![]()

Your Children and Your Money

By Rick Kahler CFP

By Rick Kahler CFP

As a doctor – Do your kids know how much money you make? If not, and they asked, would you feel comfortable telling them?

My hunch is that the most common answer to both these questions is “No.” Talking about money is such a strong taboo that it often keeps us from sharing information about our earnings and net worth even with members of our immediate families.

Yet being honest with children about what we earn and how we spend it is a perfect opportunity to teach them important life lessons about money.

Here are a few suggestions to foster those conversations:

- Take advantage of teachable moments. As with many other big questions, like where babies come from or whether cats go to heaven (personally, I doubt it, but that may say more about my prejudices than my theology), the ideal time to answer money questions is when the kids ask.

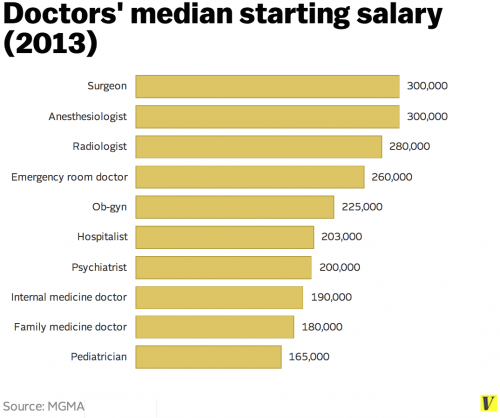

- Provide context for numbers. To a child who gets an allowance of five bucks a week, either $10,000 or $100,000 a year can seem huge. One way to put those numbers into context is with comparisons: “I earn about the same amount as your teachers do,” or, “Most doctors probably earn about twice as much as our family does.”

- Talk about expenses as well as income. This is huge. It’s another important way of providing context. Plus it helps open kids’ eyes to the realities of earning and spending. When my kids, at about age 10 and 14, first asked about my income, they were impressed with how high the number was. Then we looked at the family expenses: house payment, health insurance, food, college savings, and everything else. They were even more impressed. Seeing what things cost and where the money goes is a good start to educating kids about spending, saving, and creating healthy money habits.

- Share appropriately for kids’ ages and understanding. Seven-year-olds and 13-year-olds aren’t ready for the same information. Don’t underestimate your kids’ comprehension, however; if you encourage them to ask questions and are willing to explain and clarify, they may understand more than you expect.

- Tell the truth. If you have financial difficulties that stem from your own money mistakes or other bad choices, being honest with your kids can be a powerful teaching opportunity. If you don’t earn a lot but are managing to take care of the family, that’s something to be proud of. If your kids may inherit substantial amounts, it’s wise to start teaching them early how to deal with wealth. Whether you have a net worth in the millions or are barely getting by from month to month, clean honesty about the family finances is a good policy.

- Remember that you’re the adult. Over-sharing about financial challenges can frighten your kids. It’s more useful to be matter-of-fact about problems and focus on what you’re doing to solve them.

- Keep in mind that when parents don’t talk about money, kids will make up their own stories. Typically this will be either that you earn and have more than you do, or that the family is on the brink of bankruptcy and homelessness.

- Look at your own shame and secrecy about money. If parents never talk about money, kids may never ask money questions. Either the topic is simply not on their radar, or they have internalized the unspoken message that it is off limits. In either case, parents can change the family culture by becoming more open about their finances. Those teachable moments for kids begin to happen when money is no longer a secret.

***

***

More:

- More on the Doctor Salary Conundrum

- MD Salary versus Net-Worth Conundrum [.ppt slide-show presentation]

- More on Doctors and Personal Net Worth

- Rich Doctor’s?- Maybe Not!

Conclusion

Your thoughts and comments on this ME-P are appreciated. Feel free to review our top-left column, and top-right sidebar materials, links, URLs and related websites, too. Then, subscribe to the ME-P. It is fast, free and secure.

Speaker: If you need a moderator or speaker for an upcoming event, Dr. David E. Marcinko; MBA – Publisher-in-Chief of the Medical Executive-Post – is available for seminar or speaking engagements. Contact: MarcinkoAdvisors@msn.com

OUR OTHER PRINT BOOKS AND RELATED INFORMATION SOURCES:

- PRACTICES: www.BusinessofMedicalPractice.com

- HOSPITALS: http://www.crcpress.com/product/isbn/9781466558731

- CLINICS: http://www.crcpress.com/product/isbn/9781439879900

- ADVISORS: www.CertifiedMedicalPlanner.org

- FINANCE: Financial Planning for Physicians and Advisors

- INSURANCE: Risk Management and Insurance Strategies for Physicians and Advisors

- Dictionary of Health Economics and Finance

- Dictionary of Health Information Technology and Security

- Dictionary of Health Insurance and Managed Care

[PHYSICIAN FOCUSED FINANCIAL PLANNING AND RISK MANAGEMENT COMPANION TEXTBOOK SET]

***

Share this:

Filed under: "Doctors Only", Career Development, Health Economics, Practice Worth | Tagged: physician income, physician salary |

TEENS

Teen allowance is being upgraded from cash wads to full-on banking apps. Yesterday, two such apps, Current and Step, announced new funding rounds of $220 million and $100 million, respectively. Now worth $2.2 billion, Current tripled its valuation in just five months.

Both apps let parents and teens make deposits and offer no-fee checking accounts, since in high school being a thousandaire feels like being London Tipton.

How are Current and Step different?

* Current focuses on signing up parents, while Step focuses on recruiting teens.

* Current has almost 3 million users. Step has 1.5 million, but has only been around for six months.

* Current’s backed by traditional VC heavyweights like a16z. Step’s investor lineup looks more like a red carpet: Charli D’Amelio, The Chainsmokers, and Will Smith, to name a few.

And yesterday, it revealed Steph Curry was on board.

Angelo

LikeLike