Expect higher deductibles”

In the ACA, Congress chose market-based cost controls over measures that are common internationally, such as global budgets. Mandating coverage while requiring affordable premiums without enacting other cost-control mechanisms almost inevitably gives rise to increased cost sharing as the simplest mechanism for reducing premiums.

The ACA is therefore expected to cause a “seismic shift” in HDHP enrollment. Small employers newly required to purchase employees’ insurance may well choose HDHPs as the least expensive coverage option. Larger employers might adopt HDHPs to achieve ACA-regulated premium levels and avoid the 2018 “Cadillac tax.”

http://theincidentaleconomist.com/wordpress/quote-expect-higher-deductibles/

[J. Frank Wharam, Dennis Ross-Degnan and Meredith Rosenthal]

New England Journal of Medicine

Sharon

LikeLike

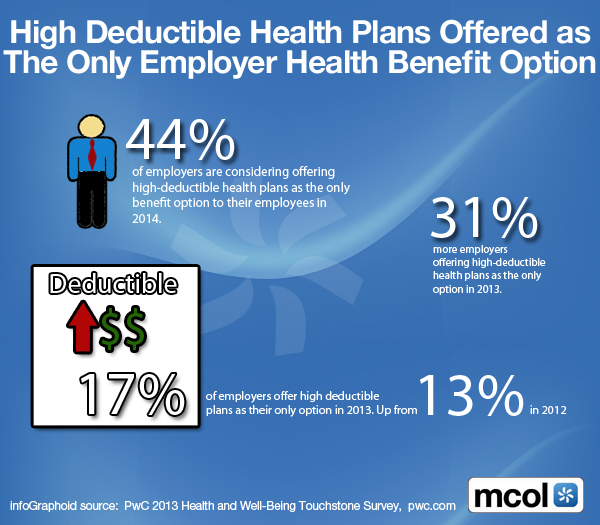

Some perspectives on HDHCPs

While there has been a general growth trend in high deductible health plans (HDHPs), in our public agency and health systems niches (and most collectively bargained industries in California), adoption of high deductible plans has been somewhat slow.

However, where PPO participation is still a significant factor, HDHPs will likely become more accepted as a way to increase affordability to help employers comply with the Affordable Care Act. The looming 2018 Cadillac Tax will potentially accelerate this trend, as the premiums for many employer plans are close to, or already exceed, the 2018 tax threshold.

Since one of the main objectives for implementing HDHPs is the enhancement of consumer engagement, a more significant upfront investment in participant education and provider performance data is essential. Health care consumerism depends on the consumer being knowledgeable in selecting providers and having actionable information about their prospective providers. Better scorecard data is available than in the past, but not nearly enough on pricing for the patient-consumer to negotiate. At the very least, HDHP participants need to be better equipped with the appropriate questions to ask. Consumers as patients need to be informed, not only about the expectations and risks of their treatment, but also the cost-effectiveness of the treatment and why they should choose a particular provider for their treatment.

From my standpoint as a medical provider, HDHPs have traditionally not been compatible in most cases with coordinated care capitated arrangements as delivered by California organized medical groups.

In addition, the higher deductible can result in increased bad debt exposure for providers, which is of significant concern. Thus, we need to be mindful of this in the implementation of HDHPs.

For HDHPs to be successful in controlling cost trends, they must create incentives for patients, providers, payers and plan sponsors to operate in an open, competitive market where value and quality are keys to success. When incentives are properly aligned it maximizes the opportunity to deliver the best overall results.

Dr. David Edward Marcinko MBA CMP™

http://www.CertifiedMedicalPlanner.org

LikeLike

Percentages of persons under age 65 with private health insurance coverage who were enrolled in a high-deductible health plan

1.2008 – 19.2%

2.2009 – 22.5%

3.2010 – 25.3%

4.2011 – 29.0%

5.2012 – 31.1%

6.2013 ( Jan. – Sept. ) – 33.4%

Source: CDC/NCHS, National Health Interview Survey

LikeLike

Triple Tax-Free Play

If patients choose a high-deductible plan, they pay less per month and they can put the difference in an HSA where there is triple tax savings — money goes in tax free; it earns tax-fee interest, and it goes out tax-free.

Gene

LikeLike

More on HSAs and High Deductible Plans

IRS urged to broaden preventive coverage.

http://www.medicalpracticeinsider.com/news/irs-urged-broaden-preventive-coverage-high-deductible-plans?email=MARCINKOADVISORS@MSN.COM&GroupID=90115

Hope R. Hetico RN MHA

LikeLike

Disrupting Deductibles

An Innovative Approach to HD-HCPs.

http://thehealthcareblog.com/blog/2016/11/02/disrupting-deductibles-an-innovative-approach-to-hdhps/

Clarence

LikeLike

39.1% of Adults Had A High-Deductible Health Plan in 2016

The National Center for Health Statistics recently released estimates from their 2016 National Health Interview Survey on health insurance coverage. Here are some key findings from the report:

• In 2016, 28.2 million (8.8%) persons of all ages were uninsured.

• 20.4 million fewer persons were uninsured in 2016 than in 2010.

• 20.3% of adults had public coverage and 69% had private coverage in 2016.

• In 2016, 43.4% of children had public coverage and 53.5% had private coverage.

• 4.9% of adults had coverage through the Marketplace or state exchanges.

• Those with high-deductible health plans increased from 36.7% in 2015 to 39.1%.

Source: Centers for Disease Control and Prevention, February 2017

LikeLike